While investors chase gold and silver to record highs in 2025, two rarer metals quietly power every car on the road and could soon fuel the next energy revolution. Platinum trades at approximately $1,640 per troy ounce as of October 20, 2025, while palladium sits near $1,483. Yet platinum is 15 times rarer than gold, and palladium is 30 times rarer, yet both trade at substantial discounts to gold’s current price of $4,349 per ounce.

This disconnect creates one of the most compelling asymmetric opportunities in precious metals today. These metals aren’t just rare – they’re essential to global decarbonization, critical for every catalytic converter, and increasingly vital for the hydrogen economy that governments worldwide are backing with billions in investment.

What Makes Platinum & Palladium Special

Extreme Rarity Meets Industrial Necessity

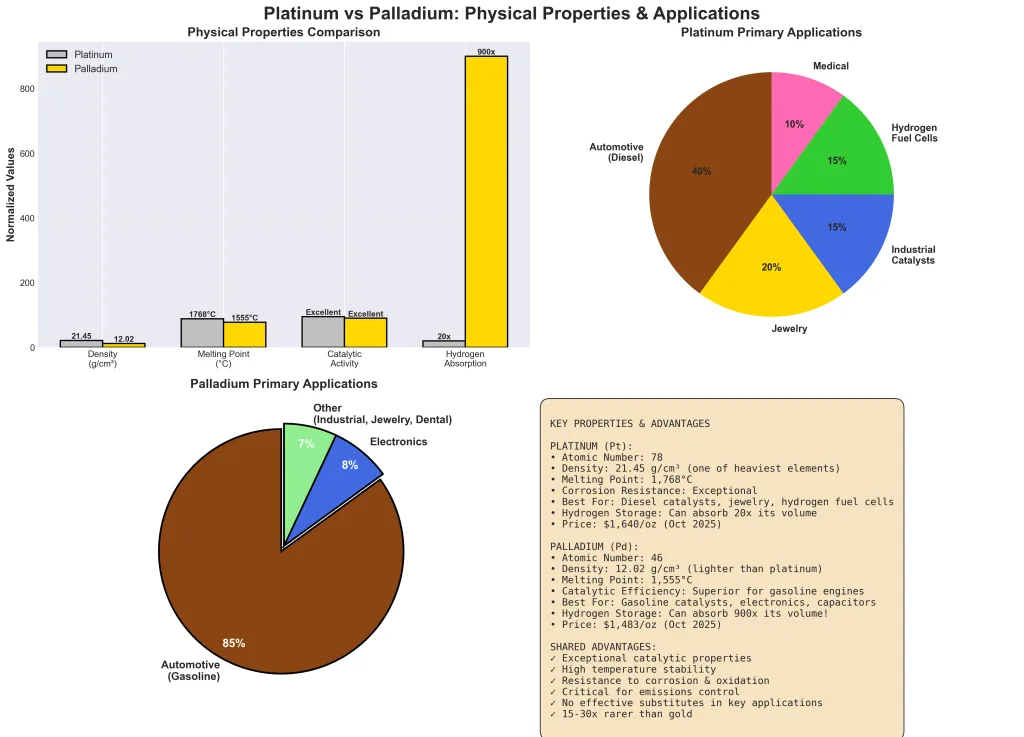

Platinum and palladium belong to the Platinum Group Metals (PGMs), six rare noble metals with unique catalytic properties. Platinum’s density of 21.45 grams per cubic centimeter and exceptional corrosion resistance make it irreplaceable in high-temperature applications. Palladium, at 12.02 grams per cubic centimeter, possesses remarkable catalytic abilities and can absorb 900 times its volume in hydrogen.

World Platinum Investment Council data shows annual platinum production at 6 million troy ounces and palladium at 7 million ounces. Compare this to gold production exceeding 110 million ounces annually. Despite this extreme scarcity, platinum trades at a 62% discount to gold and palladium at 66% discount.

