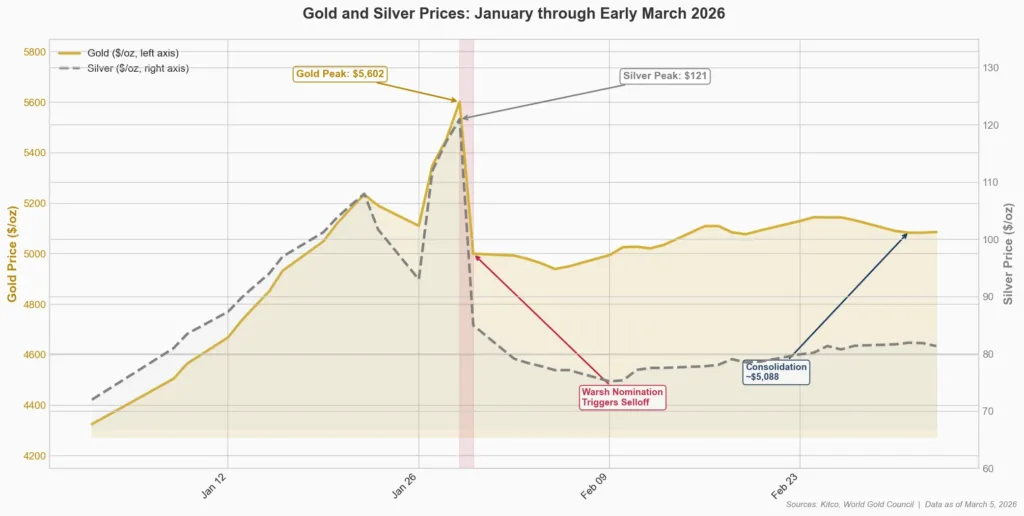

Earlier this year, gold and silver staged one of the most explosive rallies the precious metals market has ever seen. Silver surged roughly 68% in a single month, capping off gains of over 300% since the beginning of 2025. Gold climbed nearly 30% in January and more than doubled over the same period, briefly touching $5,602 per ounce. Moves like that simply do not happen often, and when they do, history has a clear message: the market needs time to breathe.

After the January peak, silver dropped more than 30% in just over a week. Gold gave back about 10% from its all-time high. For anyone watching the headlines, that kind of pullback sounds dramatic and even scary. But if you zoom out and look at how precious metals bull markets have behaved over the past 50 years, this gold silver correction 2026 is not unusual at all. In fact, it is exactly what healthy bull markets do.

What Actually Happened in January

To understand the correction, it helps to understand just how far and fast things moved. According to Kitco’s market analysis, gold reached an intraday record of $5,602 per ounce on January 29, representing a gain of 29.5% for the month alone. Silver’s move was even more extreme: it touched an all-time high above $121 per ounce, a gain of roughly 68.5% in January and more than 300% from its starting point near $24 at the beginning of 2025.

These were not gradual, steady climbs. They were parabolic moves fueled by a combination of central bank buying, geopolitical uncertainty, currency debasement concerns, and a flood of speculative capital pouring into the metals market. When assets move this far this fast, the inevitable question is not whether a correction will come, but when.

The immediate trigger arrived on January 30, when President Trump nominated Kevin Warsh as the next Federal Reserve Chair. Warsh, widely viewed as an inflation hawk, caused markets to quickly reprice interest rate expectations. Treasury yields pushed higher, the dollar strengthened, and precious metals sold off hard. Gold plunged $380 in just 28 minutes. Silver followed even harder, as it always does.

History Shows This Is Textbook Behavior

The pattern we saw in January is not new. It has repeated multiple times across decades of precious metals history, and every time, the initial reaction was fear followed by the realization that the long-term trend was still intact.

