A wave of sensational claims about a silver critical mineral export ban has swept through social media and some corners of the precious metals community.The allegation? That the United States has secretly banned silver exports through an executive order, triggering emergency powers and fundamentally reshaping the silver market overnight.

The reality is far less dramatic, but considerably more important to understand.

Silver has indeed received increased attention from U.S. policymakers as a strategically important metal. However, the leap from “strategically important” to “export ban under emergency powers” represents a significant misreading, or in some cases deliberate misrepresentation, of what has actually occurred.

Let’s examine what the evidence actually shows.

What Has Actually Happened with Silver’s Designation

The U.S. Geological Survey maintains an official list of critical minerals that is updated periodically according to the Energy Act of 2020. This list identifies non-fuel minerals essential to U.S. economic and national security that face supply chain vulnerabilities.

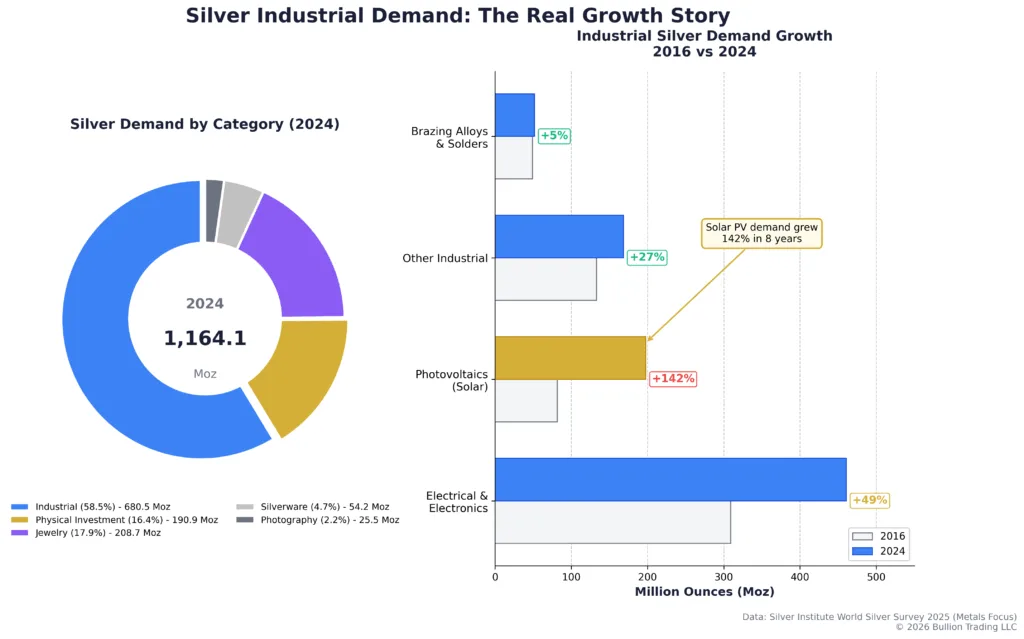

Silver’s strategic importance has long been recognized. The metal is essential to defense electronics, military applications, power generation infrastructure, and advanced manufacturing technologies. According to The Silver Institute, industrial demand now accounts for approximately 59% of total silver usage, with the electrical and electronics sector driving unprecedented consumption growth.