Supply Concentration Creates Vulnerability

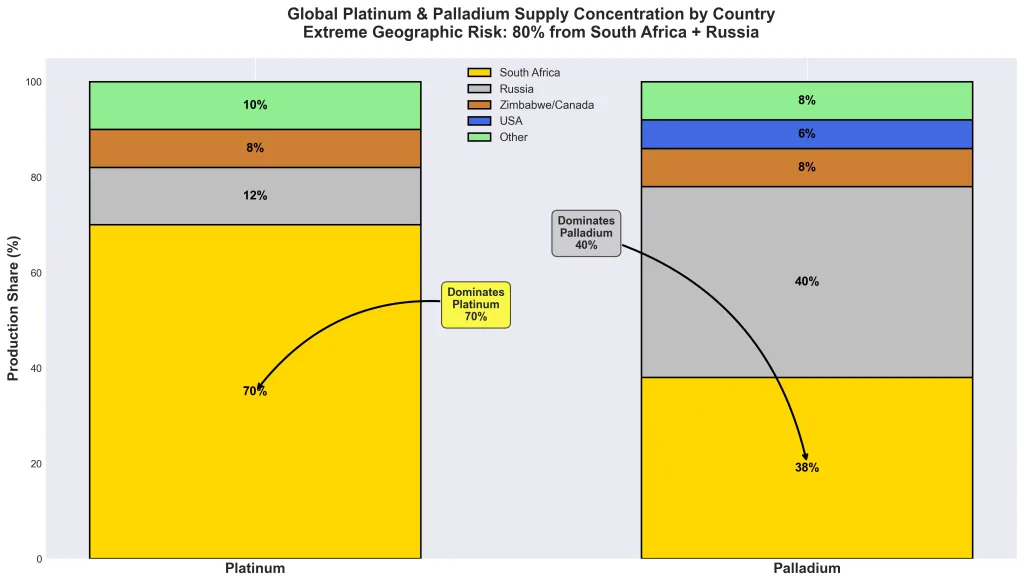

South Africa produces 70% of the world’s platinum and 38% of its palladium. Russia supplies another 40% of global palladium. This means roughly 80% of combined production comes from just two countries, both facing significant operational and geopolitical challenges including power shortages, labor disputes, and sanctions.

Industrial Demand: The Real Driver

Automotive Sector Dominance

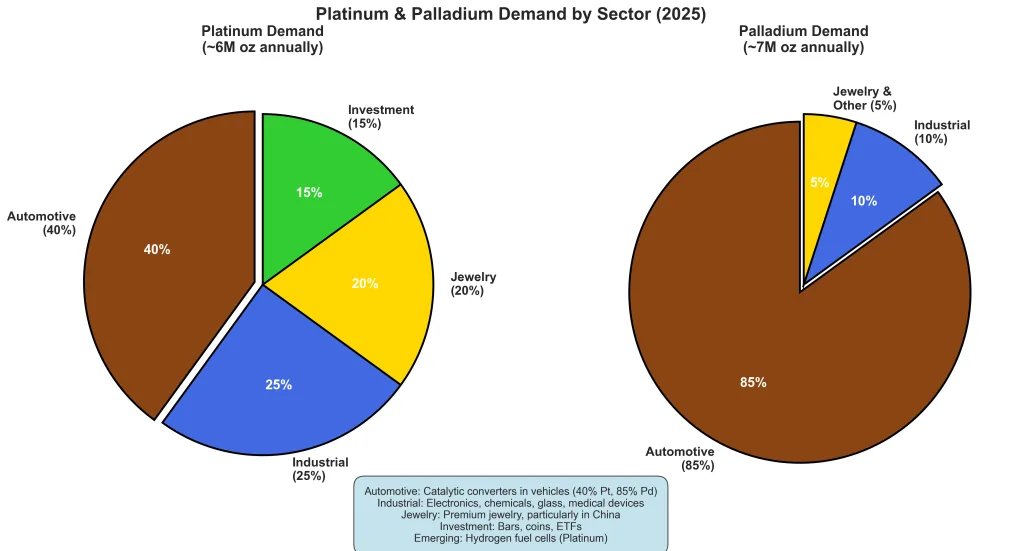

The automotive sector consumes 40% of platinum and 85% of palladium production annually, according to Johnson Matthey’s PGM Market Research. Every gasoline and diesel vehicle contains a catalytic converter with 2-7 grams of PGMs, worth $100-$400 per converter.

