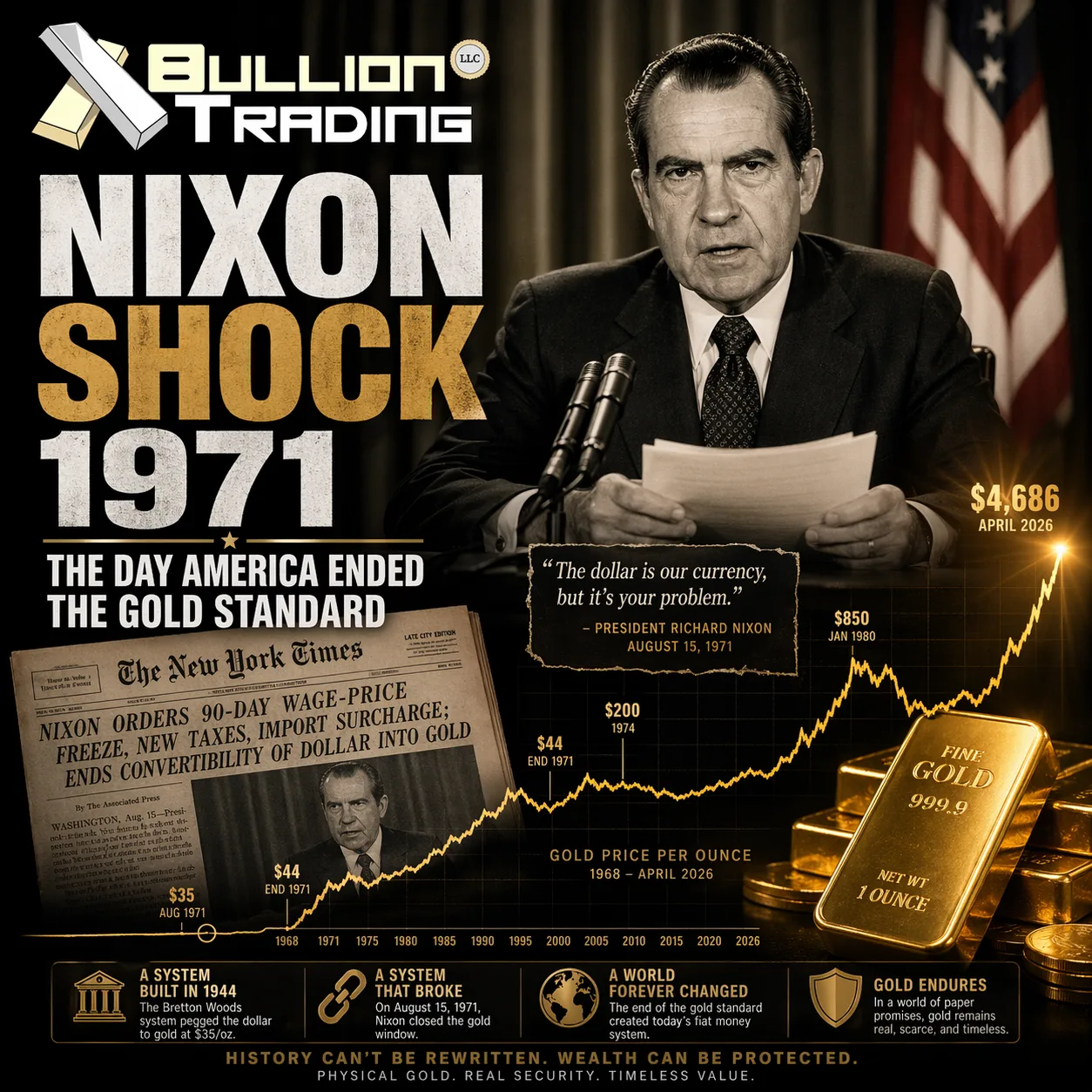

The night was August 15, 1971. Millions of Americans were at home watching television when President Richard Nixon took over the broadcast to deliver what he called his “New Economic Policy”. The speech lasted fifteen minutes. Its consequences have lasted more than fifty years. In one address, Nixon suspended the dollar’s convertibility into gold, tore up the international monetary framework that had governed the postwar world, and, without quite intending to, set gold on a course from $35 per ounce to the $4,686 it reached in April 2026.

