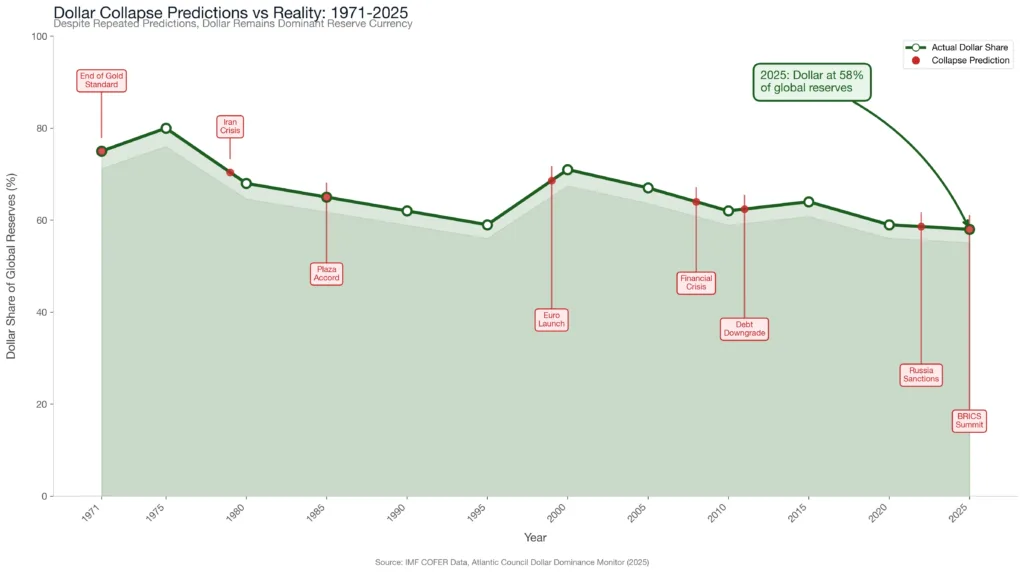

For decades, the prediction has remained remarkably consistent: the US dollar is about to collapse, and only gold can save you. The argument typically follows a familiar pattern. Money must be backed by gold, and if it is not, it will eventually go to zero. This narrative has persisted through multiple administrations, economic cycles, and global crises. Yet here we are in December 2025, and the dollar remains the world’s dominant reserve currency.

At Bullion Trading LLC, we have been recommending gold for years because gold absolutely has an important role in a well-structured portfolio. But we also believe in honest analysis over fear-based marketing. Understanding the real reasons to own gold, and the real dynamics behind currency systems, matters more than repeating predictions that have failed to materialize for generations.

What History Actually Shows About Dominant Currencies

When you look at how currencies have functioned across centuries, a consistent pattern emerges that contradicts the simplistic “gold backing equals value” narrative. The dominant power of each era had a currency that traded at a premium, and this premium existed even when other regions possessed more gold and silver.

Roman denarii were imitated across the ancient world. Byzantine solidus coins were copied throughout the Mediterranean for centuries. Venetian ducats became the standard for international trade during the Italian Renaissance. In many cases, the imitations contained equal or even more gold than the originals. Yet the originals still carried more value. Why? Because they came from the financial center of their era. What mattered was not just the metal content but who issued the currency and where the capital markets were located.

