Social media has been going crazy lately about silver. You have probably seen the posts: rumors about leverage, repo operations, and claims that major banks are about to collapse because of their silver short positions. Some of these posts get millions of views, and the headlines are designed to grab your attention. But what is actually happening in the silver market right now? Let me cut through the noise and give you my take on the paper silver vs physical silver price disconnect that everyone is talking about.

There is a real story here, and it matters for anyone holding physical silver or thinking about buying. But the real story is not about banks going bankrupt or some imminent financial collapse. The real story is that silver is behaving differently than it has for the past 30 to 40 years, and that shift has major implications for investors.

The Paper and Physical Price Gap Is Real

First, let me address what is actually true. There is a genuine disconnect right now between paper silver prices and what you pay for physical metal. This part is not a rumor or social media hype.

COMEX, operated by CME Group, serves as the main exchange for silver derivatives, options, and futures contracts. While physical silver can technically be delivered through COMEX, the reality is that most trades settle in cash. Traders are not actually taking delivery of metal bars. They are making bets on price movements, rolling contracts forward, and closing positions for cash profits or losses.

This creates a situation where paper silver trades one way while physical silver trades very differently around the world. When you go to buy actual silver coins or bars from a dealer, you are paying a premium over that paper spot price. And those premiums have widened significantly.

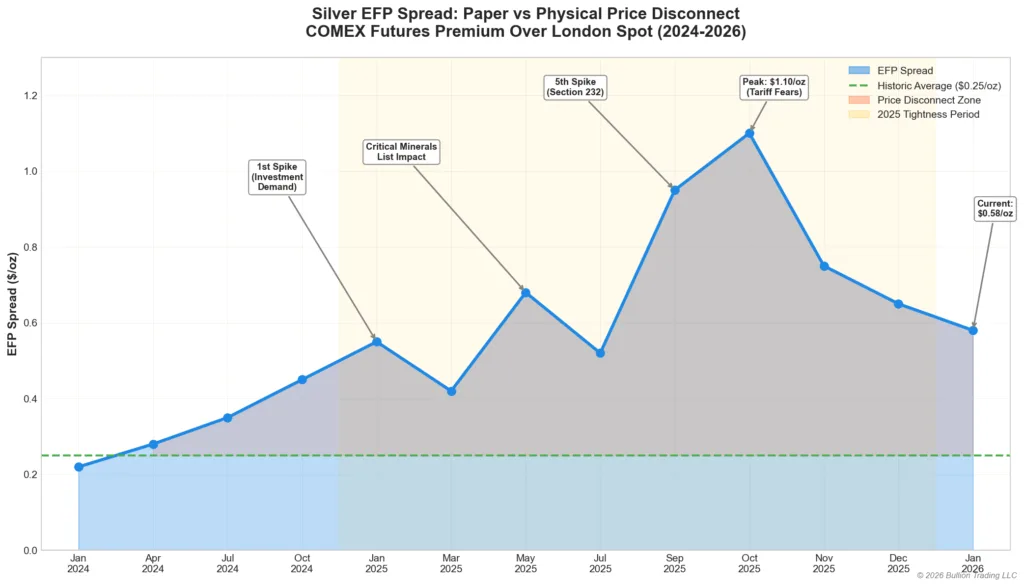

According to LBMA market analysis, the Exchange for Physical (EFP) spread, which measures the difference between COMEX futures prices and London spot prices, expanded from a historic average of 25 cents to as much as $1.10 per ounce during recent tightness episodes. This premium tells us that metal is flowing between markets at unprecedented rates because demand in certain locations outpaces available supply.

Why Margin Hikes Do Not Mean Silver Is Collapsing

Here is something that many people are not understanding correctly. When margin requirements get raised by 20%, 30%, or whatever the number happens to be, that does not mean silver is collapsing. It means the opposite in terms of market mechanics.

When margin requirements increase, paper traders must post more collateral to maintain their positions. Many cannot afford to do this, so they have to liquidate. This forces the paper demand out of the market. Traders are selling their contracts not because they think silver is going down, but because the leverage has become too expensive to maintain.

