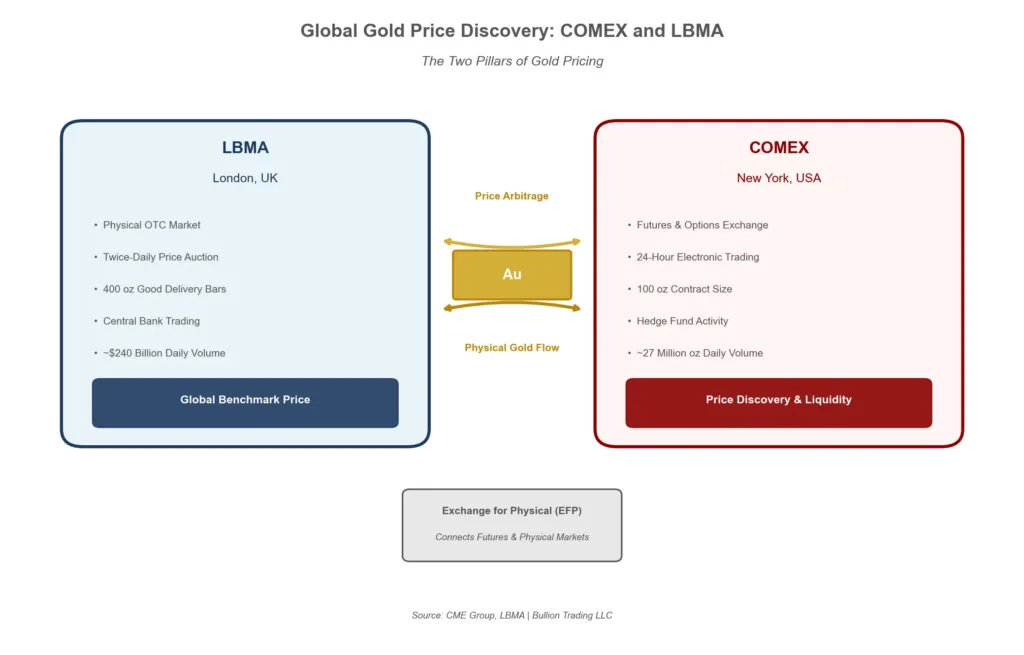

When you check the gold price on any financial website, you’re seeing the result of a complex interplay between two major global markets. The COMEX in New York and the LBMA in London together form the backbone of worldwide gold price discovery. Understanding how these two markets function, and how they relate to each other, gives investors valuable insight into what actually drives the price of gold.

Whether you’re buying a single gold coin or managing a significant precious metals portfolio, the prices you encounter trace back to activity in these two interconnected hubs. Let’s break down how each market works and why both matter for anyone interested in gold.

The London Bullion Market Association: Setting the Global Benchmark

The London Bullion Market Association (LBMA) represents the wholesale physical gold market, and its twice-daily benchmark price serves as the reference point for gold transactions worldwide. This isn’t an exchange in the traditional sense. Instead, the London gold market operates as an over-the-counter (OTC) marketplace where major banks, refiners, mining companies, and central banks trade directly with each other.

The current LBMA Gold Price auction, administered by ICE Benchmark Administration (IBA), replaced the historic “London Gold Fix” in March 2015. The old fixing process had been running since 1919, but concerns about transparency led to the creation of the modern electronic auction system.

How the LBMA Gold Price Auction Works

The auction occurs twice daily at 10:30 AM and 3:00 PM London time. The process is remarkably straightforward in concept, though the execution requires sophisticated coordination among major financial institutions.

The auction chairperson, provided by ICE Benchmark Administration, starts each session by proposing an opening price based on current market conditions. The 12 direct participants, which include major bullion banks like HSBC, JP Morgan, UBS, Goldman Sachs, and Bank of China, then submit buy or sell orders into the system.

Each auction round lasts 30 seconds. If buy and sell orders don’t balance within a tolerance of 10,000 ounces (roughly 25 standard gold bars), the price adjusts and a new round begins. This continues until equilibrium is reached. The final price becomes the LBMA Gold Price, used as a benchmark for settling gold contracts, valuing gold-backed ETFs, and pricing physical gold transactions globally.