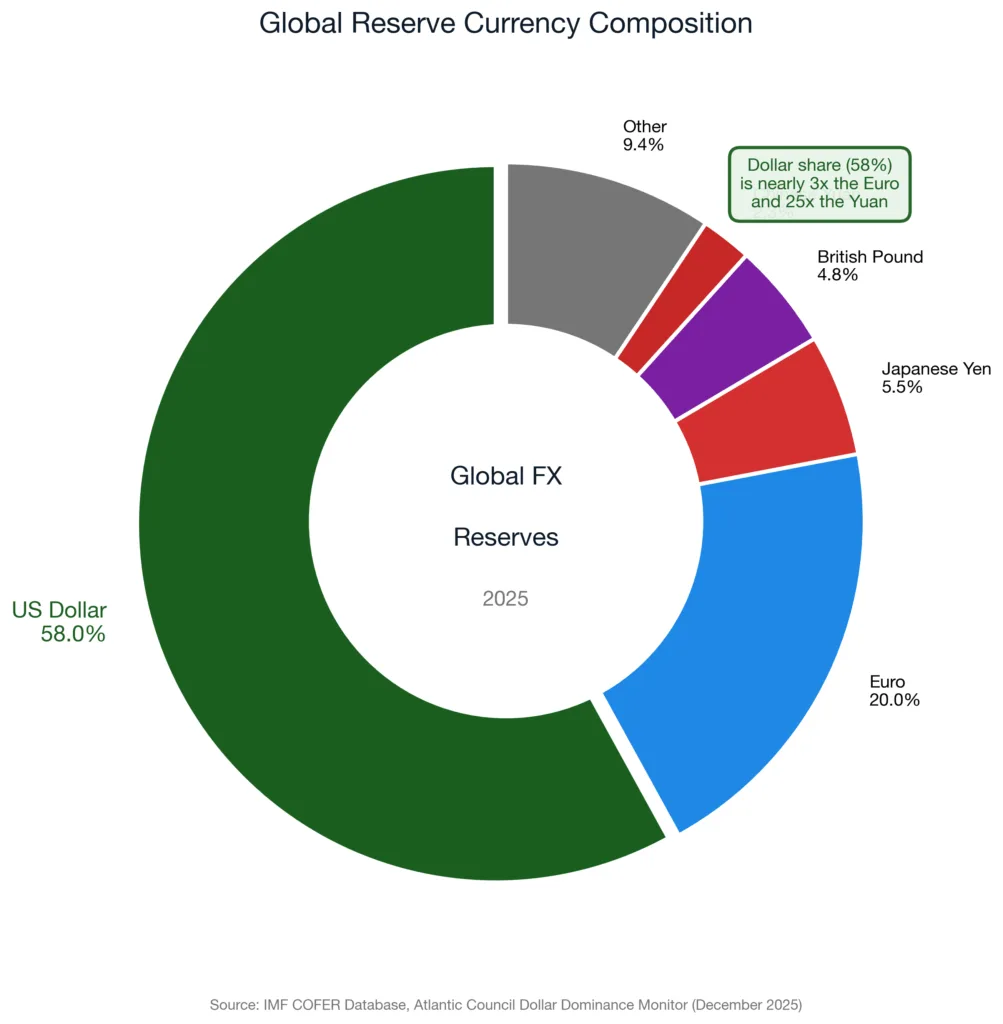

According to research from the Atlantic Council’s GeoEconomics Center, this pattern continues today. The US dollar represents approximately 58 percent of foreign reserve holdings worldwide. The euro, the second most used currency, accounts for only 20 percent. This dominance persists not because of ideology or tradition but because of practical realities that alternatives simply cannot match.

The Real Source of Currency Value

The real wealth of a nation has never been its gold reserves alone. It is the productivity of its people, the ability to create and trade, and the capacity to attract capital. This explains something that gold-backed-money advocates struggle to address: how countries devastated after World War II were able to rebuild into economic powerhouses without relying on gold backing.

The Bretton Woods system established in 1944 created a new international monetary framework, but the reconstruction of Germany, Japan, and other war-torn economies did not depend on those countries accumulating gold reserves. It depended on rebuilding productive capacity, establishing stable institutions, and integrating into global trade networks. When President Nixon ended dollar convertibility to gold in 1971, many predicted catastrophe. Instead, the dollar’s dominance continued because the underlying fundamentals remained intact.

The United States has the deepest and most liquid capital markets in the world. According to SIFMA’s 2025 Capital Markets Fact Book, global fixed income markets outstanding reached $145.1 trillion in 2024, with US markets representing a dominant share. Global equity market capitalization hit $126.7 trillion. When someone needs to deploy billions of dollars efficiently, there is really only one place that can absorb that kind of capital at scale.

Why Dollar Collapse Predictions Keep Failing

Every time the dollar has not collapsed, the prediction simply evolves. First it was the end of gold backing in 1971. Then it was the petrodollar system. Then the euro was supposed to replace dollar dominance. Now it is BRICS. Yet none of these alternatives offer what actually matters: scale, liquidity, and trust in capital markets.

The Atlantic Council’s Dollar Dominance Monitor provides current analysis on this dynamic. Their research shows that even countries that publicly criticize the dollar still borrow in dollars, issue dollar-denominated debt, and park capital in US markets. The 2025 BRICS Summit in Brazil made little mention of de-dollarization, with member nations facing some of the highest US tariff rates globally becoming hesitant to publicly challenge dollar dominance.