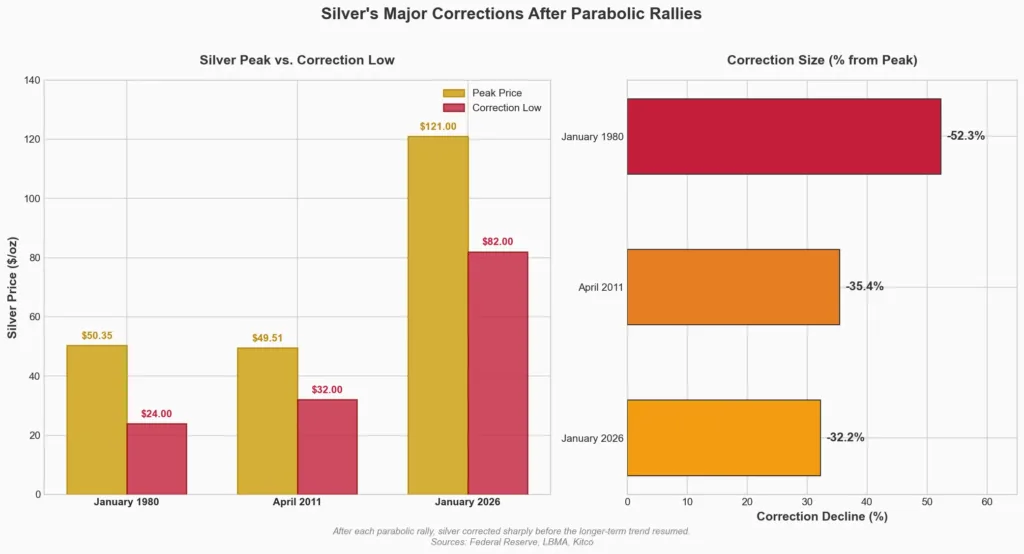

In January 1980, silver surged to $50 per ounce in a parabolic blow-off driven by the Hunt brothers’ attempted corner of the market and genuine inflation fears. The correction that followed was brutal. Silver lost more than 50% in a matter of days. According to Federal Reserve historical data, the refining system broke down under the pressure, with COMEX futures trading at a 25% discount to spot because metal could not be processed quickly enough.

In April 2011, silver once again raced toward $50 per ounce, reaching $49.51 before reversing. Over the following weeks, it gave back roughly 35% of its gains. The pullback lasted several weeks, shook out leveraged positions, and reset overbought technical conditions. Gold experienced a similar correction later that year after hitting its then-record of $1,921.

In both of these cases, the correction felt like the end of the world at the time. Commentators declared the bull market dead. Investors panicked. And yet, the forces that drove those rallies, rising government debt, currency debasement, inflation, geopolitical instability, did not disappear when prices pulled back. They never do.

Why Silver Always Falls Harder Than Gold

One thing that catches newer investors off guard is how much more volatile silver is compared to gold. Silver’s 30% decline from its January high was nearly three times the size of gold’s pullback in percentage terms. That is not a sign that something is broken with silver. It is simply how the metal behaves.

Silver’s market is much smaller than gold’s, which means less capital is needed to move the price significantly in either direction. According to the Silver Institute, the total annual silver market is valued at a fraction of the gold market, making it more susceptible to sharp swings when speculative capital enters or exits. During rallies, silver tends to outperform gold by wide margins. During corrections, it tends to fall harder and faster. That higher volatility is baked into the nature of the metal.

As HSBC’s James Steel noted in February, “Just because it’s a safe haven doesn’t mean it’s not volatile”. This applies to both gold and silver, but silver amplifies every move gold makes. If you own silver, the swings are part of the game. Understanding that going in makes it much easier to hold through the inevitable rough patches.

The Fundamentals Have Not Changed

Here is the part that matters most: nothing about the reasons people own gold and silver has changed since January’s peak. The correction was about speed and positioning, not about the underlying case for precious metals falling apart.