History calls it the Nixon Shock. For gold investors, it is the founding event of the modern bullion market.

A System Built at the End of a World War

To understand why the Nixon Shock happened, you have to go back nearly three decades earlier, to the summer of 1944. As World War II was drawing toward its close, delegates from 44 nations gathered at the Mount Washington Hotel in Bretton Woods, New Hampshire, for the United Nations Monetary and Financial Conference. Their mission was to build a new international monetary order from scratch, one that would prevent the competitive currency devaluations and trade wars that had made the Great Depression so catastrophic.

The system they designed was elegant in its simplicity. The US dollar would be pegged to gold at a fixed price of $35 per ounce. Every other participating currency would then be fixed to the dollar within a band of one percent. Two new institutions, the International Monetary Fund and the World Bank, would supervise the system and lend support to countries running into balance-of-payments trouble. According to the Federal Reserve History, the IMF came into formal existence in December 1945 when the first 29 member countries signed its Articles of Agreement, and the system became fully functional in 1958 when currencies became freely convertible.

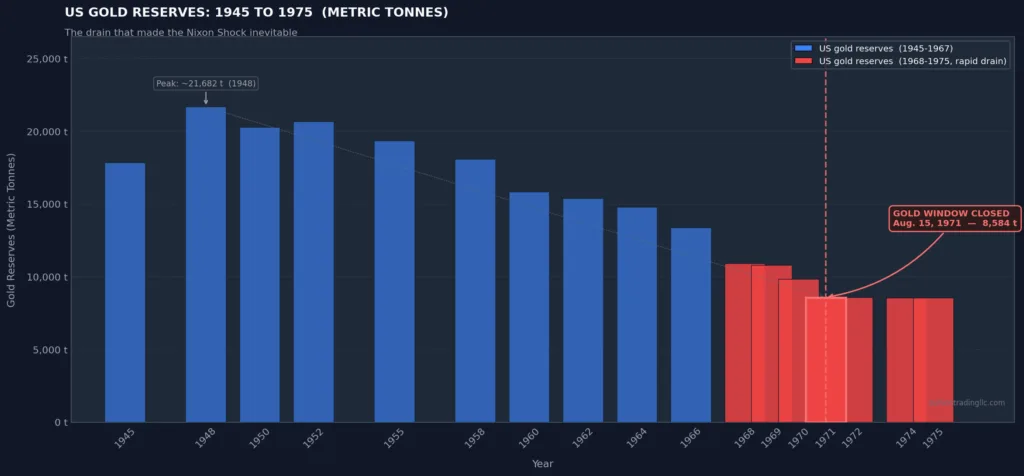

The United States was the natural anchor for this arrangement. Coming out of the war, America held roughly two thirds of the world’s monetary gold and produced about half of global economic output. The dollar was, in practical terms, as good as gold. For most of the late 1940s and 1950s, the system worked brilliantly, underpinning the postwar reconstruction of Europe and Japan and enabling extraordinary global growth.

The Triffin Dilemma: A Structural Flaw Nobody Could Fix

In 1960, a Belgian-American economist named Robert Triffin appeared before the US Congress and explained why the Bretton Woods system was, at its core, self-defeating. His argument was simple and devastating. For the world to grow and trade, it needed dollars, and lots of them. But the only way the United States could supply those dollars was by running persistent balance-of-payments deficits, pushing more currency out into the world than it took in. The problem was that the more dollars accumulated abroad, the more foreign governments would doubt the US had enough gold to redeem them all at $35 an ounce. The system was built on a contradiction that would eventually destroy it.

Through the 1960s, that contradiction deepened. Vietnam War spending, foreign aid, and the cost of maintaining American military bases across the globe pumped dollars into foreign hands at an accelerating pace. Presidents Kennedy and Johnson both tried to stem the outflow through foreign investment disincentives, interest rate schemes, and multilateral monetary negotiations. The US State Department’s Office of the Historian records that nothing worked.

