Gold prices have surged to unprecedented levels in 2026, breaking through $4,900 per ounce as investors navigate an increasingly complex monetary policy environment. Understanding the relationship between central bank actions and gold prices has never been more critical for investors seeking to protect and grow their wealth. At the center of this relationship sits one of modern monetary policy’s most powerful and controversial tools: quantitative easing.

The connection between quantitative easing (QE) and gold prices isn’t merely theoretical. Since the Federal Reserve first deployed large-scale QE programs during the 2008 financial crisis, gold has demonstrated remarkable sensitivity to central bank balance sheet expansions. Today, as the Fed maintains a balance sheet of approximately $6.9 trillion following years of monetary expansion, understanding how QE influences gold prices provides essential context for navigating current market conditions.

For precious metals investors, the mechanics of quantitative easing represent far more than academic interest. These policies create the fundamental conditions that drive gold’s performance, influencing everything from inflation expectations to currency valuations to real interest rates. By understanding these dynamics, investors can make more informed decisions about when to accumulate positions, how to structure portfolios, and what to expect as monetary policy evolves.

What Is Quantitative Easing?

Quantitative easing represents an unconventional monetary policy tool that central banks deploy when traditional interest rate adjustments become ineffective. According to Investopedia’s comprehensive analysis, QE involves central banks purchasing securities in the open market to increase the money supply and encourage lending and investment.

The mechanics work as follows. When central banks like the Federal Reserve implement QE, they create new bank reserves electronically and use them to purchase government bonds, mortgage-backed securities, and other assets from financial institutions. These purchases inject liquidity directly into the banking system, lowering long-term interest rates and theoretically encouraging banks to lend more freely to businesses and consumers.

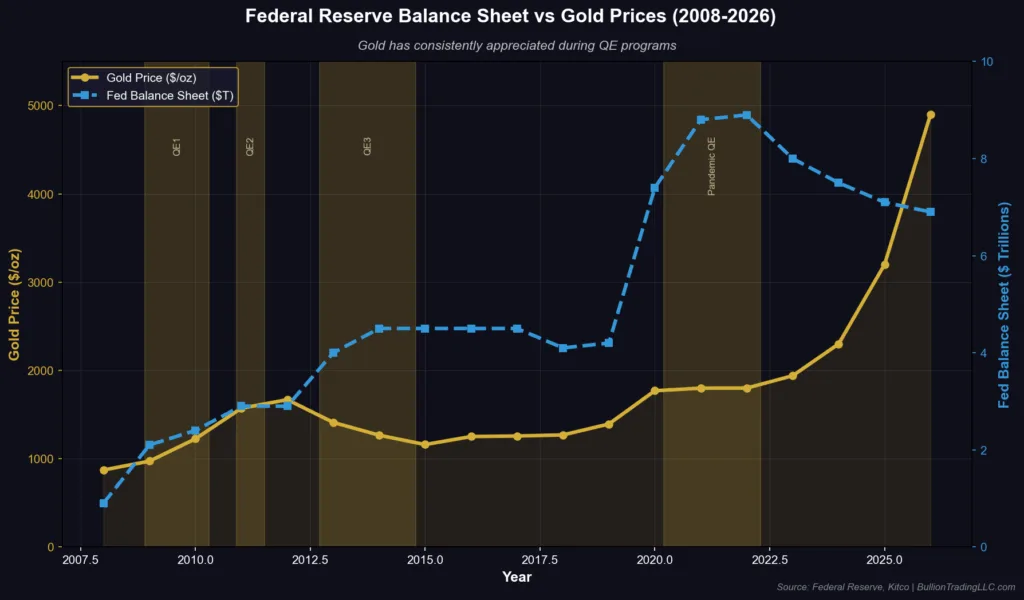

The Federal Reserve deployed QE on an unprecedented scale following the 2007-2008 financial crisis. Between 2009 and 2014, the Fed’s balance sheet grew from roughly $900 billion to over $4.5 trillion as it purchased bonds and mortgage securities. The Federal Reserve’s own data shows that during the COVID-19 pandemic in 2020, the Fed dramatically expanded QE again, with holdings reaching 56% of Treasury security issuances by the first quarter of 2021.

