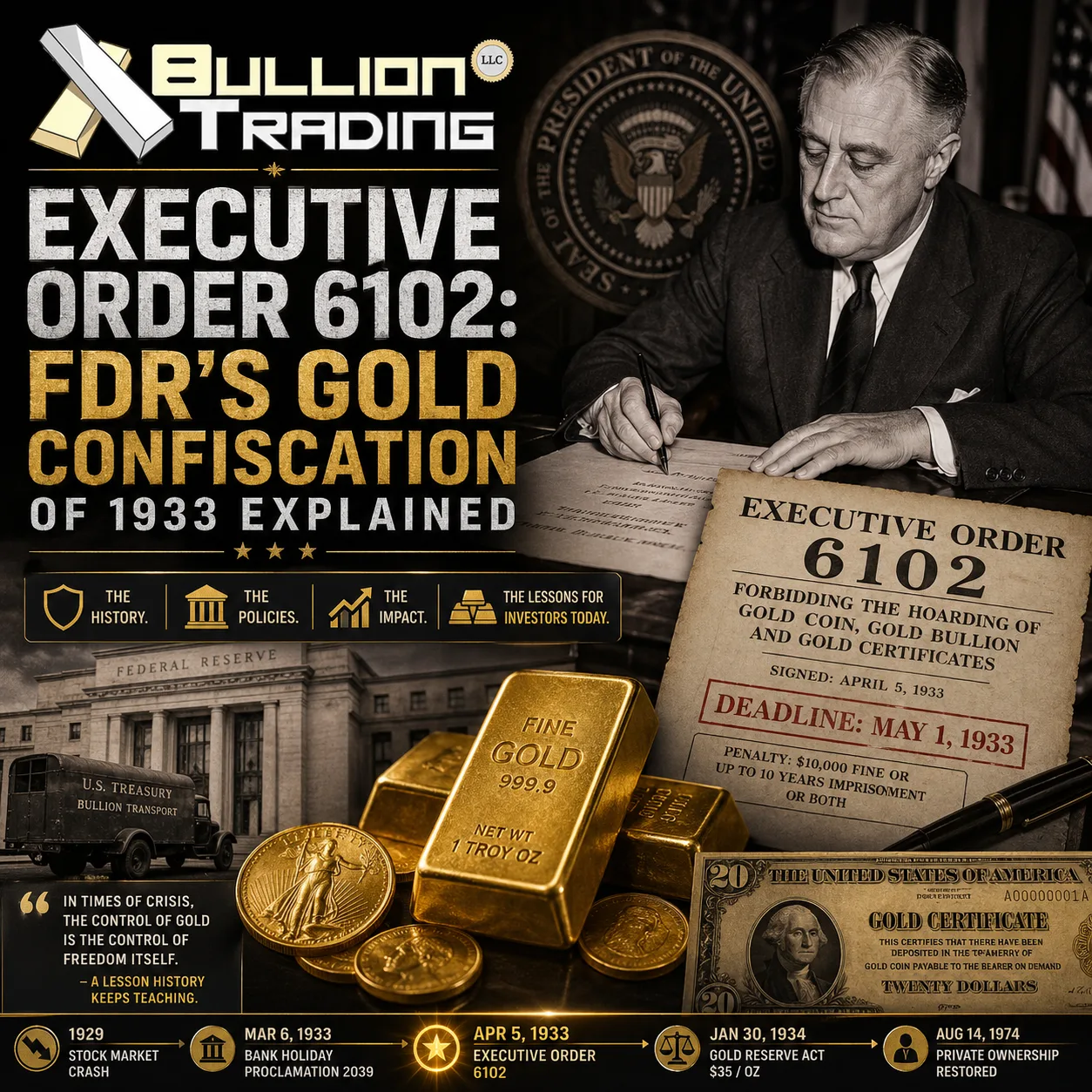

On April 5, 1933, President Franklin D. Roosevelt signed a document that would fundamentally alter the relationship between Americans and their gold. Executive Order 6102 gave every person in the country roughly 25 days to hand over their gold coins, gold bullion, and gold certificates to the nearest Federal Reserve Bank or member bank. Failure to comply carried penalties that sound almost unbelievable today: a fine of up to $10,000 and up to ten years in prison.

