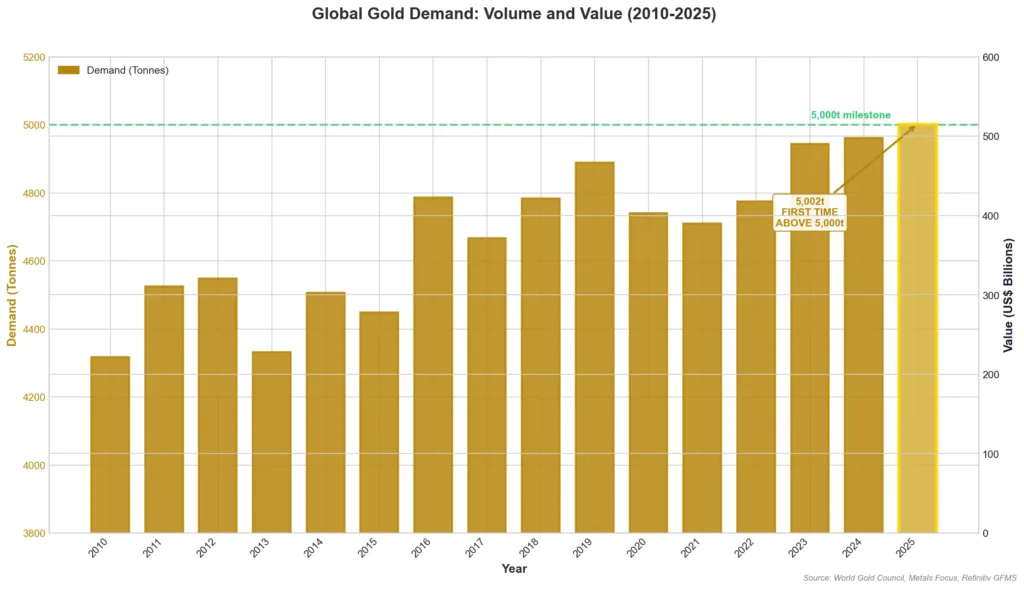

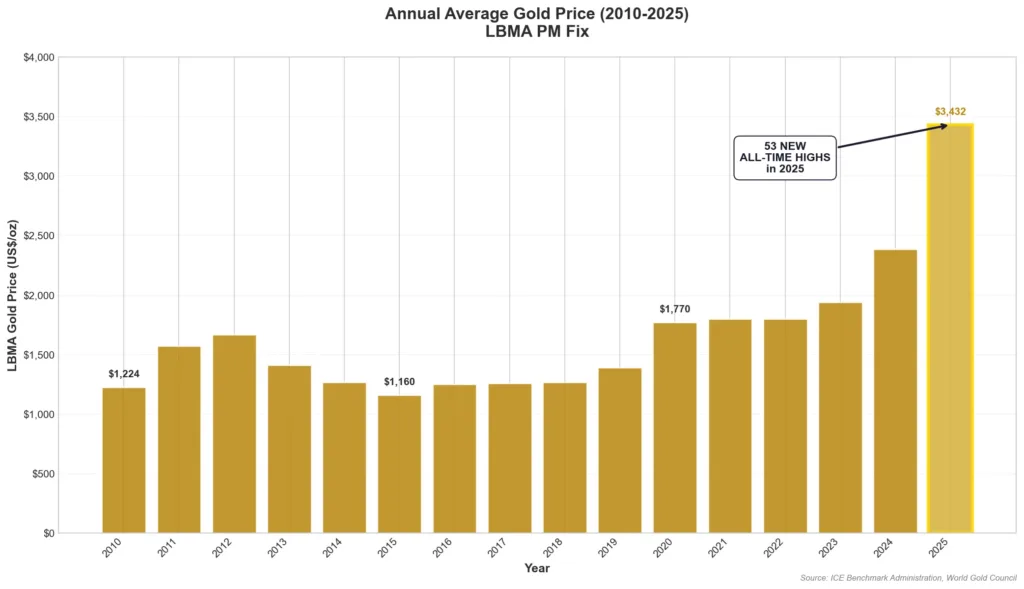

The numbers are in, and 2025 will go down as a groundbreaking year for gold. According to the World Gold Council’s Gold Demand Trends report released on January 29, 2026, total gold demand (including OTC transactions) exceeded 5,000 tonnes for the first time in history. When you combine that unprecedented volume with a gold price that set 53 new all-time highs throughout the year, you get a staggering total value of US$555 billion, representing a 45% year-over-year increase.

This wasn’t just another good year for gold. It was a record-breaking performance across multiple categories that reshaped how investors, central banks, and analysts view the precious metals market. Let’s dive into what happened, why it matters, and what it might mean for your investment strategy going forward.

