With gold trading above $4,500 per ounce in March 2026 and record inflows pouring into gold-backed ETFs, more investors than ever are asking a deceptively simple question: where does all that gold actually sit, and who really owns it?

The answer depends almost entirely on the type of storage account behind the investment. The difference between allocated and unallocated gold storage is not just a technicality. It determines whether you hold legal title to specific bars of metal or whether you are simply an unsecured creditor with a claim on a pool of gold that may or may not exist in the quantity promised. For investors building meaningful positions in physical gold, understanding this distinction could be one of the most important decisions they make.

What Is Allocated Gold Storage?

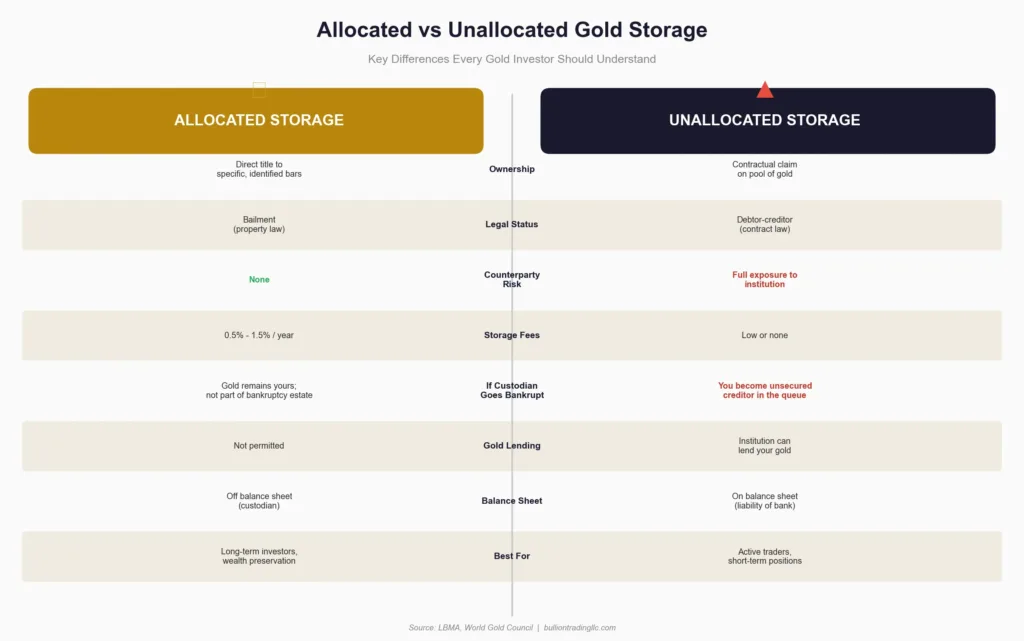

In an allocated gold account, specific gold bars are identified, recorded by serial number, weight, and assay (purity mark), and held in a vault on your behalf. Think of it like a safe deposit box at a bank, except instead of holding documents or jewelry, the box contains uniquely identified gold bars that belong to you and only you.

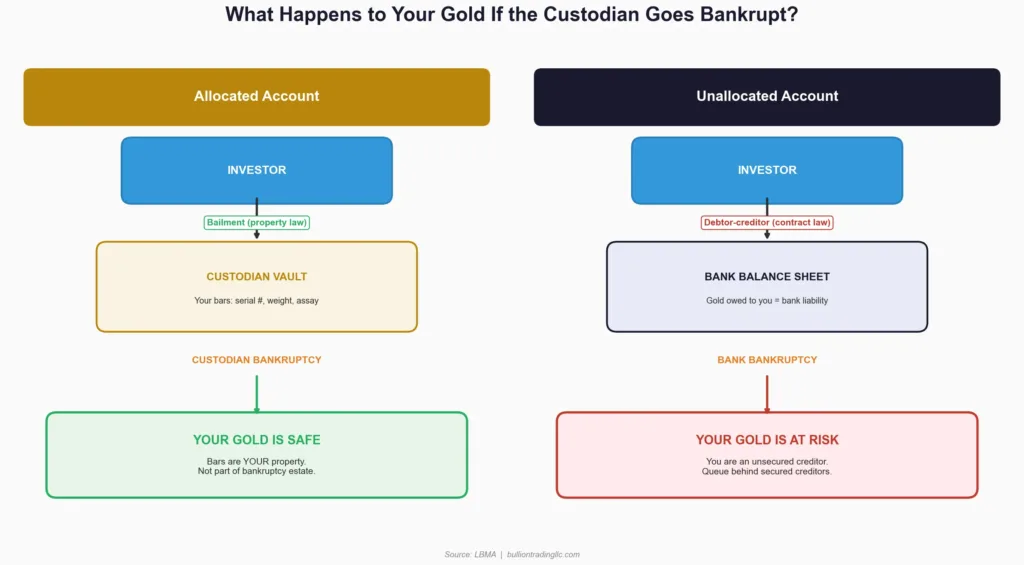

The custodian acts as a bailee under this arrangement. According to the London Bullion Market Association’s guide to the precious metals market, the custodian has no right to use, lend, lease, or otherwise deal with the gold in an allocated account. The metal is segregated from the custodian’s own assets and from the assets of other clients. Each bar on your account appears on a specific weight list that details its unique identifier, refiner, gross weight, and fineness.