As the Atlantic Council notes: “The dollar’s role as the primary global reserve currency remains secure in the near and medium term. The dollar continues to dominate foreign reserve holdings, trade invoicing, and international currency transactions. All potential rivals, including the euro, have a limited ability to challenge the dollar in the immediate future.”

This is not cheerleading for the dollar. It is simply recognizing that currency systems change when capital flows change, not because of political rhetoric or slogans. The dominance of a reserve currency reflects underlying economic realities that cannot be wished away.

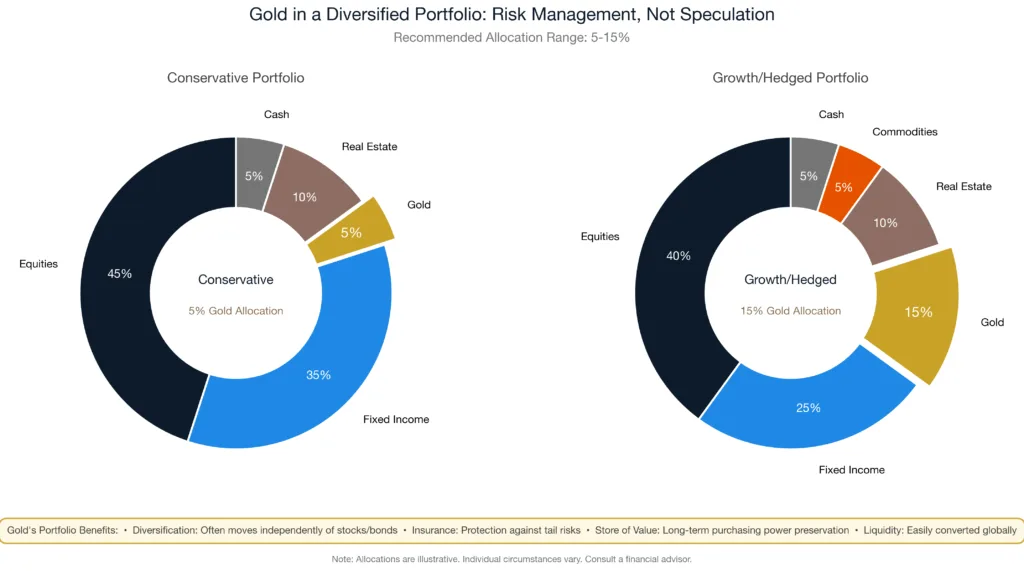

Where Gold Actually Fits in Portfolio Strategy

Gold is often misunderstood because people mix together two very different ideas: a hedge against inflation and a hedge against government and systemic risk. These are related but distinct concepts, and understanding the difference matters for making sound investment decisions.

Almost all tangible assets rise during inflation. Real estate, businesses, commodities, productive farmland: these all act as inflation hedges to varying degrees. What makes gold different is that it is portable, liquid, and universally recognized. This is why gold becomes critical during wars, political breakdowns, and capital controls. When capital needs to move quickly and safely across borders, gold has historically played that role in ways that real estate or business ownership cannot.