With 1.4 billion vehicles on global roads and 80 million produced annually, automotive demand remains structurally robust. Stricter emissions regulations like Euro 7 standards will require 20-30% more catalyst material per vehicle. Critically, hybrid vehicles often use more PGMs than conventional vehicles due to frequent engine cycling.

Hydrogen: The Game-Changing Catalyst

Platinum serves as the critical catalyst in hydrogen fuel cells, converting hydrogen and oxygen into electricity with zero emissions. The European Union has committed over €470 billion to hydrogen development through 2030 as part of its European Green Deal.

According to the World Platinum Investment Council, hydrogen-related platinum demand could reach 1.5-2 million troy ounces annually by 2030, representing 25-33% of current total supply. This creates entirely new consumption that didn’t exist before, fundamentally transforming market balance.

Market Deficit Dynamics

Supply Cannot Keep Pace

Platinum has transitioned into sustained deficit. The World Platinum Investment Council’s Q2 2025 forecast projects an 850,000 ounce deficit for 2025, the third consecutive annual deficit. Cumulative deficits since 2023 total approximately 2 million ounces, equal to one-third of annual mine supply.

South African mines extend 2-3 kilometers underground with rock temperatures exceeding 60°C, requiring extensive cooling systems. Production costs have risen steadily while chronic power cuts from state utility Eskom force periodic shutdowns. No major new PGM deposits have been discovered in decades, and development timelines stretch 10-15 years from discovery to production.

Industrial demand proves remarkably price-inelastic. Automakers cannot reduce platinum or palladium content below levels required for emissions compliance, regardless of price.

The Investment Case

Platinum: Deep Value Play

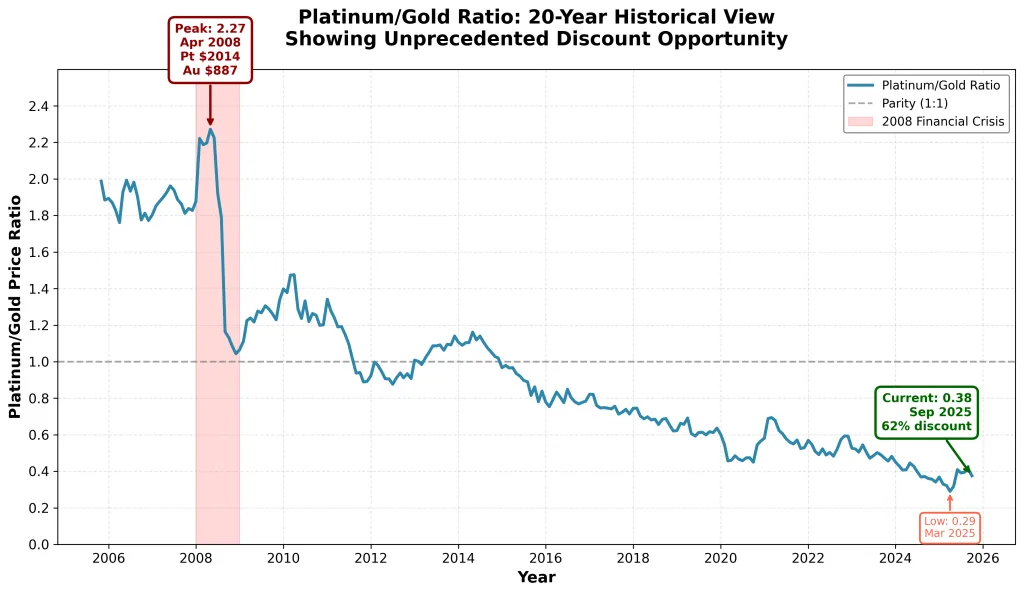

At $1,640 versus gold’s $4,349, platinum’s 62% discount represents a complete inversion of historical norms. From 1970-2014, platinum consistently commanded a 20-40% premium to gold. During the 2008 financial crisis, platinum traded above $2,000 while gold sat below $1,000, giving platinum a 2.27x premium.