This selling pressure hits paper prices while physical supply remains tight. The traders dumping their COMEX contracts are not selling actual metal because they never owned any metal in the first place. Meanwhile, industrial users and physical buyers continue competing for real silver that is becoming harder to source in certain regions.

So when you see margin hikes followed by paper price drops, understand what you are actually watching. You are seeing leveraged speculators getting flushed out while the underlying physical market remains strong.

Physical Demand Has Not Gone Away

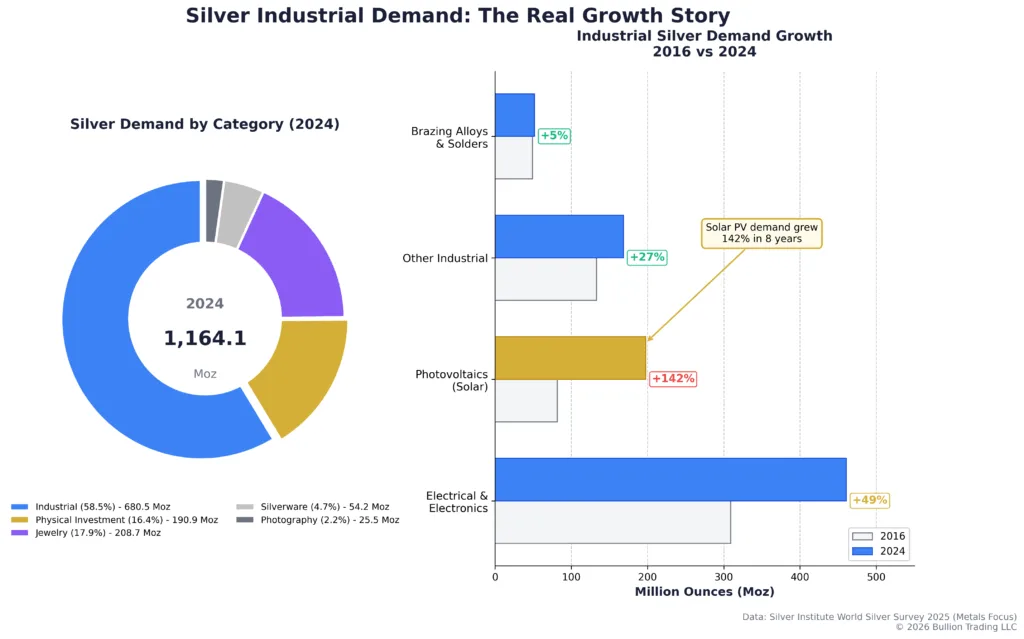

While paper traders are getting squeezed by margin increases, physical demand continues growing. According to The Silver Institute’s World Silver Survey 2025, industrial demand accounts for a massive portion of silver usage, and it hit another record year in 2024.

The electrical and electronics sector has been the biggest demand driver for silver, with consumption increasing 51% since 2016 according to Sprott’s Silver Investment Outlook. This makes sense when you think about it. Silver is the most electrically conductive metal on Earth, making it essential for applications where efficiency matters.

Solar photovoltaic demand alone accounted for 17% of total silver demand in 2024, compared to just 5.6% in 2015. That represents an annualized growth rate of 12.6%. China increased its solar capacity by 45% in 2024 alone, requiring enormous quantities of silver for panel manufacturing.

Add to this the silver needed for electric vehicles, consumer electronics, 5G networks, and defense applications. You end up with a situation where industrial users need silver regardless of price. A solar panel manufacturer cannot simply pause production when metal becomes tight. They must secure supply at whatever cost, which puts upward pressure on physical prices even when paper markets are selling off.