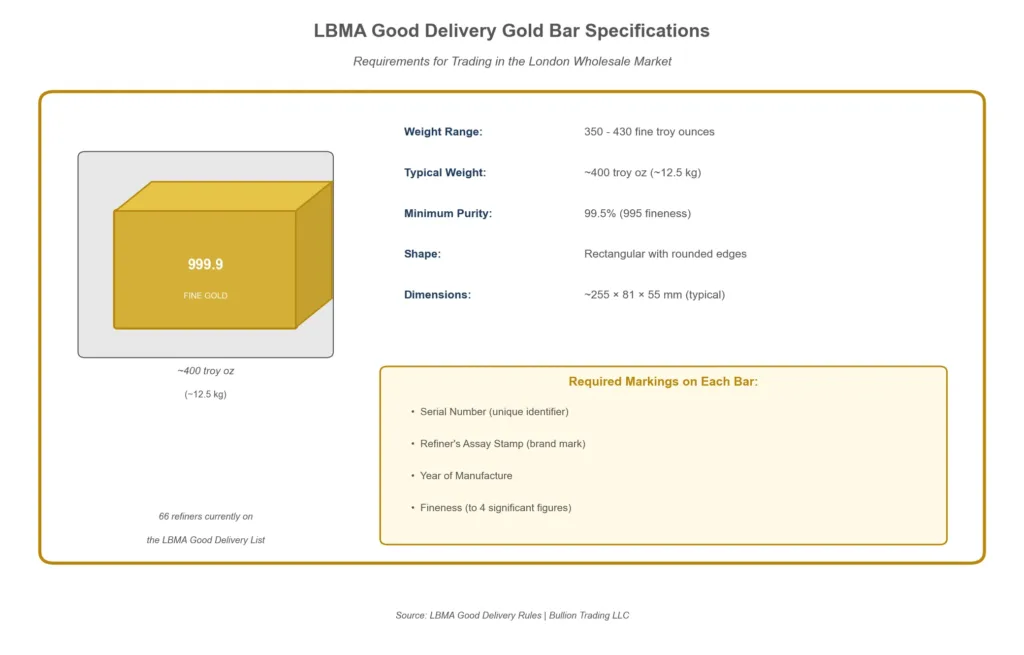

According to the LBMA’s Guide to the Loco London Precious Metals Market, trades in the London market settle using a concept called “loco London,” meaning the gold is priced and delivered in London, with physical delivery taking the form of 400-ounce Good Delivery bars.

Understanding LBMA Good Delivery Standards

Not just any gold bar can trade in the London wholesale market. The LBMA maintains strict Good Delivery standards that specify requirements for weight, purity, and appearance. A London Good Delivery gold bar must weigh between 350 and 430 fine ounces (typically around 400 ounces or 12.5 kilograms) and have a minimum purity of 99.5%.

Only refiners that have passed LBMA accreditation appear on the Good Delivery List. Currently, 66 gold refiners worldwide hold this accreditation, including well-known names like Argor-Heraeus, Metalor Technologies, MKS PAMP, Valcambi, the Royal Canadian Mint, and the Perth Mint. Bars from these refiners command full liquidity in the wholesale market, while bars from non-accredited sources trade at discounts or require re-assaying.

COMEX: The Futures Market Driving Price Discovery

While London handles the physical wholesale market, the COMEX division of the CME Group in New York dominates gold futures trading. According to Investopedia, COMEX futures trades the equivalent of nearly 27 million ounces daily, making it the most liquid gold trading venue in the world.

COMEX was founded in 1933 through the merger of several New York commodity exchanges. It joined forces with the New York Mercantile Exchange (NYMEX) in 1994 and became part of CME Group in 2008. Today, the exchange operates electronically through CME Globex, with trading available nearly 24 hours per day from Sunday evening through Friday afternoon.

COMEX Gold Futures Contract Specifications

The standard COMEX gold futures contract, designated “GC,” represents 100 troy ounces of gold. According to CME Group’s contract specifications, prices are quoted in U.S. dollars and cents per troy ounce, with minimum price fluctuations of $0.10 per ounce ($10 per contract).