Unlike traditional monetary policy that works through the federal funds rate (the overnight lending rate between banks), QE operates when interest rates are already near zero and cannot be reduced further. In these circumstances, central banks turn to balance sheet expansion as their primary tool for providing economic stimulus.

The impacts of QE extend far beyond banking system liquidity. By purchasing massive quantities of government bonds, central banks drive bond prices higher and yields lower. These lower yields on government securities push investors toward riskier assets seeking better returns, creating what economists call a “portfolio rebalancing effect.” Additionally, the expansion of the money supply creates potential inflationary pressure, particularly when economic activity eventually accelerates.

How Quantitative Easing Affects Gold: The Fundamental Mechanisms

The relationship between quantitative easing and gold prices operates through several interconnected mechanisms, each creating upward pressure on precious metal valuations. Understanding these connections helps explain why gold has historically performed strongly during QE periods.

Currency devaluation stands as perhaps the most direct mechanism linking QE to gold prices. When central banks dramatically expand the money supply through asset purchases, they effectively dilute the value of their currency. Gold, priced in dollars but holding intrinsic value independent of any government’s monetary policy, becomes more valuable in currency terms. Investopedia notes that QE can devalue domestic currency, making imports more expensive and impacting consumer price levels. For gold investors, this currency devaluation represents a fundamental driver of price appreciation.

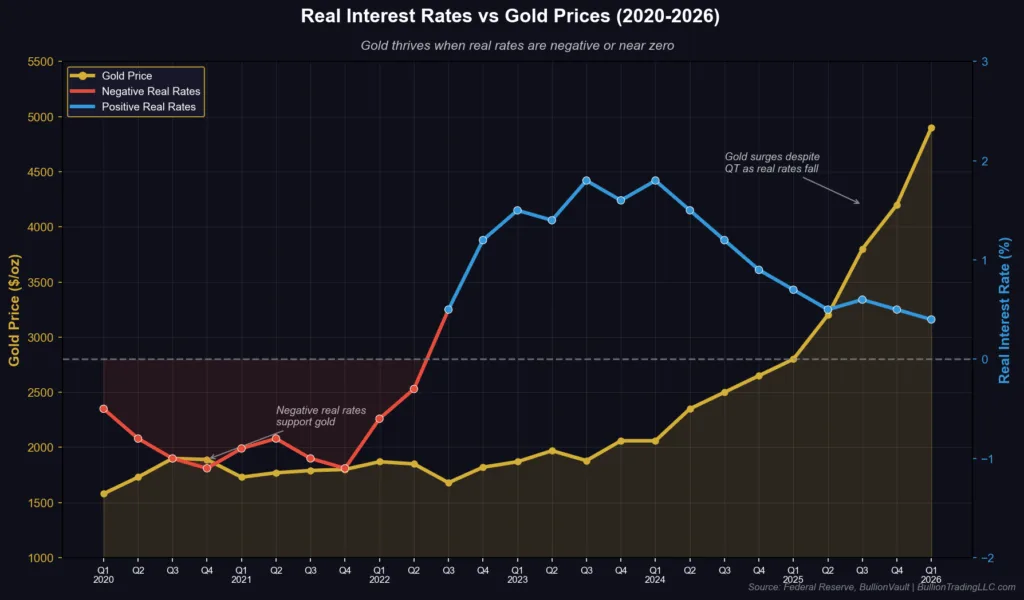

Real interest rates, the nominal interest rate minus inflation expectations, provide another critical transmission mechanism. QE drives nominal interest rates down by flooding markets with liquidity and purchasing interest-bearing securities. Simultaneously, the money supply expansion inherent in QE creates inflation expectations. When these forces combine to push real interest rates into negative territory, gold becomes increasingly attractive. Unlike bonds or savings accounts that deliver negative real returns when real rates are below zero, gold preserves purchasing power without the burden of negative real yields.