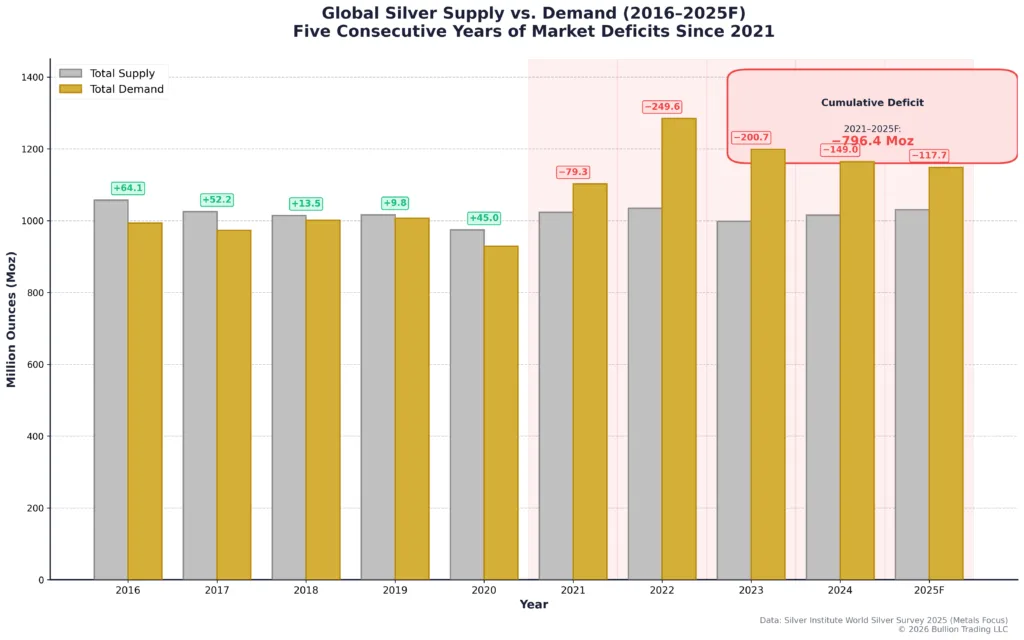

The Seven-Year Deficit That Nobody Talks About

Here is a number that deserves more attention than it gets. The global silver market has been in structural deficit for seven consecutive years. According to The Silver Institute, total silver demand in 2024 reached 1.16 billion ounces while global mine production was only 819.7 million ounces.

Sprott reports that the cumulative shortfall from 2021 through 2025 totals almost 800 million ounces. That is 800 million ounces of silver that had to come from existing above-ground inventories because mines could not produce enough to meet demand.

This matters because unlike paper contracts that can be created with a few keystrokes, physical silver must be mined, refined, and transported. Mine supply has actually declined by 7% since 2016 according to Sprott’s analysis. New silver production is not keeping pace with demand growth, and that gap has been filled by drawing down available inventories.

Investment demand through silver ETFs compounds this pressure. In the first half of 2025, global silver-backed exchange traded products experienced net inflows of 95 million ounces. This metal gets locked in vaults backing ETF shares and becomes unavailable for industrial users or physical buyers.

The Silver Institute reports that since 2019, more than 1.1 billion ounces have been drawn from available mobile inventory to satisfy both industrial demand and ETP backing requirements. That is metal that was readily accessible for trading and lending that is now locked up in various forms.

About Those Bank Collapse Rumors

Now let me address the elephant in the room. Social media keeps claiming that major banks like JPMorgan are about to collapse because of their silver short positions. Every repo operation or overnight funding number gets linked to some theory about banks being underwater on their metals positions.

Here is a reality check. If major banks were actually in trouble because of silver exposure, their stock prices would be telling you a very different story. Markets do not whisper about these things. They scream.

JPMorgan’s stock closed at $334.61 on January 6, 2026, just shy of its 52-week high of $337.25. The company reported trailing twelve-month net income of $56.66 billion according to Yahoo Finance data. Total assets exceed $4 trillion with a market cap of $920 billion. Does that look like a bank on the verge of collapse from silver shorts?

The bank has also just been named as topping global M&A rankings with $1.48 trillion in deals for 2025. Wall Street analysts maintain price targets averaging $332.87 with many issuing hold or outperform ratings. If silver shorts were creating existential risk, the institutional investors and analysts covering these banks would be sounding alarms.

This does not mean that banks do not have precious metals positions or that those positions are always profitable. But linking every repo operation and margin adjustment to some imminent banking crisis based on silver is lazy analysis designed to generate engagement rather than inform investors.