Investment Demand Led the Charge

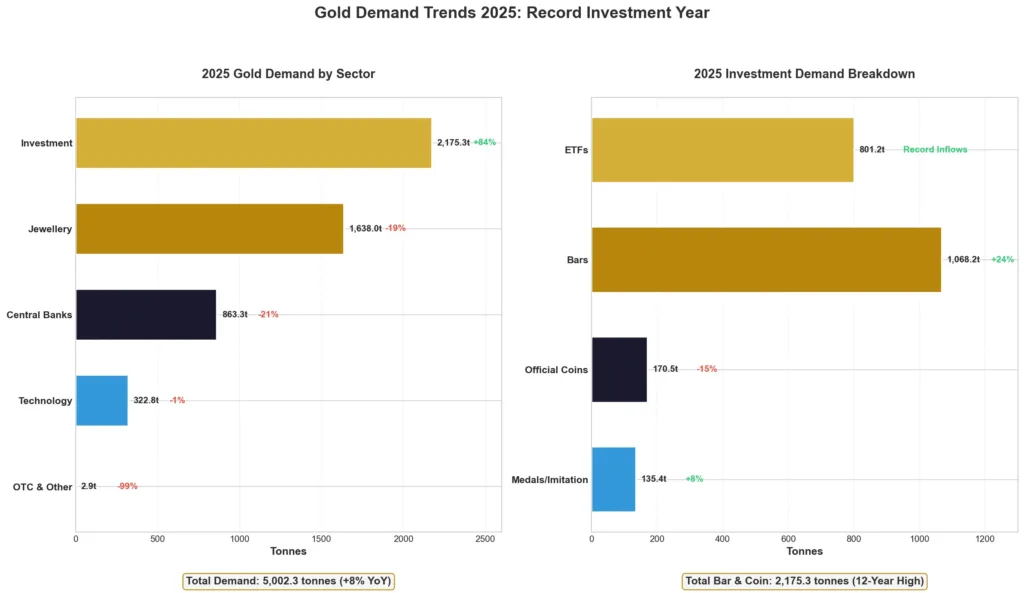

The headline story of 2025 was investment demand, and the numbers tell a compelling tale. Total investment demand reached 2,175.3 tonnes, representing an 84% increase compared to 2024. This wasn’t a marginal uptick or seasonal variation; it was a fundamental shift in how investors approached gold allocation.

Gold-backed exchange-traded funds (ETFs) drove much of this surge, adding 801 tonnes throughout the year. This marks the second-strongest year on record for ETF inflows, trailing only the pandemic-driven accumulation of 2020 when uncertainty pushed investors toward safe-haven assets. The difference this time is that 2025’s inflows came amid rising prices rather than falling ones, suggesting genuine conviction rather than panic buying.

Bar and coin demand accelerated to reach a 12-year high at 1,374.1 tonnes, up 16% from the previous year. Within this category, gold bars showed particular strength with demand increasing 24% to 1,068.2 tonnes. Interestingly, official coin demand declined 15% to 170.5 tonnes, while medals and imitation coins grew 8% to 135.4 tonnes. This split likely reflects both price sensitivity among retail buyers and production constraints at government mints struggling to keep pace with demand.

The U.S. Mint’s bullion sales figures provide a useful window into retail demand patterns, showing sustained interest throughout the year despite the rising price environment.

What Drove Investors to Gold in 2025?

Understanding the motivations behind 2025’s investment surge requires looking beyond the numbers to the macroeconomic backdrop. Safe-haven and diversification motives were consistent themes throughout the year, as geopolitical tensions, trade uncertainties, and concerns about fiscal sustainability drove investors toward assets with no counterparty risk.

Price-driven motivations also played a significant role. The gold price set 53 new all-time highs during 2025, with the average Q4 price reaching a record US$4,135 per ounce, a 55% increase compared to Q4 2024. For the full year, the average price of US$3,431 per ounce represented a 44% gain from 2024’s average of US$2,386. Rather than deterring buyers, these rising prices appeared to attract additional investment as momentum built throughout the year.

Japan offers a particularly interesting case study. According to The Jerusalem Post, gold fever hit Japan with panic buying as prices soared past $4,000, demonstrating how price psychology can work in gold’s favor when investors fear missing further upside.

Central Banks: Still Buying, But at a Slower Pace

Central bank purchases totaled 863.3 tonnes in 2025, placing at the upper end of the World Gold Council’s expected range. While this represents a 21% decline from 2024’s 1,092.4 tonnes, it remains historically elevated and geographically widespread. The moderation from recent peaks shouldn’t obscure the bigger picture: central banks have now been net purchasers of gold for 15 consecutive years since becoming net buyers in 2010.

The World Gold Council’s 2025 Central Bank Survey revealed that 95% of respondents expected global official gold reserves to increase over the next 12 months, marking the highest level of optimism in the survey’s eight-year history. Even more telling, a record 43% of central banks indicated plans to increase their own gold holdings, up from 29% in 2024, with none anticipating a reduction.

Poland emerged as a notable buyer, with Barron’s reporting in January 2025 that the Polish central bank was eyeing further increases in gold reserves. Kazakhstan continued its accumulation strategy, with Bloomberg (via terminal) reporting that the Kazakh central bank would keep buying gold as trade tensions grew. The Czech National Bank also maintained its gold acquisition program throughout the year.