Inflation expectations themselves play a powerful role in driving gold demand during QE periods. The massive expansion of central bank balance sheets creates concerns about future inflation, even if current inflation remains muted. Gold’s historical performance as an inflation hedge makes it a natural destination for capital seeking protection against currency debasement. As Federal Reserve data shows, inflation measured by the Personal Consumption Expenditures (PCE) Price Index reached 7.2% in June 2022 following extensive QE programs, validating concerns about monetary expansion’s inflationary consequences.

Portfolio rebalancing creates another channel through which QE drives gold demand. When QE pushes government bond yields to historic lows, investors holding these securities face diminishing returns. Many reallocate capital toward alternative assets offering better risk-adjusted returns or portfolio diversification benefits. Gold, with its low correlation to traditional financial assets, becomes an attractive destination for these reallocated funds.

The wealth effect represents a less obvious but still significant mechanism. QE programs aim to boost asset prices across the board, from stocks to real estate to commodities. As investors’ portfolio values rise, some of this increased wealth flows into gold as part of a diversified holdings strategy. This dynamic creates self-reinforcing momentum during QE periods.

Historical Evidence: Gold’s Performance During QE Programs

The historical record provides compelling evidence of gold’s sensitivity to quantitative easing programs. Examining specific QE periods reveals consistent patterns of gold price appreciation that validate the theoretical mechanisms described above.

During the Federal Reserve’s first QE program (QE1) from November 2008 to March 2010, gold prices rose from approximately $750 per ounce to over $1,100, representing a gain of roughly 47%. This period coincided with the Fed’s purchase of $1.7 trillion in mortgage-backed securities, agency debt, and Treasury securities. The magnitude of this monetary expansion created immediate concerns about currency devaluation and future inflation, driving investors toward gold as a safe haven and inflation hedge.

QE2, running from November 2010 to June 2011, saw the Fed purchase an additional $600 billion in Treasury securities. Gold responded with continued appreciation, rising from around $1,350 per ounce to over $1,900 by September 2011, shortly after the program concluded. This period marked gold’s nominal price peak before its subsequent correction, demonstrating both the powerful impact of QE on gold prices and the importance of other factors that can eventually overwhelm monetary policy influences.

The Federal Reserve’s QE3 program, announced in September 2012 and continuing through October 2014, proved more complex in its impact on gold. Unlike previous QE programs with predetermined size limits, QE3 was open-ended, with the Fed committing to purchase $40 billion monthly in mortgage-backed securities (later expanded to $85 billion including Treasuries). Interestingly, gold prices declined during much of this period, falling from over $1,700 per ounce in late 2012 to below $1,200 by late 2014.

This apparent contradiction requires explanation. Gold’s decline during QE3 resulted from several factors overwhelming the expansionary monetary policy. The U.S. economy’s strengthening recovery reduced safe-haven demand. The Fed’s clear communication about eventual policy normalization anchored inflation expectations despite ongoing QE. Most significantly, rising real interest rates in 2013 and 2014, as economic growth accelerated while QE continued, made opportunity costs of holding non-yielding gold more pronounced.

The COVID-19 pandemic prompted the most aggressive QE program in Federal Reserve history. Beginning in March 2020, the Fed purchased assets at an unprecedented pace, expanding its balance sheet by over $4 trillion in less than two years. Gold’s response was dramatic and immediate. Prices surged from around $1,600 per ounce in March 2020 to over $2,070 by August 2020, setting new nominal highs. The combination of near-zero interest rates, massive fiscal and monetary stimulus, and profound economic uncertainty created ideal conditions for gold appreciation.

The European Central Bank and Bank of Japan provided additional international evidence for QE’s impact on gold. When these institutions implemented their own QE programs, gold prices in euros and yen showed even more dramatic appreciation than dollar-denominated gold, reflecting currency-specific devaluation effects alongside global monetary expansion trends.