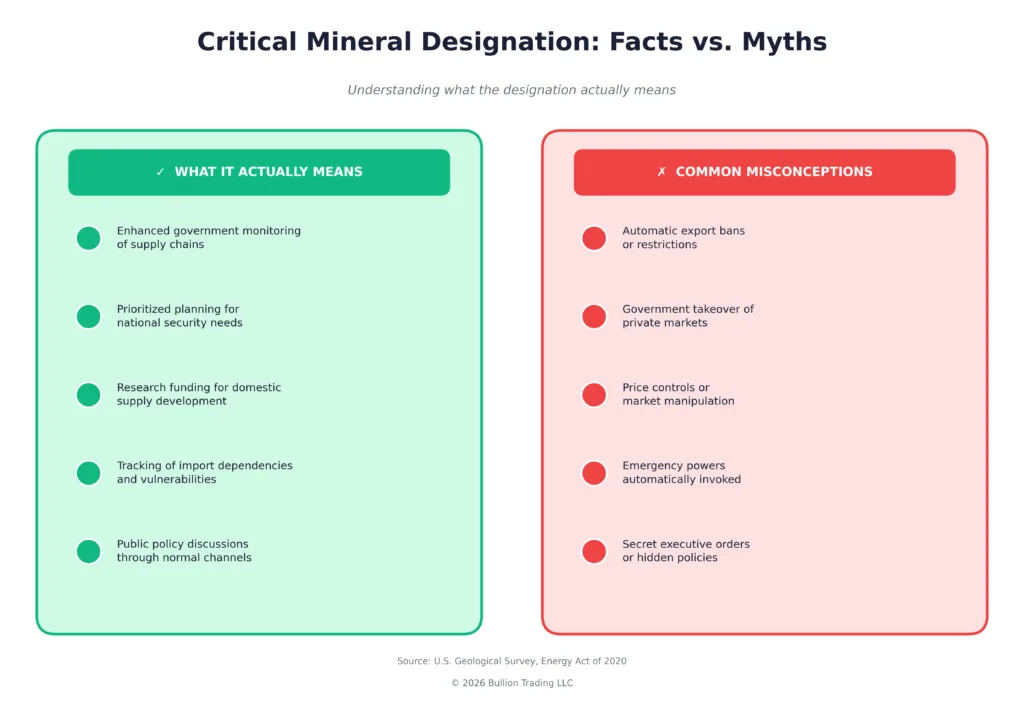

What a critical mineral designation actually means is straightforward: the mineral becomes subject to enhanced monitoring, supply chain analysis, and prioritized planning. Federal agencies track domestic production, import dependencies, and potential vulnerabilities. Research funding may be directed toward domestic supply development or recycling technologies.

What it does not mean is equally important: designation as a critical mineral does not automatically trigger export restrictions, government takeover of markets, price controls, or emergency powers. Those outcomes would require separate, specific, and very public government actions.

The Missing Evidence Problem

If the United States had actually restricted silver exports, the evidence would be impossible to hide. International trade operates under detailed regulatory frameworks that generate extensive documentation. Any export restriction would require formal Bureau of Industry and Security notices, Department of Commerce directives, and updates to export control regulations published in the Federal Register.

Refiners, wholesalers, and dealers would receive official guidance. The London Bullion Market Association and COMEX would update their rules. Customs declarations would reflect new requirements. None of these exist.

The White House presidential actions page maintains a comprehensive public record of executive orders and proclamations. A search of recent actions reveals no silver export restrictions, no invocation of the Defense Production Act regarding silver, and no emergency declarations affecting precious metals markets.

This absence of documentation is not a technicality. When governments restrict commodity exports, they do so through formal, published processes. The international trade system depends on predictable, transparent rules. Secret export bans would violate treaty obligations and trigger immediate diplomatic responses from trading partners.

Where the Confusion Originates

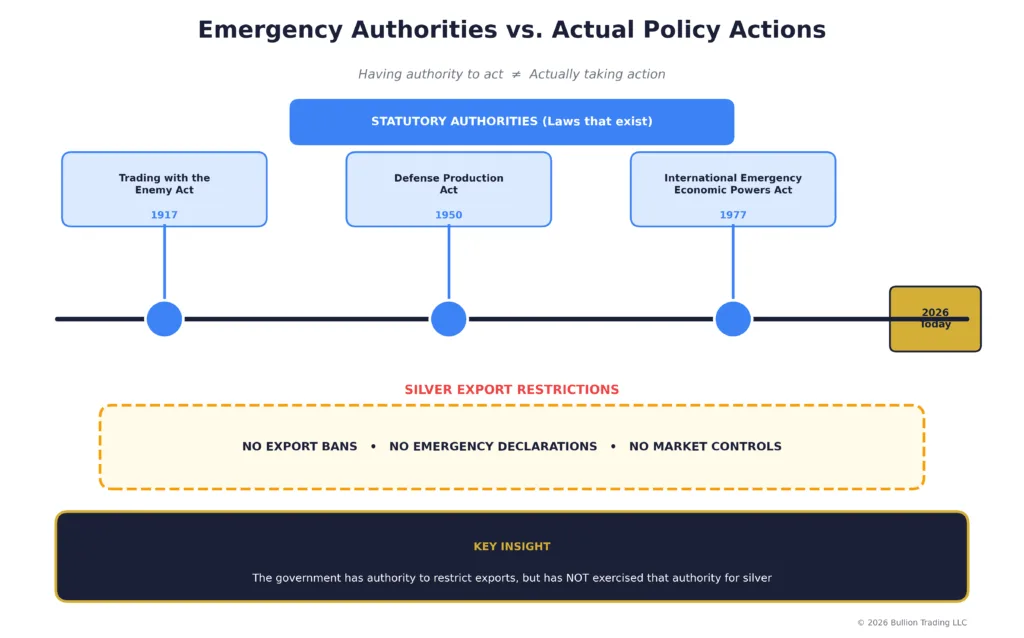

Much of the current narrative traces back to citations of old statutory authorities. The Trading with the Enemy Act of 1917, the International Emergency Economic Powers Act of 1977, and various provisions within the Defense Production Act grant the executive branch significant powers during declared emergencies. These laws have existed for decades.