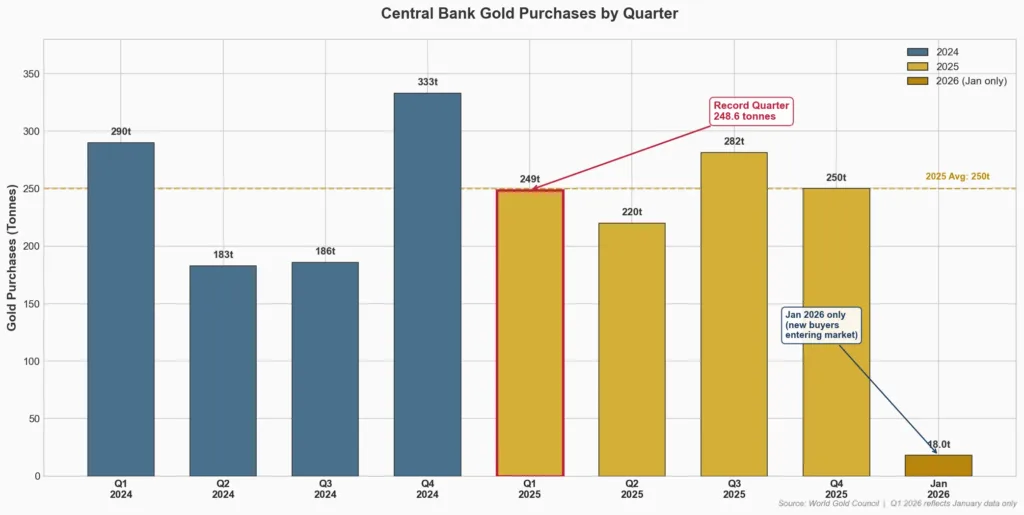

Central banks are still buying gold at a significant pace. The World Gold Council reported in early March that while January purchases came in below the 2025 monthly average, new sovereign buyers entered the market, suggesting the demand base is actually broadening. Central banks purchased 248.6 tonnes of gold in Q1 2025, the highest quarterly total ever recorded, and the structural shift toward gold reserves has shown no signs of reversing.

Joe Cavatoni of the World Gold Council described gold’s record 2025 run as “a structural shift, not a speculative peak”. That distinction matters. Speculative peaks tend to collapse and not recover. Structural shifts, where institutional demand permanently resets to a higher level, tend to produce corrections that are eventually absorbed by ongoing buying.

Currencies are still being printed at historically elevated rates. Government debt levels in the United States, Europe, and Japan continue to expand. J.P. Morgan analysts wrote in February that gold has surged over 170% in the past five years, and “the biggest driver may be a new era of geopolitical volatility and fragmentation incentivizing investors to buy the precious metal”. Their conclusion was that the case against gold continuing higher, while reasonable on its surface, is ultimately wrong.

Silver’s industrial demand picture remains equally compelling. Sprott’s Silver Investment Outlook showed that industrial demand accounts for 59% of silver usage, with solar photovoltaic demand alone representing 17% of total silver demand, up from just 5.6% in 2015. The silver market has been running structural supply deficits for seven consecutive years. None of that changed because prices pulled back in late January.

What Changed Was the Speed, Not the Direction

When markets move too far, too fast, a mechanical process takes over. Leveraged positions get unwound. Stop-loss orders trigger cascading sell-offs. Market makers widen their spreads and step back from providing liquidity. Algorithmic trading systems amplify the volatility. Ole Hansen, Head of Commodity Strategy at Saxo Bank, described this dynamic perfectly when he noted that gold had gone “from being the adult in the room to behaving like an angry teenager, just like silver”.

That is not a fundamental change. That is a market that got overheated and needed to reset. Investors paused, reassessed, and recalibrated their expectations for the near term. This is exactly how corrections work in every asset class, and precious metals are no exception.

StoneX analyst Rhona O’Connell noted in early March that gold and silver rallies are “likely on pause” even as new tariffs, higher inflation, and Middle East escalation continue to provide fundamental support. In other words, the bullish reasons have not gone away. The market is simply digesting a very large move.