This matters most in a worst-case scenario. If the custodian or vault operator goes bankrupt, allocated gold does not become part of the bankruptcy estate. Because you hold legal title to specific, identified bars, those bars are yours to claim. Creditors of the failed institution cannot touch them. This protection is rooted in property law rather than contract law, and it is why allocated storage is widely considered the gold standard (if you will forgive the pun) for physical gold custody.

The tradeoff is cost. Allocated storage typically involves annual storage fees ranging from 0.5% to 1.5% of the metal’s value, depending on the provider and the amount stored. The custodian earns no income from the gold itself because they cannot lend or trade it, so the storage fee is their only revenue from the arrangement.

What Is Unallocated Gold Storage?

Unallocated gold storage works very differently. When you hold gold in an unallocated account, no specific bars are assigned to you. Instead, you have a contractual claim on a certain quantity of gold from the institution, similar to a deposit at a bank. The institution owes you a quantity of gold, but it has no obligation to hold specific bars on your behalf.

This is the mechanism that underpins most of the London over-the-counter (OTC) gold market. As the LBMA’s comprehensive market guide explains, unallocated accounts are the primary vehicle through which wholesale gold is traded globally, and they function in a way that is conceptually similar to a bank current account. The institution can use the underlying gold for its own trading, lending, and hedging operations, and in return, it typically charges no storage fees or very low ones.

The appeal is obvious. Lower costs, simpler administration, and easy liquidity. For institutional traders who need to move large quantities of gold in and out of positions quickly, unallocated accounts offer flexibility that allocated accounts cannot match. But that convenience comes with a significant catch. In an unallocated arrangement, you are an unsecured creditor of the institution. If the bank or dealer holding your unallocated gold goes insolvent, you do not have a claim on specific bars sitting in a vault. Instead, you join the queue of unsecured creditors, alongside bondholders, trade counterparties, and other depositors, hoping to recover a fraction of what you are owed after secured creditors and administrators have been paid.

Why the Legal Distinction Matters More Than You Think

For years, many investors treated the difference between allocated and unallocated gold as an abstract distinction. If the institution was large and reputable, the thinking went, the risk was negligible. History has shown otherwise.

In 2023, an investigation by the Australian Broadcasting Corporation’s Four Corners program raised serious questions about the Perth Mint’s handling of its depository storage program. The investigation revealed that the mint had sold gold dore containing impurities to the Shanghai Gold Exchange and raised broader concerns about whether customer metal in certain accounts was being managed as transparently as depositors believed. While the mint denied allegations of mishandling depositor gold, the controversy highlighted the real-world risks that can arise when the lines between allocated and unallocated storage are not crystal clear.

The collapse of MF Global in 2011 offers another cautionary example. When the futures broker went bankrupt, customers who believed their assets were segregated discovered that funds had been commingled. Although this case involved cash and futures rather than physical gold specifically, it demonstrated that unsecured creditor status can become painfully real when a counterparty fails.

These episodes are not reasons to panic. They are reasons to ask pointed questions about exactly how your gold is held, what documentation supports your ownership, and what protections exist in the jurisdiction where your gold is vaulted.

How Basel III Changed the Game

The regulatory landscape for gold storage shifted significantly with the implementation of the Basel III banking framework. Under the Net Stable Funding Ratio (NSFR) rules, which have been phased in across major jurisdictions over the past few years, the regulatory treatment of allocated and unallocated gold diverged sharply.

Allocated gold held in custody does not appear on a bank’s balance sheet. It belongs to the client, the bank is simply storing it, and therefore it carries no capital charge for the bank. Unallocated gold, by contrast, is a liability of the bank. Because the bank owes a quantity of gold to the account holder, the obligation sits on its balance sheet. Under Basel III’s NSFR, banks are required to hold stable funding equal to 85% of the value of their unallocated gold liabilities.

The practical impact has been substantial. Holding large unallocated gold positions became significantly more expensive for banks, which prompted many institutions to restructure their precious metals operations. Some banks exited the gold clearing business. Others encouraged clients to shift from unallocated to allocated storage, or introduced new fee structures that reduced the cost advantage unallocated accounts once enjoyed.