France under President Charles de Gaulle was especially aggressive. De Gaulle famously criticized what he called the “exorbitant privilege” of the dollar’s reserve currency status and began systematically exchanging French dollar reserves for physical gold. When the London Gold Pool, a cooperative arrangement among central banks to hold the market price at $35, finally collapsed under the pressure in March 1968, authorities created a two-tier gold market: one official price for governments, one free-market price for everyone else. The architecture was crumbling. By August 1971, a full-scale speculative run on the dollar was underway, and the moment of reckoning had arrived.

The Camp David Weekend That Changed Everything

On Friday, August 13, 1971, Nixon quietly gathered his top economic advisers at the Camp David presidential retreat in the Maryland mountains. The meeting was kept strictly secret. According to the State Department’s historical account, those present included Secretary of the Treasury John Connally, a commanding Texan who would become the public face of the new policy, and Office of Management and Budget Director George Shultz. Conspicuously absent were Secretary of State William Rogers and National Security Adviser Henry Kissinger. This was an economic decision, made by economic people, and it would be announced before the rest of the world had time to react.

The secrecy was not incidental. Had word leaked before the announcement, the run on gold and the dollar would have become a stampede. Over two days of intense discussion, the group designed a package that would be revealed to the public before Asian financial markets opened on Monday morning. On Sunday evening, Nixon went on television.

The Three Pillars of Nixon’s New Economic Policy

Nixon framed his speech in the language of strength and self-defense, warning against the threat of “international money speculators” and calling on Americans to support a new era of economic confidence. Behind the rhetoric were three concrete and far-reaching measures.

The first was a 90-day freeze on wages and prices across the economy, an extraordinary peacetime intervention designed to break the inflationary spiral that had been building since the mid-1960s. The second was a 10 percent surcharge on all dutiable imports, a tariff meant to pressure America’s trading partners into letting their currencies rise against the dollar and opening their markets to US goods. The third, and most consequential for the global monetary order, was the immediate suspension of the dollar’s convertibility into gold.

The gold window was closed. Foreign governments could no longer present dollars to the Federal Reserve and receive gold in return at $35 an ounce. The anchor that had held the Bretton Woods system together for nearly three decades was gone, dissolved in a single presidential sentence.

The International Reaction and the Slow Death of Fixed Rates

The reaction abroad was immediate and unhappy. European and Japanese financial officials, who had not been consulted, scrambled to respond. The choice facing every major economy was stark: let their currencies float upward (making exports more expensive and less competitive), or keep buying dollars to defend their exchange rates (effectively importing American inflation). Most chose to float.

After months of fraught negotiations, the Group of Ten industrialized nations reached the Smithsonian Agreement in December 1971. The deal revalued currencies against a devalued dollar and raised the official gold price to $38 per ounce. Nixon declared it “the most significant monetary agreement in the history of the world”.It lasted fifteen months.

Speculative pressure returned in early 1973, forcing yet another devaluation. Within weeks, the system buckled again. In March 1973, the Group of Ten approved a new arrangement in which six members of the European Community tied their currencies together and jointly floated against the dollar. The Bretton Woods era was definitively over. The world had moved into the age of floating exchange rates, the regime that governs currency markets to this day.