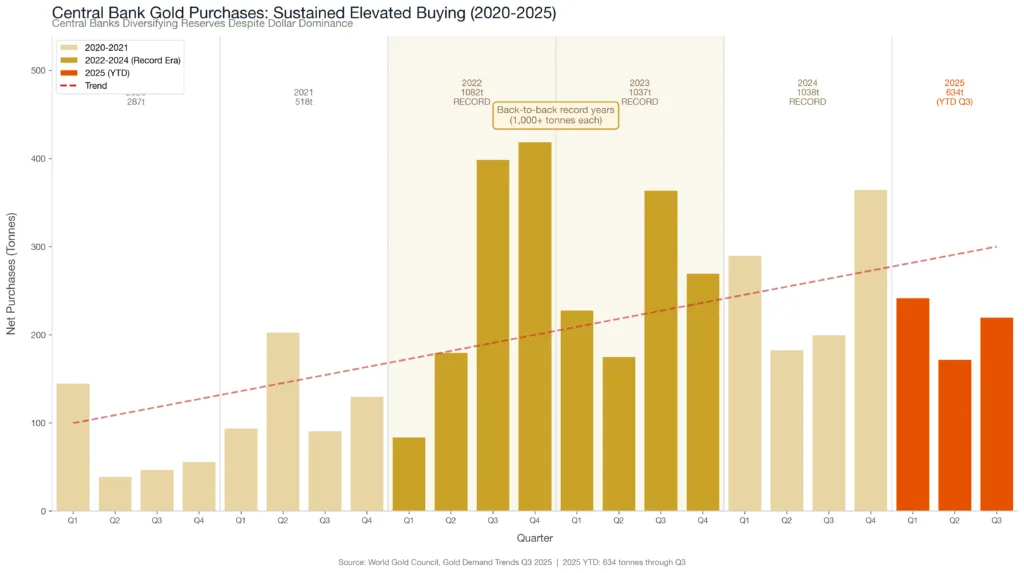

According to the World Gold Council’s Q3 2025 Gold Demand Trends report, total gold demand grew 3% year-over-year to 1,313 tonnes in Q3 2025, the highest quarterly total in their data series. The value measure of demand jumped 44% year-over-year to a record of US$146 billion. Central bank buying remained elevated at 220 tonnes for the quarter, with year-to-date purchases of 634 tonnes.

Central banks are not buying gold because they expect the dollar to collapse tomorrow. They are buying gold as part of prudent reserve diversification and as insurance against scenarios that may never occur but would be catastrophic if they did. This is the distinction between risk management and prediction.

The Honest Case for Owning Gold

Gold does not need exaggerated claims to justify its place in a portfolio. The honest case is compelling enough.

Gold provides genuine diversification because it often moves independently of stocks and bonds. During the 2008 financial crisis, gold held its value while equity markets crashed. During 2020’s pandemic uncertainty, gold reached new highs. In 2025, with gold prices touching records above $4,400 per ounce according to World Gold Council data, the metal continues demonstrating its role as a store of value during uncertain times.

Gold provides insurance against scenarios that are unlikely but possible. Political instability, currency crises, banking system failures, or geopolitical conflicts that disrupt normal financial channels: these events are rare, but they do occur. Gold provides optionality in these scenarios that other assets cannot match.

Gold maintains purchasing power over very long periods. An ounce of gold in Roman times could buy a quality toga and sandals. An ounce of gold today can buy a quality suit and shoes. This is not a perfect comparison, but it illustrates gold’s unique characteristic of maintaining real value across centuries and civilizations.

What gold does not do is generate cash flow, pay dividends, or grow through reinvestment. It sits there, maintaining value but not creating new wealth. This is why gold works best as a component of a diversified portfolio rather than as a primary investment strategy.

Risk Management, Not Prediction

Owning gold is about risk management, not predicting the end of the dollar tomorrow. It is about acknowledging uncertainty and preparing for multiple possible futures. The world’s financial center changes only when capital flows change, and that process is gradual and observable, not sudden and apocalyptic.

The IMF’s October 2025 World Economic Outlook projects continued global growth, though with significant uncertainties. The global financial system faces real challenges including elevated debt levels, geopolitical tensions, and structural economic shifts. These are legitimate concerns that warrant prudent portfolio positioning. They are not the same as imminent collapse.

A Distinction Worth Understanding

Gold is valuable. That does not automatically mean the dollar is collapsing. Understanding this difference matters dramatically for making sound investment decisions.

The case for gold stands on its own merits: diversification, insurance against tail risks, and proven ability to maintain purchasing power across generations. These are solid reasons that do not require exaggeration or fear to be compelling.

History shows that currency systems evolve gradually as economic power shifts. The dollar’s eventual decline, when it comes, will likely be a multi-decade process accompanied by observable changes in trade patterns, capital flows, and institutional arrangements. It will not happen because someone predicted it on the internet.

For investors building long-term positions in precious metals, this understanding enables better decision-making. Rather than panic buying at peaks based on collapse fears, investors can methodically build positions as part of a diversified strategy. Rather than expecting gold to solve all financial problems, investors can appreciate gold for what it actually does well.

Whether you are adding your first gold coins or expanding an existing precious metals allocation, Bullion Trading LLC offers comprehensive options backed by market expertise and commitment to honest investor education. Our extensive inventory of gold, silver, platinum, and palladium products provides solutions for every investment objective, from small retail purchases to larger institutional allocations.