Understanding how this happened, and why, tells us a great deal about the fragility of the gold standard under extreme economic stress, the realities of monetary crisis management, and why gold has remained a subject of deep interest for investors ever since. The story is more nuanced than the word “confiscation” implies, and getting the details right matters both historically and for anyone thinking about gold as part of a long-term portfolio strategy.

The Crisis That Set Everything in Motion

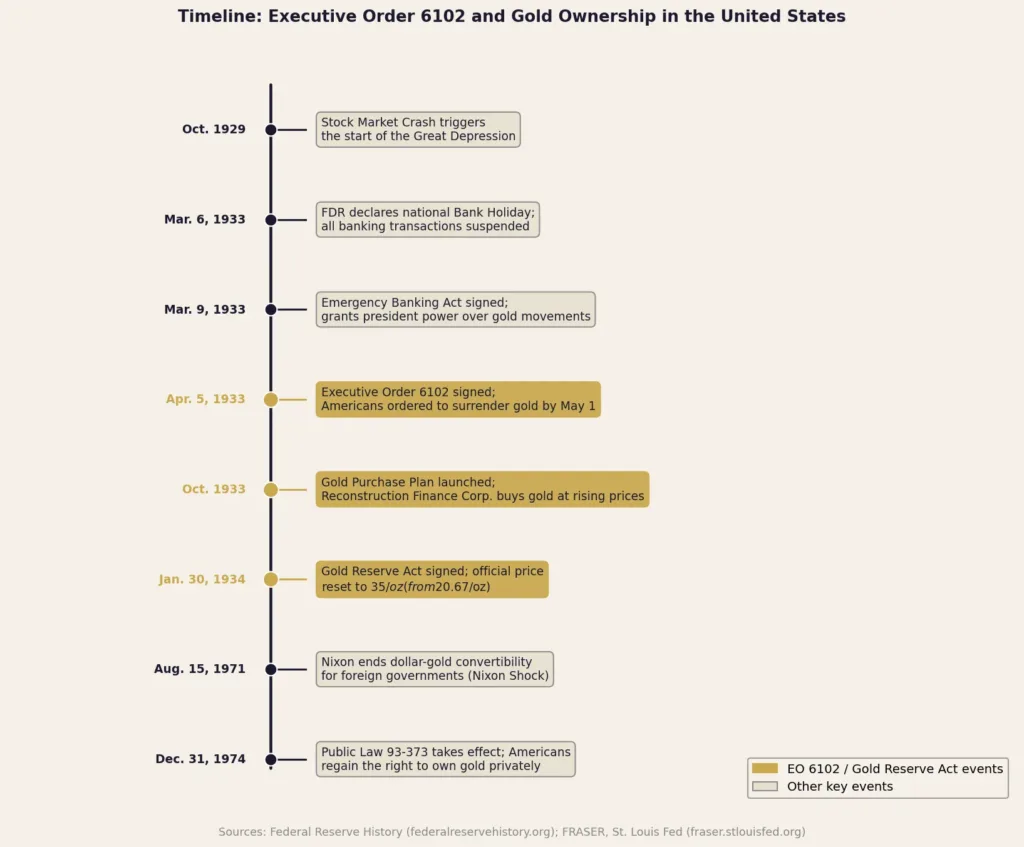

The story of Executive Order 6102 cannot be told without understanding the economic catastrophe that preceded it. By early 1933, the United States had been grinding through the Great Depression for more than three years. Thousands of banks had already failed across the country, and a fresh wave of bank runs was accelerating through January and February of that year, pushing the financial system toward total collapse.

The Federal Reserve had been operating on a gold standard since it began operations in 1914, required by law to hold gold reserves equal to at least 40 percent of the currency it issued and to redeem paper dollars for gold at a fixed price of $20.67 per troy ounce. As panic spread, Americans increasingly preferred holding actual gold over bank deposits or paper currency. Foreign investors, fearing a devaluation of the dollar, were simultaneously converting their dollar holdings into gold at an alarming pace. Both drains together consumed the Federal Reserve’s legally required reserves.