Silver Is No Longer Just a Monetary Metal

The real story that matters for your investment decisions is this: silver is no longer behaving the way it did for the last 30 to 40 years because its role in the global economy has fundamentally changed.

For most of modern history, silver was primarily a monetary metal and store of value with some industrial applications. Today, it has become a strategic industrial input essential to technologies that governments around the world consider critical infrastructure. As of early January 2026, silver trades above $82 per ounce according to Kitco, with the gold/silver ratio sitting around 55, well below its historical average of 67 and dramatically improved from the 91 ratio seen in mid-2025.

Solar energy, electric vehicles, defense systems, artificial intelligence, 5G networks. These are not optional industries that can simply reduce silver consumption when prices rise. They are sectors receiving massive government investment and policy support across virtually every major economy.

This creates a demand profile we have never seen before in the silver market. Industrial consumption has become price inelastic in the short term. Manufacturers building solar panels or EVs will pay whatever price is necessary to secure their silver supply because the alternative is shutting down production lines.

When Paper and Physical Disconnect for This Long

Anyone claiming they know exactly how this paper versus physical disconnect will resolve is guessing. Nobody has seen this exact setup before because the industrial demand dynamics are unprecedented.

But history does provide some guidance. When paper and physical prices stay disconnected for extended periods, the resolution typically comes from paper moving toward physical rather than physical collapsing down to paper prices.

During the 2025 silver market tightness, lease rates spiked to extraordinary levels. BullionVault reported that silver’s one-month lease rate reached more than 19% per annum and subsequently spiked to 35% as silver prices touched all-time highs above $50 per ounce. With silver now trading above $80, those dynamics have only intensified.

These elevated lease rates indicate that metal exists but faces temporary obstacles to immediate delivery. According to LBMA research, this reflects wrong location, wrong form, or metal tied up in uses that prevent immediate lending rather than fundamental shortage.

The market has weathered similar tightness episodes before and rebalanced. But the current situation has an additional factor that previous episodes lacked: structurally growing industrial demand that will not moderate simply because prices rise.

What This Means for Physical Silver Buyers

For investors building long-term precious metals positions, the current environment suggests focusing on fundamentals rather than social media drama.

The paper market volatility creates noise that can be either opportunity or trap depending on your approach. If you are buying physical silver for long-term holdings, paper price pullbacks driven by margin-induced liquidation can offer attractive entry points because the underlying physical market remains tight.

Physical premiums over spot prices reflect real supply chain constraints rather than artificial manipulation. Refiners prioritize large institutional bars that move efficiently through the system. Retail products like one-ounce coins require different production processes and more labor per ounce of output. When refiners are overwhelmed with demand, production of small retail forms falls behind, and that scarcity commands premiums.

According to industry reports cited in Numismatic News, silver refiners have been building up significant backlogs as demand for both large bars and retail products exceeds processing capacity.

Conclusion: Watch the Fundamentals, Not the Headlines

The silver market is telling a story in 2026, but it is not the story you see in most viral social media posts. Banks are not collapsing from silver shorts. The market is not being manipulated into oblivion. Silver is not about to go to zero or simultaneously skyrocket to $500 tomorrow.

The real story is more nuanced and, frankly, more bullish for long-term physical holders. Silver has become a strategic industrial metal with demand growing faster than production. With silver now above $80 per ounce and the gold/silver ratio compressing to around 55, the market is already reflecting some of this fundamental strength. The paper market and physical market have partially decoupled, with paper prices reflecting speculator positioning while physical prices reflect actual supply constraints.

Seven consecutive years of structural deficits have drawn down available inventories. Industrial demand continues growing regardless of price. Investment demand adds further pressure on available supply. And all of this is happening in an environment where new mine production is declining rather than expanding.

Whether you are looking to add physical silver to your portfolio or better understand why your existing holdings are behaving differently than the spot price might suggest, focus on these fundamentals. The headlines about leverage drama and bank collapses are designed to generate clicks. The supply and demand data tells you what actually matters for long-term value.

Whatever path you choose, Bullion Trading LLC stands ready to help with expert guidance and comprehensive precious metals solutions. Our inventory of silver coins, bars, and rounds provides options across the spectrum for investors navigating this unique market environment.