Contracts are listed for the current month, the next two calendar months, and any February, April, August, and October falling within a 23-month period, plus any June and December falling within a 72-month period. This structure allows traders and hedgers to lock in prices far into the future.

Physical delivery is possible for traders who hold positions through expiration. Gold delivered against COMEX contracts must be in the form of 100-ounce bars or three one-kilogram bars, stored at COMEX-approved depositories in the New York area. However, less than 1% of contracts actually result in physical delivery. Most traders close out positions before expiration or roll them into later contract months.

How COMEX and LBMA Prices Interact

Though separated by an ocean, the COMEX and LBMA markets operate in continuous dialogue. When one market opens, it inherits pricing from the other. As both are open during overlapping hours (typically 8:00 AM to 1:30 PM Eastern Time when both London afternoon and COMEX sessions run), arbitrageurs work to keep prices aligned between the two venues.

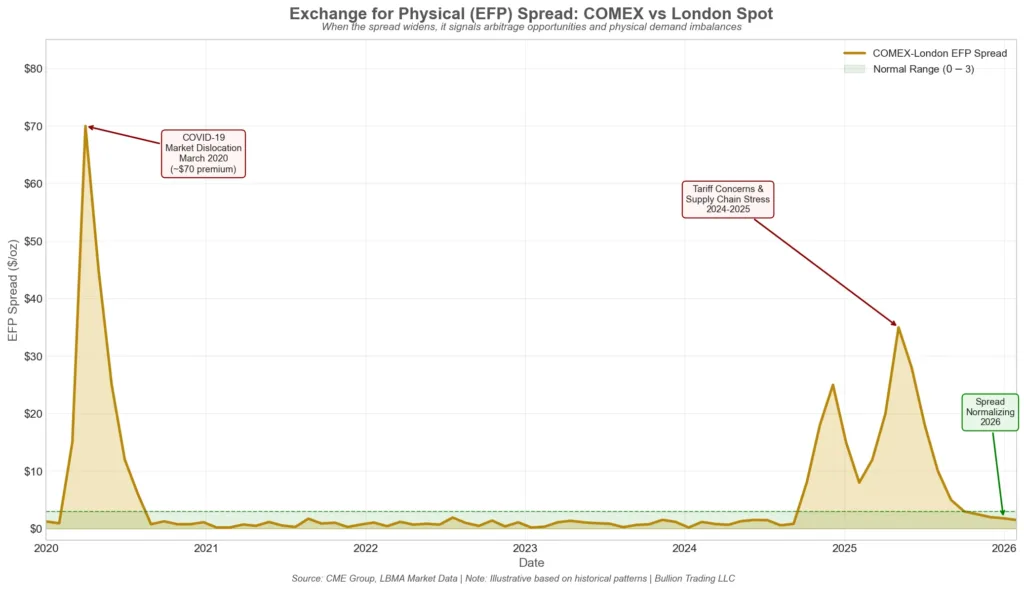

This arbitrage mechanism is formalized through a process called Exchange for Physical (EFP). An EFP transaction allows a trader to swap a COMEX futures position for physical gold in London, or vice versa. The EFP spread, which represents the price difference between COMEX futures and London spot, fluctuates based on supply and demand dynamics in each market.

Under normal conditions, the EFP spread stays within a narrow range. However, during periods of market stress or unusual demand for physical metal in one location, this spread can widen dramatically. When COMEX trades at a significant premium to London, it signals strong U.S. demand and encourages gold to flow eastward from London to New York vaults. When the relationship reverses, metal flows back across the Atlantic.

Why Both Markets Matter for Gold Investors

Understanding the dual nature of gold pricing helps investors interpret market signals and make informed decisions. The LBMA Gold Price provides a transparent, auditable benchmark that’s used to price everything from central bank gold reserves to gold-backed ETFs like the SPDR Gold Shares (GLD).

COMEX futures, meanwhile, offer insights into market sentiment and positioning. The Commitment of Traders reports published weekly by the CFTC reveal how different categories of traders, including hedge funds, managed money, and commercial hedgers, are positioned in gold futures. Large speculative long positions might suggest bullish sentiment, while heavy commercial hedging could indicate producer concerns about future prices.