By March 1, 1933, the Federal Reserve Bank of New York’s gold reserves had fallen below the legal minimum. Governor George L. Harrison sent an urgent message to Washington stating bluntly that he would “no longer take responsibility” for running the New York Reserve Bank with deficient reserves. The system was on the edge.

Just 36 hours after his inauguration, Roosevelt issued Proclamation 2039 on March 6, 1933, ordering the suspension of all banking transactions. Every bank in America went dark. Three days later, on March 9, Congress passed the Emergency Banking Act, which among other provisions granted the president broad authority to regulate gold movements and gave the Treasury Secretary the power to compel the surrender of gold coins and certificates. When banks reopened on March 13, the immediate panic subsided. But gold continued flowing out of the system, and the administration moved to address it permanently.

What Executive Order 6102 Actually Said

The executive order was signed on April 5, 1933, and transmitted by the Federal Reserve Bank of New York to all banking institutions the following day. Its official title was simply “Forbidding the Hoarding of Gold Coin, Gold Bullion and Gold Certificates”. The legal authority it cited was Section 5(b) of the Trading with the Enemy Act of 1917, as amended by the Emergency Banking Act, a wartime statute that gave the president sweeping powers over economic activity during declared emergencies.

The core requirement was unambiguous. Section 2 of the order required every person in the continental United States, individuals, businesses, partnerships, and corporations, to deliver all gold coin, gold bullion, and gold certificates to a Federal Reserve Bank or member bank by May 1, 1933. In return, they would receive the equivalent value in paper currency at the official monetary rate of $20.67 per troy ounce.

The penalties for willful violation were severe. Section 9 of the order stated that violators could be “fined not more than $10,000, or, if a natural person, may be imprisoned for not more than ten years, or both”. In 1933 terms, a $10,000 fine was an enormous sum, equivalent to roughly $240,000 in 2026 dollars. The order also specified that any officer, director, or agent of a corporation who knowingly participated in a violation could be punished identically.

The Exceptions: Who Could Keep Their Gold

Executive Order 6102 was not an absolute confiscation of every ounce of gold in the country. The order carved out four specific categories of exempt gold, and understanding them matters for anyone studying the history of precious metals regulation.

Individuals were permitted to retain gold coin and gold certificates up to an aggregate value of $100, a modest personal allowance equivalent to roughly 4.8 troy ounces at the time. More significantly for collectors and investors, the order explicitly exempted “gold coins having a recognized special value to collectors of rare and unusual coins”. This numismatic exemption protected genuinely rare coins from forced surrender and is the direct ancestor of the collector coin carve-outs that appear in modern precious metals discussions.

Gold held for legitimate industrial, professional, or artistic use was also exempt, as was gold held in trust for foreign governments or recognized foreign central banks. The industrial exemption explains why the Federal Reserve Bank of Cleveland was still supplying gold bars to manufacturers as late as July 1933. As the Federal Reserve’s own historical records document, the Columbus Dental Manufacturing Company applied for and received 29 gold bars totaling 476.92 ounces in late July of that year, a legal transaction under the industrial exemption.