Gold Unleashed: From $35 to $4,686

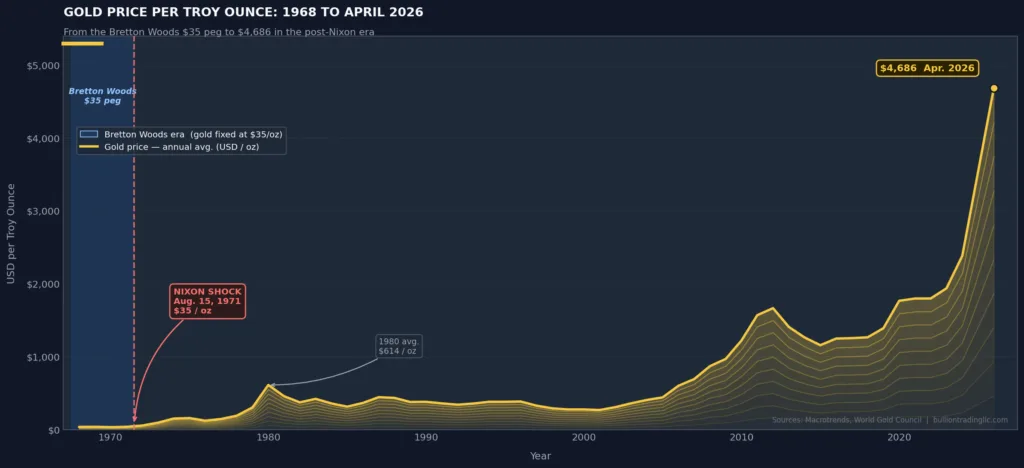

Perhaps the most dramatic consequence of the Nixon Shock was what it did to the price of gold. For more than two decades, gold had been artificially held at $35 per ounce by international agreement. Once that constraint was lifted, the market moved quickly to establish a very different value.

By the end of 1971, gold was trading in the mid-forties. By 1974, when Congress finally ended the four-decade American ban on private gold ownership and US citizens could legally buy bullion again, prices were approaching $200 per ounce. The 1970s brought persistent inflation, two oil shocks, and geopolitical crises, all powerful tailwinds for gold. By January 1980, gold hit an intraday peak of $850 per ounce, representing a 24-fold increase from its Bretton Woods price in under a decade.

The decades that followed saw gold correct, stabilize through the 1980s and 1990s, and then surge again with the financial crisis of 2008, the pandemic money-printing of 2020, and the geopolitical tensions of the mid-2020s. As of April 2026, gold trades at approximately $4,686 per ounce, according to the World Gold Council. That is an increase of more than 13,000 percent from the $35 peg that Nixon abandoned on that August evening in 1971. The dollar, meanwhile, has lost the vast majority of its purchasing power over the same period.

Why the Nixon Shock Still Matters for Gold Investors in 2026

The Nixon Shock matters to anyone holding physical gold today not simply as history but as context. It was the moment when the last formal link between paper money and a tangible asset was severed. Every dollar, euro, yen, and pound in circulation today is backed by nothing more than a government’s promise and a central bank’s credibility. That is the world the Nixon Shock created.

For decades, that arrangement worked well enough, held in place by institutional credibility and disciplined monetary policy. But since the 2008 financial crisis, and especially since 2020, governments and central banks have expanded money supplies at a scale that would have been unimaginable under a gold constraint. The Federal Reserve’s own data shows total assets growing from under $1 trillion in 2007 to a peak of more than $8 trillion in 2022. National debt levels across the developed world are at peacetime records. The structural forces that drove gold from $35 in 1971 remain very much alive.

Central banks themselves appear to have drawn their own conclusions. According to the World Gold Council, central bank gold purchases have exceeded 1,000 tonnes per year for three consecutive years through 2025, a pace of accumulation not seen since the Bretton Woods era itself. They are, in a quiet way, rebuilding a relationship with gold that Nixon dismantled more than half a century ago.

For individual investors, understanding the Nixon Shock means understanding the fundamental reason gold belongs in a portfolio. In a world where money can be created at will by governments, gold remains the one form of monetary asset that cannot be printed, diluted, or defaulted on.

Conclusion: A Hinge in History

August 15, 1971 was not just a policy decision; it was a turning point in how money works. Nixon did not set out to dismantle the Bretton Woods system. He set out to protect America’s economy from a currency crisis that had become impossible to contain. The unintended consequence was a global monetary order with no formal anchor at all, and gold’s 55-year march from $35 to $4,686 is the clearest measure of what that shift has meant in practice.

The Nixon Shock is, above all, an origin story. It explains why gold is not simply a commodity or a collectible but a monetary asset with a specific role to play in preserving wealth when the paper alternatives come under pressure. That role has not diminished. If anything, the monetary environment of 2026, with sovereign debt at historic highs and central banks quietly accumulating gold, suggests it has only grown more relevant.