Multiple catalysts support revaluation:

Chinese Demand Surge: Q2 2025 data shows jewelry demand surging 11% to 2,226 thousand ounces, the highest since 2018, with Chinese consumers driving growth.

Deepening Deficits: The 850,000 ounce deficit projected for 2025 will exhaust above-ground stocks within 2-3 years unless prices rise significantly.

Hydrogen Infrastructure: Every new hydrogen fueling station and fuel cell vehicle announcement incrementally tightens supply-demand balance.

Even partial mean reversion toward historical parity with gold implies 165% upside from current levels.

Palladium: High-Beta Industrial Play

Palladium has declined over 50% from its 2021 peak above $3,000, reflecting concerns about electric vehicle adoption. However, these fears appear premature. The International Energy Agency’s Global EV Outlook 2024 suggests internal combustion vehicles will remain dominant through 2030 at minimum.

Recent U.S. trade restrictions on Russian palladium could tighten supply for American manufacturers. Palladium continues trading in structural deficit with no realistic substitute for gasoline catalytic converters.

Portfolio Strategy

Allocation Framework

A targeted 5–15% exposure to platinum-group metals adds asymmetric potential to a precious metals portfolio. Weighting roughly two-thirds toward platinum captures its revaluation potential, while a smaller palladium position provides optionality on industrial recovery.

Implementation: Physical metal through reputable dealers like Bullion Trading LLC offers pure exposure and eliminates counterparty risk.

Maintain a 2-3 year minimum holding period, using price weakness to dollar-cost average rather than attempting to time entries. PGMs’ supply-demand fundamentals play out over years, not weeks.

Key Risks

Volatility and Economic Sensitivity

Daily price swings of 2-3% are common due to limited market liquidity. Unlike gold, which provides crisis protection, PGMs can decline alongside stocks during recessions due to their industrial exposure. This different role requires proper position sizing within portfolios.

The EV Transition Timeline

Electric vehicle adoption represents the largest long-term risk. However, real-world adoption has consistently lagged forecasts. Infrastructure challenges, range anxiety, and higher costs have slowed consumer acceptance. For platinum specifically, hydrogen fuel cell applications could offset automotive demand decline.

The global vehicle fleet turns over slowly, with average age exceeding 12 years in the U.S. Even aggressive EV adoption scenarios suggest hundreds of millions of ICE vehicles will remain on roads through 2040-2050.

Conclusion: The Contrarian Opportunity

The investment case for platinum and palladium rests on a fundamental disconnect between geological scarcity, industrial essentiality, and current valuations. These metals are 15-30 times rarer than gold yet trade at 60-70% discounts, an anomaly unprecedented in modern commodity markets.

Their industrial importance cannot be overstated. Every one of the world’s 1.4 billion vehicles depends on PGMs to meet emissions standards. The hydrogen economy envisions fuel cells requiring substantial platinum loadings. Meanwhile, supply faces structural constraints with no major new deposits awaiting development.

Market deficits are drawing down inventories accumulated over decades, and current prices provide insufficient incentive for supply responses needed to balance markets. For investors willing to look beyond gold and silver headlines, platinum and palladium offer compelling asymmetric risk-reward profiles.

The path won’t be smooth. Volatility is inherent to smaller, industrially-focused metals, and economic downturns will pressure prices. But for patient investors with 2-3 year horizons and proper position sizing, the opportunity appears substantial.

As gold tests new highs above $4,350 and silver captures attention, the world’s rarest precious metals trade in quiet obscurity. But market inefficiencies don’t persist forever. Supply-demand fundamentals eventually assert themselves, and scarcity creates value markets cannot ignore indefinitely.Whether you’re looking to diversify beyond gold and silver or build strategic positions in undervalued industrial metals, Bullion Trading LLC offers comprehensive precious metals solutions backed by market expertise. Our inventory includes platinum and palladium products alongside our extensive gold and silver offerings, providing options for investors seeking exposure across the full precious metals spectrum.