The Price Americans Were Paid and What Happened Next

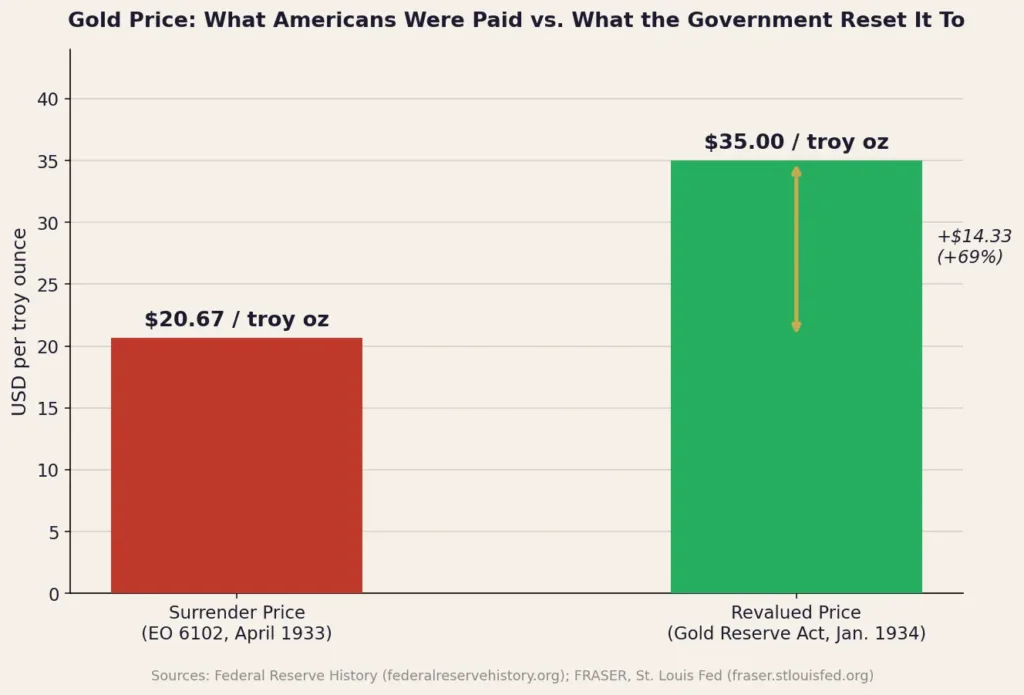

The compensation question is where the historical controversy sharpens. Americans were paid $20.67 per troy ounce, the official monetary price that had been fixed since the Gold Standard Act of 1900. On the surface this appeared to be fair market value since it was the same rate the government had always honored. But what followed made the situation considerably more complicated.

Beginning in October 1933, the Roosevelt administration launched what it called the gold purchase plan. The government authorized the Reconstruction Finance Corporation to buy gold at progressively higher prices, deliberately devaluing the dollar by raising the dollar price of gold. Then, on January 30, 1934, Roosevelt signed the Gold Reserve Act, which formally transferred all monetary gold in the United States to the Treasury and reset the official gold price at $35 per troy ounce. This new rate, as the Federal Reserve’s historical analysis notes, “reduced the gold value of the dollar to 59 percent of the value set by the Gold Standard Act of 1900”.

In practical terms, the gold that Americans had surrendered at $20.67 per ounce was revalued to $35 just nine months later, an increase of roughly 69 percent. The paper dollars citizens received in exchange were immediately worth only about 59 cents on the gold dollar once the new rate was established. The Treasury, meanwhile, booked a substantial accounting profit on its newly accumulated gold holdings. This sequence is the primary source of the historical criticism of EO 6102: the government collected the nation’s gold at one price, then repriced it sharply higher for its own benefit.

The Historical Debate: Necessary Emergency or Government Overreach?

Critics at the time called Roosevelt’s gold policies “completely immoral” and described them as a “flagrant violation of the solemn promises” made to purchasers of Liberty and Victory Loans during World War I. They argued the policies would trigger dangerous credit expansion and eventually produce an even worse speculative collapse than the one the country was already living through.

Economic historians have reached a more measured judgment. As the Federal Reserve’s own historical analysis of Roosevelt’s gold program concludes, scholars who studied the episode, including Milton Friedman and Anna Schwartz in their landmark 1963 work A Monetary History of the United States, as well as economists Ben Bernanke and Christina Romer, generally concluded that reflating the economy accelerated recovery from the Great Depression. Research by economists Barry Eichengreen and Jeffrey Sachs demonstrated that countries which suspended the gold standard and reflated their economies began recovering earlier than those that did not.

The key tension is real and should be acknowledged honestly. Executive Order 6102 was an exercise of extraordinary executive power over private property, implemented under genuine emergency conditions. The order’s practical effect on compliance appears to have been primarily psychological, the combination of banking crisis exhaustion, fear of criminal penalties, and genuine patriotism drove most people to comply without systematic enforcement. The numismatic coin exemption, in particular, was loosely defined, and many collectors retained their holdings throughout the period without prosecution. The line between a “rare coin” and an ordinary gold coin was never precisely established by the courts.