Where Things Stand Now

As of early March 2026, gold is trading around $5,088 per ounce according to World Gold Council data, roughly 9% below its January peak but still more than double its price from the start of 2025. Silver is trading near $82 per ounce, down about 32% from its record but still up dramatically from where it started the prior year.

ANZ Bank forecasts gold reaching $5,800 per ounce in the second quarter of 2026. Multiple analysts from Franklin Templeton to Saxo Bank remain constructive on the medium-term outlook. The consensus view across major institutions is that the bull market is not over but rather that the market needed a reset before the next leg higher.

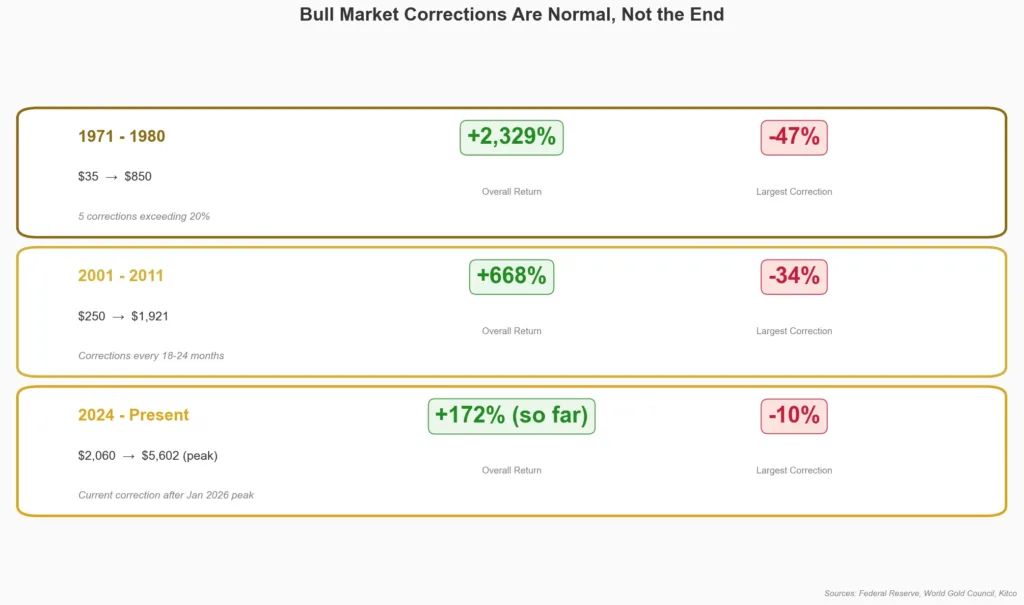

If history is any guide, the metals market may need more time and possibly a bit more downside before the next major move. Corrections can last weeks or months, and they do not always end cleanly. But this kind of consolidation is not weakness. It is how bull markets work. They climb, they pull back, they scare people out, and then they climb again. The 1970s bull market had five corrections exceeding 20%. The 2001 to 2011 bull market saw pullbacks of 15% to 34%. In both cases, the overall trend was decisively higher.

What This Means for Investors

The natural reaction to a sharp correction is to question everything. That is human nature. But the investors who have done best in precious metals over the decades are the ones who understood the difference between a change in price and a change in the story. Right now, the price has changed. The story has not.

Central banks are still accumulating. Governments are still running deficits. Industrial demand for silver is still growing. Geopolitical risks, including the ongoing conflict in the Middle East, show no signs of subsiding. These are the forces that drove gold from $2,600 to $5,600 and silver from $24 to $121. A correction does not erase those forces. It just temporarily overwhelms them with short-term selling pressure.

For those who have been wanting to add to their precious metals positions, corrections like this one are what experienced investors wait for. For those already holding, this is the part of the bull market that tests conviction. As veteran trader Kevin Grady told Kitco after the January crash, despite witnessing some of the wildest volatility in his 30-year career: “I do think that ultimately gold is going higher. I think silver’s going higher”.