The Current Environment: Quantitative Tightening and Gold’s Resilience

The monetary policy environment has shifted dramatically since the peak of pandemic-era QE. In 2022, facing inflation that reached 40-year highs, the Federal Reserve pivoted from quantitative easing to quantitative tightening (QT), allowing bonds to mature without replacement and actively reducing its balance sheet. This shift might be expected to create headwinds for gold prices, yet the precious metal has demonstrated remarkable resilience, with prices reaching new nominal highs above $4,900 per ounce in January 2026.

Federal Reserve data shows the central bank has reduced its balance sheet from peak levels near $9 trillion to approximately $6.9 trillion as of January 2026. This reduction represents the largest quantitative tightening program in the Fed’s history. Traditional QE-gold relationships might suggest this should be bearish for precious metals, yet gold has thrived.

Several factors explain this apparent paradox. First, despite QT, the Fed’s balance sheet remains historically massive. Even after significant reduction, it stands nearly eight times larger than before the 2008 financial crisis. This elevated baseline means monetary conditions remain extraordinarily loose by historical standards, even as the marginal direction has shifted toward tightening.

Second, real interest rates have remained relatively contained despite the Fed’s aggressive rate hiking campaign in 2022 and 2023. With the federal funds rate currently in the 3.50% to 3.75% range and inflation measured by PCE running at 2.8% as of November 2025, real rates hover barely above zero. These modest real rates continue to support gold, particularly as concerns about fiscal sustainability and potential future inflation episodes persist.

Third, geopolitical uncertainty has intensified dramatically, with ongoing conflicts, trade tensions, and questions about the dollar’s reserve currency status driving safe-haven demand. Gold’s role as geopolitical insurance has become increasingly valued as the international order faces unprecedented challenges.

Fourth, central bank gold purchases have reached historic levels. Central banks purchased 248.6 tonnes in Q1 2025, the highest quarterly purchase ever recorded. This institutional demand, driven by reserve diversification away from dollar assets, creates powerful fundamental support for gold prices independent of Western monetary policy directions.

What Investors Need to Know: Practical Implications for Gold Holdings

Understanding the quantitative easing-gold relationship provides crucial insights for investment strategy, but translating theory into practice requires careful consideration of current conditions and forward-looking expectations.

The first critical lesson concerns timing and position building. Gold’s historical sensitivity to QE doesn’t mean prices only rise during active QE programs. The anticipation of future QE, the persistence of QE’s effects long after programs end, and the elevated baseline from past QE all influence gold prices. Investors shouldn’t wait for central banks to announce new QE programs before establishing positions. By that time, gold often has already repriced significantly to reflect changed monetary policy expectations.

The relationship between real interest rates and gold deserves particular attention. Even when QE isn’t actively expanding central bank balance sheets, the low interest rate environment that QE creates can persist for years. Monitoring real interest rates, both current and expected, provides one of the most reliable guides to gold’s medium-term direction. When real rates are negative or very low, gold typically performs well. When real rates rise significantly, gold faces headwinds.

Diversification benefits from gold extend beyond simple inflation hedging. The precious metal’s low or negative correlation with stocks and bonds makes it valuable for portfolio construction regardless of immediate monetary policy direction. Modern portfolio theory suggests allocations of 5% to 15% to gold can improve risk-adjusted returns across various market environments. Quantitative easing periods often provide attractive entry points for establishing or increasing these allocations.

Currency considerations matter significantly for international investors. While U.S. dollar-denominated gold prices receive the most attention, investors in other currencies experience different dynamics based on their local central bank policies. When the ECB or Bank of Japan implement QE while the Fed doesn’t (or vice versa), relative currency movements can create outsized returns for investors in certain jurisdictions.