What Came After: The Gold Reserve Act and the Road to $35

The Gold Reserve Act of January 30, 1934 was the formal culmination of everything the administration had set in motion through EO 6102. Beyond setting the new $35 price, the Act transferred ownership of all monetary gold to the Treasury, prohibited the Treasury and financial institutions from redeeming dollars for gold, and established the Exchange Stabilization Fund, a $2 billion reserve, funded by the Treasury’s profit on revaluing gold, that gave the administration tools to manage foreign exchange without Federal Reserve involvement.

As the Federal Reserve Bank of New York’s Governor George Harrison later noted, the Gold Reserve Act effectively stripped the Federal Reserve of its independent monetary policy role. The Washington Post described it plainly: “The gold reserve act of 1934 not only took from the system all of its gold, but in doing so definitely deprived it of future control over gold movements”. The Fed would not regain meaningful control over monetary policy until the Fed-Treasury Accord of 1951.

When Americans Got Their Gold Back

The ban on private gold ownership remained in place for over four decades, long after the monetary architecture that had justified it had itself been dismantled. On August 15, 1971, President Nixon ended dollar-to-gold convertibility entirely, severing the dollar’s last link to gold and letting it trade freely on international markets. Yet private American citizens still could not legally own gold beyond the old limits.

It was not until August 14, 1974, that President Gerald Ford signed Public Law 93-373, which authorized Americans to own gold effective December 31, 1974. Ford also signed Executive Order 11825 on December 31, 1974, effective January 1, 1975, formally revoking the executive orders that had restricted gold ownership. By that time, as Federal Reserve historians note, gold had already been trading as a free-market commodity internationally, with prices far above the old $35 ceiling. Gold was trading above $180 per ounce when Ford acted, and it would go on to reach $850 by January 1980. The forty-one years of restricted ownership had ended, and the modern era of private gold investment in the United States had begun.

What This History Means for Gold Investors Today

Executive Order 6102 surfaces regularly in precious metals investment discussions, usually as a warning that the government could “confiscate gold again”. A careful reading of the historical record suggests a more nuanced framing. The 1933 order arose from a very specific monetary architecture, a gold standard that legally required the government to exchange paper dollars for physical gold on demand. When gold drained from the Federal Reserve’s vaults faster than it could be replenished, the government faced a genuine technical insolvency in its monetary obligations. That specific architecture, and the specific vulnerability it created, no longer exists. Gold has been a freely traded commodity for fifty years, and no dollar-to-gold conversion obligation is in place today.

That said, the episode is a genuine reminder that governments have historically used their legal authority over gold during periods of monetary stress, and that the legal framework surrounding precious metals can change. It also illuminates something timeless: the very reason governments in 1933 felt compelled to collect the nation’s gold is the same reason gold remains valuable as a portfolio asset in 2026. Gold represented an independent claim on value outside the paper money system, and that is precisely what investors have sought in it throughout history.

Understanding the difference between the conditions of 1933 and today is important. So is understanding that gold’s core appeal, its independence from any single government’s monetary decisions, is not a recent invention. It is the quality that has made gold worth protecting across every monetary regime of the last century.

Conclusion: An Episode That Still Resonates

Executive Order 6102 was the product of a genuine financial emergency, a collapsing banking system, a gold drain that threatened the Federal Reserve’s legal reserve requirements, and a new administration prepared to use extraordinary measures to break the deflationary spiral of the Great Depression. The order was carefully constructed, with exemptions for industrial users, coin collectors, and foreign governments, and it was followed by a broader monetary restructuring that most economic historians regard as having accelerated America’s recovery.

At the same time, it resulted in a measurable transfer of wealth from gold holders to the Treasury: Americans surrendered their gold at $20.67 per ounce and received paper dollars that were worth 59 cents on the gold dollar nine months later. Both things are true, and the history does not need to be simplified in either direction to be interesting or instructive.

For investors in 2026, the most lasting lesson from Executive Order 6102 may be this: gold’s role as an independent store of value and its occasional inconvenience to paper money systems are not separate facts. They are the same fact, seen from different angles. That duality is precisely what has made gold one of the most studied, most debated, and most enduring assets in the history of money.