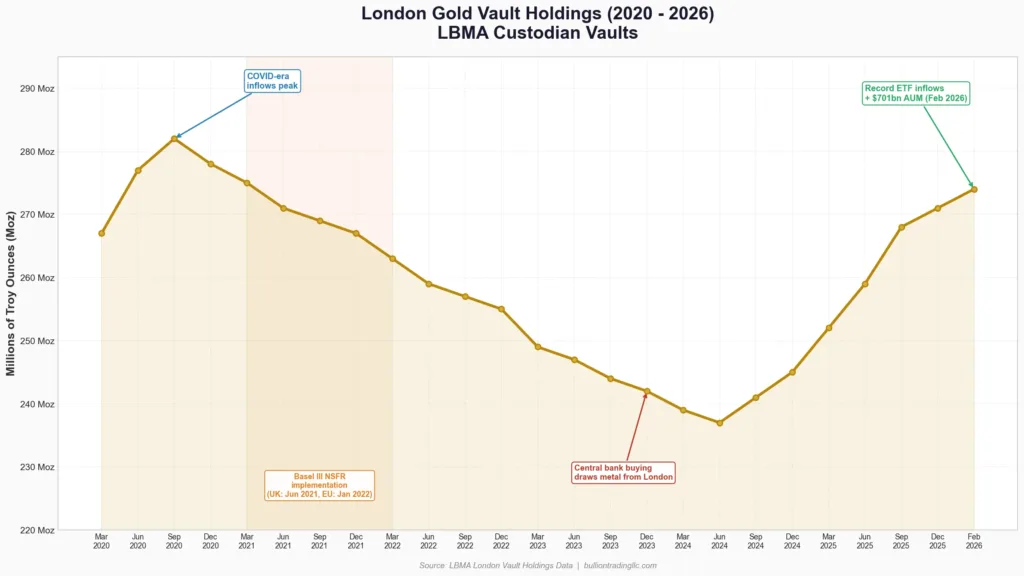

According to the LBMA’s London vault holdings data, which tracks gold held in London’s network of custodian vaults, the volume of gold stored in London has remained substantial throughout this transition period. The data shows the market adapting to the new regulatory reality rather than contracting.

For individual investors, the Basel III shift has actually been positive. As the economics of unallocated storage became less favorable for banks, allocated storage options expanded and, in some cases, became more competitively priced. The regulation effectively nudged the industry toward the storage model that provides better investor protection.

Gold ETFs and the Allocated Storage Connection

The explosive growth of gold-backed exchange-traded funds has brought the allocated storage question into mainstream investor consciousness. According to the World Gold Council’s latest ETF data, global gold-backed ETF holdings reached an all-time high of 4,171 tonnes by February 2026, with total assets under management hitting a record $701 billion. This followed nine consecutive months of net inflows, driven by geopolitical risk, shifting macro conditions, and strong gold price performance.

Most major physically backed gold ETFs, including SPDR Gold Shares (GLD) and iShares Gold Trust (IAU), use allocated storage for their metal. The gold is held in LBMA-approved vaults (primarily in London) and each bar is identified by serial number and included in a published bar list. This is an important distinction from some smaller or less transparent funds that may use unallocated arrangements for at least a portion of their holdings.

Before investing in any gold ETF, it pays to read the prospectus carefully. Look for explicit language about allocated storage, published bar lists, and regular independent audits of vault holdings. The World Gold Council’s 2025 Gold Demand Trends report noted that total gold demand exceeded 5,000 tonnes during the year, with investment fueling much of that growth. As more money flows into gold-backed products, the quality of the custody arrangements behind those products becomes increasingly important.

Choosing the Right Storage for Your Situation

The right choice between allocated and unallocated gold storage depends on what you are trying to achieve.