The critical distinction that gets lost in translation: these statutes authorize potential action, they do not constitute action themselves. Saying the government “has the authority” to restrict exports is fundamentally different from saying the government “has restricted” exports. The first statement is true for dozens of commodities under various emergency provisions. The second statement requires actual invocation of those powers through formal processes.

This conflation appears to serve particular agendas. Some commentators benefit from creating urgency and fear around precious metals. Others may genuinely misunderstand the difference between statutory authority and policy implementation. Regardless of intent, the effect is the same: misinformation spreads rapidly while accurate context struggles to keep pace.

The Real Silver Supply Picture

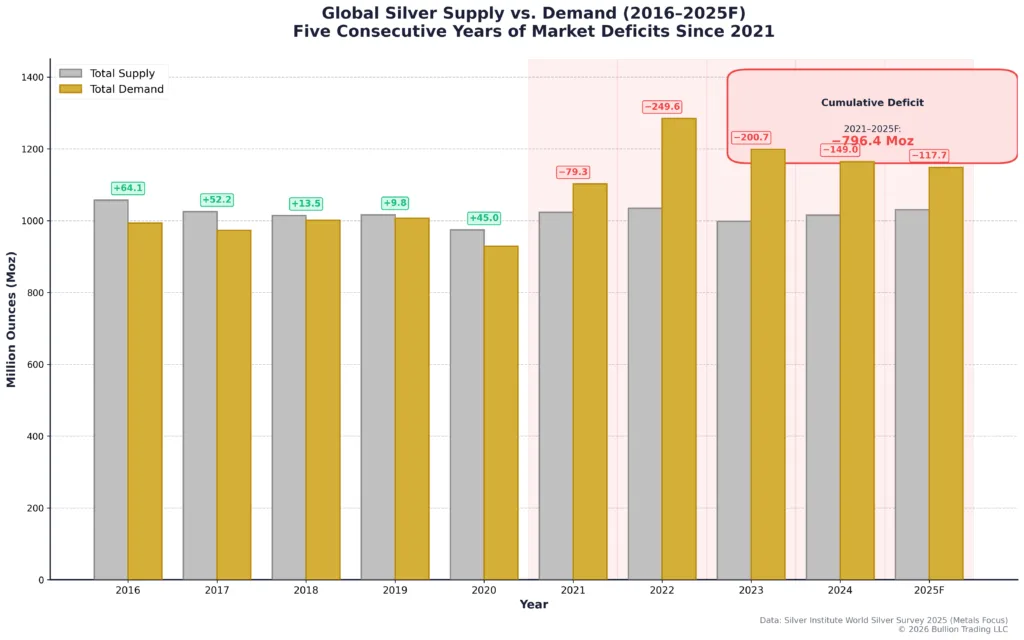

While export ban claims fall apart under scrutiny, silver’s supply situation does present genuine considerations worth understanding. According to Sprott’s Silver Investment Outlook, the global silver market has operated in structural deficit since 2021, with cumulative shortfalls totaling nearly 800 million ounces through 2025.

Industrial demand continues to surge. The Silver Institute reports that global silver mine production reached 819.7 million ounces in 2024, up just 0.9% year over year. Meanwhile, electrical and electronics demand has grown 51% since 2016, driven by solar photovoltaics, consumer electronics, automotive applications, and grid infrastructure development.

Solar photovoltaic demand alone now accounts for approximately 17% of total silver demand, compared to 5.6% in 2015. China increased its solar capacity by 45% in 2024, creating enormous demand for silver used in panel manufacturing. This industrial consumption is largely price-inelastic in the short term, as manufacturers cannot simply pause production when metal becomes tight.

Silver prices have reflected these fundamentals. According to Sprott data, silver gained nearly 25% in the first half of 2025, breaking above $35 per ounce and reaching levels not seen in over a decade. These gains occurred through normal market mechanisms responding to supply and demand dynamics, not government intervention.

Understanding Lease Rates and Market Tightness

Some of the export ban narrative appears connected to genuine market tightness that has affected silver in recent years. Analysis of gold and silver lease rates shows that borrowing costs for physical metal have spiked repeatedly, reflecting supply chain stress and strong demand.

These elevated lease rates indicate temporary tightness in deliverable inventory, not fundamental shortages or government intervention. Metal that exists in one form, such as large institutional bars, cannot instantly transform into retail coins and small bars. Metal located in London vaults takes time to ship to New York. Refiners prioritize processing efficiency, meaning retail products can face delays during demand surges.

Market observers noting these conditions sometimes interpret them as evidence of crisis. However, the precious metals market has experienced similar episodes before and rebalanced as supply chains adjusted. High lease rates signal that immediately deliverable metal commands a premium, not that silver is disappearing or being hoarded by governments.