Perhaps most significant for long-term outlook, Reuters reported in October 2025 that the Bank of Korea was considering gold purchases for the first time in many years, signaling potential new institutional demand from a major economy.

Jewellery: Volume Down, Value Up

The jewellery sector tells a nuanced story that highlights the price sensitivity of consumer demand. Jewellery fabrication declined 19% to 1,638 tonnes, with consumption falling 18% to 1,542.3 tonnes. In a market where gold prices increased 44% on average, this volume decline was entirely expected.

However, sentiment toward gold jewellery remained remarkably positive when measured by value rather than volume. Global jewellery demand climbed 18% in value terms to reach a record US$172 billion. This suggests that while consumers bought fewer grams of gold, they continued to place high value on gold jewellery as both adornment and investment. The price increase more than compensated for the volume decline, resulting in stronger revenue for the jewellery industry overall.

This dynamic is important for understanding the gold market’s structural support. Even when physical demand declines in tonnage terms, high prices maintain strong dollar demand, providing continued support for mine economics and refining operations.

Technology Demand Holds Steady

Technology demand showed remarkable stability at 322.8 tonnes, down just 1% from 2024’s 326.2 tonnes. Within this category, electronics demand was essentially flat at 270.4 tonnes (down from 270.8 tonnes), while other industrial applications declined 5% to 44.2 tonnes and dentistry fell 7% to 8.2 tonnes.

The stability in electronics demand is particularly noteworthy given disruptions in the consumer electronics space during 2025. Continued growth in AI-related applications helped offset weakness in traditional consumer electronics, demonstrating gold’s evolving role in cutting-edge technology. As artificial intelligence infrastructure expands, gold’s unique properties as a conductor and corrosion-resistant contact material become increasingly valuable in high-reliability applications.

Supply Side: Modest Growth Despite Record Prices

Total gold supply increased just 1% to 5,002.3 tonnes in 2025. Initial estimates suggest mine production reached a new record of 3,671.6 tonnes, though only marginally higher than 2024’s 3,650.4 tonnes. The relatively muted supply response to record prices reflects the multi-year lag between price signals and new production, as well as the increasingly difficult geology and regulatory environment facing new mine development.

Recycled gold showed surprisingly restrained growth, increasing only 3% to 1,404.3 tonnes despite a 67% increase in the US dollar gold price during the year. Historically, price spikes trigger significant scrap flows as consumers sell old jewellery and other gold items. The relatively modest recycling response in 2025 suggests either that easily available scrap has already been processed in previous years, or that holders are choosing to retain their gold despite the attractive selling prices.

Net producer hedging showed producers de-hedging 73.6 tonnes, indicating that mining companies expect prices to remain elevated and are choosing not to lock in current prices through forward sales.

Q4 2025: A Record Quarter

The fourth quarter of 2025 deserves special attention, as it set records of its own. Total quarterly demand of 1,303 tonnes was the highest ever for a fourth quarter, lifted by hefty ETF inflows of 175 tonnes and bar and coin buying of 420.5 tonnes.

The Q4 price averaged US$4,135 per ounce, 55% higher than Q4 2024. This strong finish to the year helped cement 2025’s status as a watershed moment for the gold market.

What This Means for Investors

The 2025 demand data carries several implications for precious metals investors. First, the breadth of demand across ETFs, bars, coins, and central banks suggests structural rather than speculative support. When multiple buyer categories increase allocations simultaneously, price support tends to be more durable than when demand is concentrated in a single segment.

Second, the relatively muted supply response indicates that significantly higher prices may be needed to incentivize meaningful production growth. Mine development takes years from discovery to production, and the 1% supply increase despite record prices suggests supply constraints may persist.

Third, central bank demand, while moderated from recent peaks, remains historically elevated and broadly distributed. The survey data showing 43% of central banks planning further accumulation suggests this demand category will continue supporting prices.

The World Gold Council’s Gold Outlook 2026 expects continued geopolitical tensions to drive another year of strong gold ETF inflows and robust bar and coin demand, underpinned by elevated central bank buying. The outlook notes that jewellery demand is likely to remain weak in a persistent high price environment, but investment and institutional demand should more than compensate.

Looking Ahead

Bloomberg’s median consensus commodity forecasts suggest analysts remain constructive on gold prices into Q4 2026, though with considerable uncertainty around economic and geopolitical trajectories. The World Gold Council’s own analysis suggests gold may perform well across various macroeconomic scenarios given its role as a diversifier and hedge.

For investors considering precious metals allocation, the 2025 demand trends underscore gold’s continued relevance in modern portfolios. Whether you’re building a new position or adding to existing holdings, understanding these demand dynamics helps inform timing and allocation decisions.

At Bullion Trading LLC, we’ve seen firsthand how investor interest has evolved throughout 2025. Our inventory of gold bars, coins, and bullion products offers options for investors at every level, from first-time buyers exploring fractional gold options to experienced investors accumulating larger positions. If you’re new to precious metals investing, our First-Time Precious Metals Buyer’s Checklist provides a comprehensive starting point.