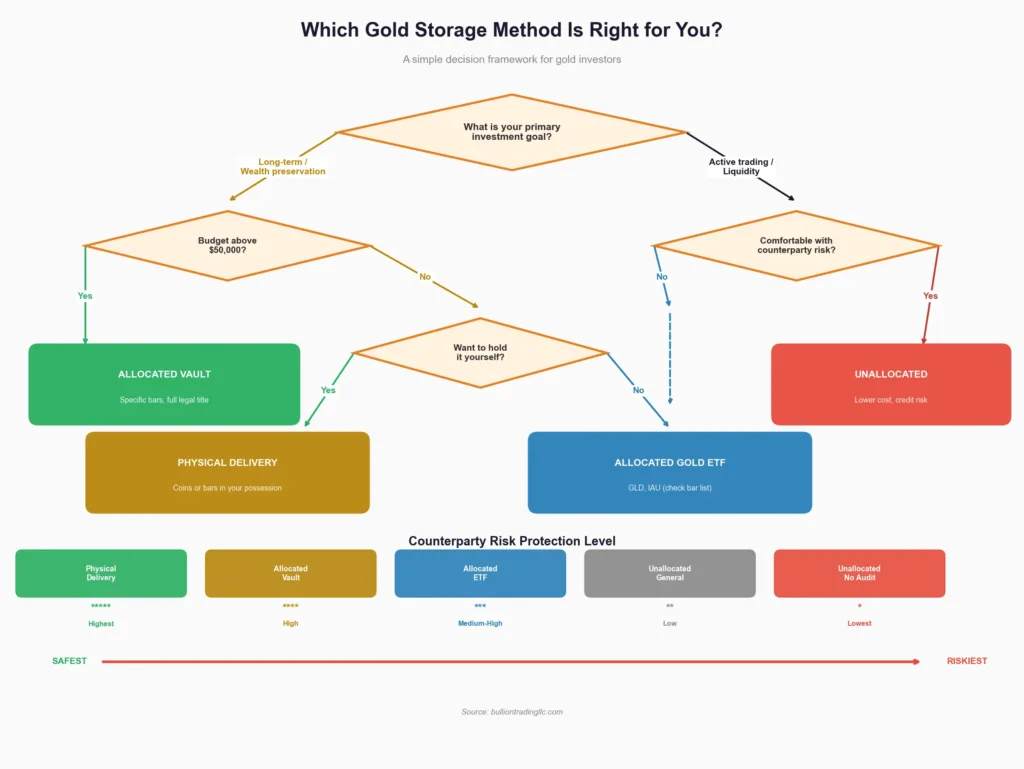

If you are a long-term investor holding gold as a portfolio hedge, wealth preservation tool, or insurance against systemic financial risk, allocated storage is almost certainly the better fit. The whole point of owning physical gold, as opposed to paper gold, is to eliminate counterparty risk. Holding gold in an unallocated account reintroduces exactly the kind of counterparty risk most physical gold buyers are trying to avoid.

For active traders who move in and out of gold positions frequently and need maximum liquidity, unallocated accounts can serve a practical purpose. The ability to settle trades quickly without transferring specific bars reduces friction in active trading strategies. But even active traders should be aware that their unallocated balance carries credit risk tied to the holding institution.

There are also practical factors to consider. Allocated storage with a reputable custodian typically requires meeting minimum investment thresholds, often starting around $50,000 to $100,000 worth of gold. Smaller investors who want the benefits of allocated storage can achieve something similar by purchasing physical gold coins or bars from a trusted dealer like Bullion Trading LLC and either storing the metal at home or in a private vault. Taking physical delivery eliminates the allocated-versus-unallocated question entirely because you hold the metal yourself.

Questions to Ask Before You Store Gold Anywhere

Whether you are opening a storage account with a bank, a bullion dealer, or a vault provider, there are several questions worth asking before committing your capital.

First, is the account allocated or unallocated, and can you receive a specific weight list identifying your bars by serial number, refiner, weight, and fineness? If the provider cannot produce this documentation, the storage is likely unallocated regardless of how they market it.

Second, what jurisdiction is the gold stored in, and what legal protections exist for allocated account holders in that jurisdiction? Vaulting gold in a jurisdiction with strong property rights and clear legal precedent for segregated custody (such as Switzerland, Singapore, or the United Kingdom) provides an additional layer of security.

Third, are the vaults insured, and does the insurance policy cover the full replacement value of the stored metal? What happens in the event of theft, natural disaster, or vault operator default?

Fourth, how often are independent audits conducted, and are the results published or available to account holders? Reputable providers will welcome these questions. If a provider becomes evasive or dismissive when you ask about audit practices, that is a meaningful red flag.

Finally, what does it cost to convert from unallocated to allocated, or to take physical delivery of your metal? Understanding exit options before you commit ensures that you are not locked into an arrangement that does not serve your interests.

The Bottom Line for Gold Investors in 2026

In a world where gold is reaching record prices, central banks are accumulating metal at near-record pace, and interest rate dynamics continue to support safe-haven demand, the question of how your gold is stored has never been more relevant. The difference between allocated and unallocated gold storage is fundamentally a question of who actually owns the metal and what happens if something goes wrong.

Allocated storage costs more, but it provides the legal certainty and counterparty protection that most physical gold investors are looking for. Unallocated storage is cheaper and more liquid, but it introduces credit risk that can undermine the very reason many people buy gold in the first place.

As with most investment decisions, the key is to understand exactly what you are getting before you commit. Ask the hard questions, read the fine print, and make sure your storage arrangement genuinely matches your investment objectives.