The form of gold ownership carries practical implications. Physical gold, whether coins, bars, or stored bullion, provides direct exposure without counterparty risk. However, storage and insurance costs create negative carry that can erode returns during extended flat price periods. Gold ETFs offer liquid exposure with minimal carrying costs but introduce counterparty risk. Mining stocks provide leveraged exposure to gold prices but carry company-specific and operational risks.

Looking Forward: What to Expect as Monetary Policy Evolves

The monetary policy outlook remains fluid as central banks navigate conflicting mandates of controlling inflation, supporting growth, and maintaining financial stability. Understanding potential future scenarios helps investors position gold holdings appropriately.

Most economists expect the Federal Reserve to resume lowering interest rates during 2026, with markets pricing in multiple rate cuts. However, the path toward renewed QE remains uncertain. If the economy enters recession, the Fed would likely cut rates aggressively and could restart asset purchases if rates reach the zero lower bound again. Alternatively, if inflation proves more persistent than expected, the Fed might maintain elevated rates for longer, potentially delaying any return to QE for years.

The fiscal situation adds complexity. U.S. government debt exceeds $36 trillion, with deficits projected to remain elevated indefinitely. Some analysts argue this debt burden makes future QE inevitable, as the Fed may eventually need to purchase government bonds to keep financing costs manageable. This “fiscal dominance” scenario would likely prove extremely bullish for gold, as it would represent monetization of government debt.

International monetary policy divergence creates another consideration. While the Fed has tightened policy, the Bank of Japan only recently ended negative interest rates in 2024 after years of aggressive QE. According to recent CNBC reporting, the BOJ maintains its accommodative stance as Japan grapples with deflation legacy. The ECB faces similar challenges. These policy differences create opportunities for gold investors to benefit from relative monetary conditions across major economies.

Central bank digital currencies (CBDCs) represent a wildcard for future monetary policy transmission. If major central banks successfully implement CBDCs, they may gain new tools for monetary policy that could be either complementary or alternative to traditional QE. The implications for gold remain uncertain but warrant monitoring.

The growing role of gold in the monetary system itself deserves attention. As central banks accumulate gold reserves at record pace and discussions about gold-backed settlement systems gain traction, the precious metal may be gaining renewed monetary importance. This could amplify gold’s sensitivity to QE and other monetary policies if gold increasingly serves as an alternative international reserve asset to the dollar.

Quantitative Easing’s Legacy: What the Data Tells Us About Gold’s Future

The evidence accumulated across multiple QE programs and varying economic conditions reveals clear patterns that inform investment strategy. Gold demonstrates consistent sensitivity to the fundamental forces QE unleashes: currency devaluation, negative real interest rates, inflation concerns, and financial uncertainty.

However, the relationship isn’t mechanical or instantaneous. Gold prices reflect expectations about future policy as much as current programs. Market conditions, alternative investment opportunities, and real interest rates all modulate gold’s response to QE. Investors who understand these nuances can better navigate the inherent volatility in precious metals markets while maintaining conviction in gold’s long-term role as a monetary asset and portfolio hedge.

The extraordinary monetary expansion of the past 15 years has permanently altered the baseline against which we measure monetary policy. Even as central banks engage in quantitative tightening, balance sheets remain orders of magnitude larger than pre-2008 levels. This elevated baseline, combined with fiscal pressures, aging demographics, and geopolitical uncertainty, suggests that monetary policy will remain accommodative by historical standards for the foreseeable future.

For investors, these conditions create a favorable backdrop for maintaining meaningful gold allocations regardless of near-term tactical considerations. The precious metal’s 5,000-year history as a store of value and its modern role as portfolio diversifier become increasingly relevant in an era of unprecedented monetary experimentation.

Whether you’re seeking to hedge against future inflation, protect purchasing power from currency debasement, or simply diversify a portfolio heavily weighted toward financial assets, understanding quantitative easing’s impact on gold provides essential context for informed decision-making.

Bullion Trading LLC stands ready to help investors of all sizes establish positions in physical gold, silver, platinum, and palladium, backed by market expertise and commitment to investor education.