Key Differences Between the Markets

The London and New York markets serve different but complementary functions. London is primarily a physical market where actual metal changes hands, typically in 400-ounce bars. The participants are mostly institutional: bullion banks, central banks, refiners, and mining companies.

COMEX provides a regulated futures market with standardized contracts, central clearing, and the ability to trade on margin. While physical delivery is possible, most participants are using futures for price exposure or hedging rather than acquiring actual metal. The leverage available in futures markets means small price movements can generate significant gains or losses.

For retail investors buying physical gold coins and bars, both markets matter. Dealers price their products based on the spot price (derived from London) plus a premium that reflects manufacturing costs, dealer margins, and current supply-demand conditions for that specific product form.

The Role of Central Banks and Institutional Players

Central banks are major participants in both markets, though they typically favor the London physical market for building or reducing gold reserves. According to World Gold Council data, central bank gold purchases have remained elevated in recent years, with many emerging market central banks diversifying reserves away from dollar-denominated assets.

The Bank of England plays a unique role in the London market. Its vault, located beneath its headquarters on Threadneedle Street, holds gold on behalf of approximately 72 customers, including central banks, international institutions, and LBMA member bullion banks. Transfers between accounts at the Bank of England occur through book entry rather than physical movement of bars, making it an efficient mechanism for settling large wholesale transactions.

Market Transparency and Regulation

Both markets have evolved toward greater transparency in recent years, though challenges remain. The LBMA Gold Price auction replaced the secretive “Gold Fix” telephone conference that had operated for nearly a century. The new system publishes real-time data during auctions and maintains audit trails.

COMEX operates under the regulatory oversight of the Commodity Futures Trading Commission (CFTC), with rules governing position limits, reporting requirements, and market manipulation. Daily trading data, open interest figures, and delivery reports are publicly available through the CME Group website.

However, the over-the-counter nature of the London market means that trading volumes between LBMA members remain largely undisclosed. The LBMA publishes monthly clearing statistics showing gold transfers between the five members of London Precious Metals Clearing Limited (LPMCL), but these represent netted positions rather than total trading activity.

Practical Implications for Gold Buyers

For investors purchasing physical gold from dealers like Bullion Trading LLC, understanding these markets provides useful context for interpreting prices. The spot price you see quoted represents current pricing in the London market, typically expressed as “loco London” for immediate delivery of unallocated gold.

When you buy a gold coin or bar, you pay the spot price plus a premium. This premium varies based on product type, with popular coins like American Gold Eagles or Canadian Gold Maple Leafs typically carrying higher premiums than generic bars due to brand recognition and collector demand.

During periods of high demand or supply chain stress, premiums can expand significantly as dealers compete for available inventory. Understanding that the underlying spot price reflects wholesale market conditions, while retail premiums reflect the specific dynamics of coin and bar production and distribution, helps investors evaluate whether current premiums represent normal conditions or unusual market stress.

Looking Ahead: The Evolution of Gold Price Discovery

The gold market continues to evolve. The Shanghai Gold Exchange has grown to become the world’s largest physical gold exchange by trading volume, introducing the possibility that Asian trading will play an increasing role in global price discovery. The SGE’s yuan-denominated gold benchmark offers an alternative reference price for the growing Chinese market.

Digital innovations, including blockchain-based gold tokens and expanded gold ETF offerings, create new mechanisms for gold exposure without physical delivery. These products typically reference LBMA or COMEX prices for their underlying value.

For investors, the fundamental dynamics remain unchanged. COMEX and LBMA gold pricing represent the intersection of supply and demand across the world’s two largest gold trading centers. Whether you’re tracking gold as a portfolio hedge, an inflation protection strategy, or simply following a fascinating market, understanding how these prices are determined provides essential foundation knowledge.

The interplay between London’s physical market and New York’s futures complex will continue to drive gold prices for the foreseeable future. By understanding both markets, investors can better interpret price movements, evaluate product premiums, and make informed decisions about when and how to add gold to their portfolios.