What Investors Should Actually Watch

Rather than chasing unverified claims about secret government actions, investors benefit from monitoring legitimate policy developments. The Department of Commerce conducts Section 232 investigations that can lead to tariffs or other trade measures, though these processes are public and well-documented.

Congressional activity around critical minerals legislation represents another area worth attention. Bipartisan interest in supply chain security has grown, and new legislation could affect mining permitting, recycling incentives, or strategic reserve policies. Any significant changes would emerge through the normal legislative process with ample public notice.

International trade relationships matter as well. China dominates solar panel manufacturing and has been a major driver of silver demand growth. Any significant shift in U.S.-China trade policy or Chinese industrial capacity would affect silver markets more than hypothetical export restrictions.

Most importantly, the fundamental supply and demand picture continues to support silver prices through entirely normal market mechanisms. Industrial demand growth, investment interest, and constrained mine supply create a supportive environment without requiring conspiratorial narratives.

The Problem with Fabricated Urgency

Sensational claims about government takeovers and secret export bans do real damage to investor decision-making. When people believe emergency actions are imminent, they may make purchases at unfavorable prices or panic sell positions based on false premises. They may allocate more to silver than appropriate for their portfolios, or less, depending on how they interpret the misinformation.

The precious metals market has enough genuine factors supporting investment consideration. Central bank buying of gold continues at elevated levels. Industrial demand for silver in green energy applications represents a structural shift. Inflation concerns and geopolitical tensions create legitimate safe-haven interest.

These real fundamentals do not require exaggeration or fabrication. The case for precious metals ownership stands on actual supply constraints, documented demand growth, and verifiable macroeconomic conditions. Layering conspiracy theories on top of this foundation undermines credibility and clouds judgment.

Separating Signal from Noise

Silver’s strategic importance to the American economy is real and growing. Government recognition of this importance through critical mineral frameworks reflects genuine policy priorities. Industrial demand continues to outpace supply growth, creating a supportive fundamental environment.

None of this requires or benefits from claims about secret executive orders, emergency powers invocations, or market takeovers that have not actually occurred.

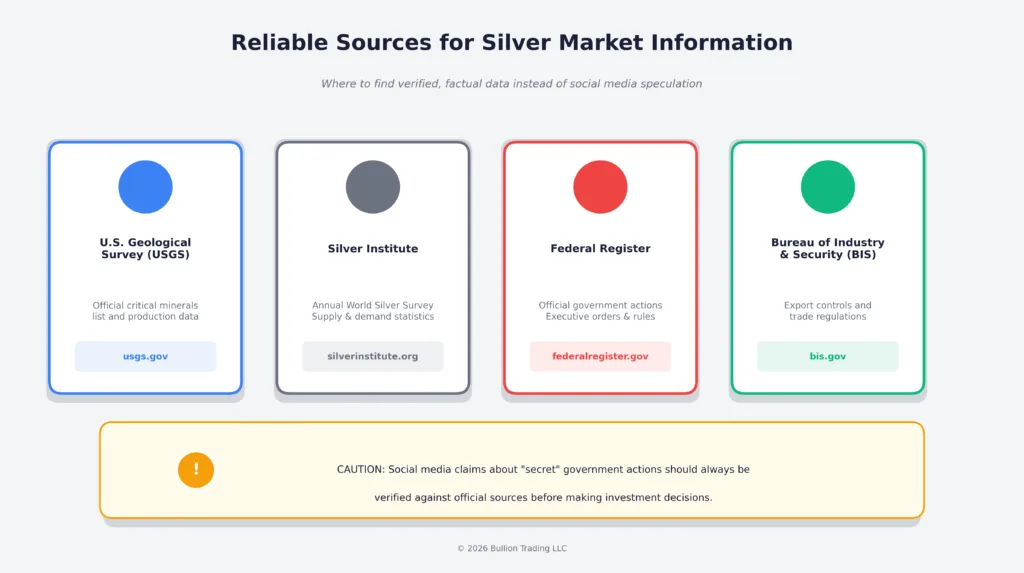

For investors evaluating silver positions, the focus should remain on verifiable information from credible sources. The USGS publishes mineral production data. The Silver Institute tracks supply and demand dynamics. The Federal Register documents actual government actions. These resources provide the foundation for informed decisions.

At Bullion Trading LLC, we believe investors deserve accurate information about precious metals markets. Whether you’re considering your first silver purchase or managing an established precious metals allocation, decisions should rest on facts rather than speculation. Our team remains committed to providing reliable market insight and access to quality physical metal, backed by genuine expertise rather than manufactured urgency.

The silver market offers legitimate investment considerations without requiring belief in unverified government conspiracies. The real story, persistent deficits, industrial demand growth, and supply constraints, provides more than enough substance for thoughtful portfolio decisions.