In a remarkable turn of events that has caught many investors off guard, silver outpaces gold in what has become one of the most compelling precious metals stories of 2025. While gold has captured headlines with its impressive surge to record highs above $3,500 per ounce, silver has been quietly staging an even more remarkable performance that deserves serious attention from both institutional and retail investors alike.

The white metal’s combination of persistent supply deficits, surging industrial demand, and recent recognition as a critical mineral has created a unique investment opportunity. As silver outpaces gold in percentage gains, it’s increasingly drawing attention from investors who recognize the fundamental shifts taking place in this overlooked market.

Silver’s Stellar Performance Exceeds Gold’s Historic Rally

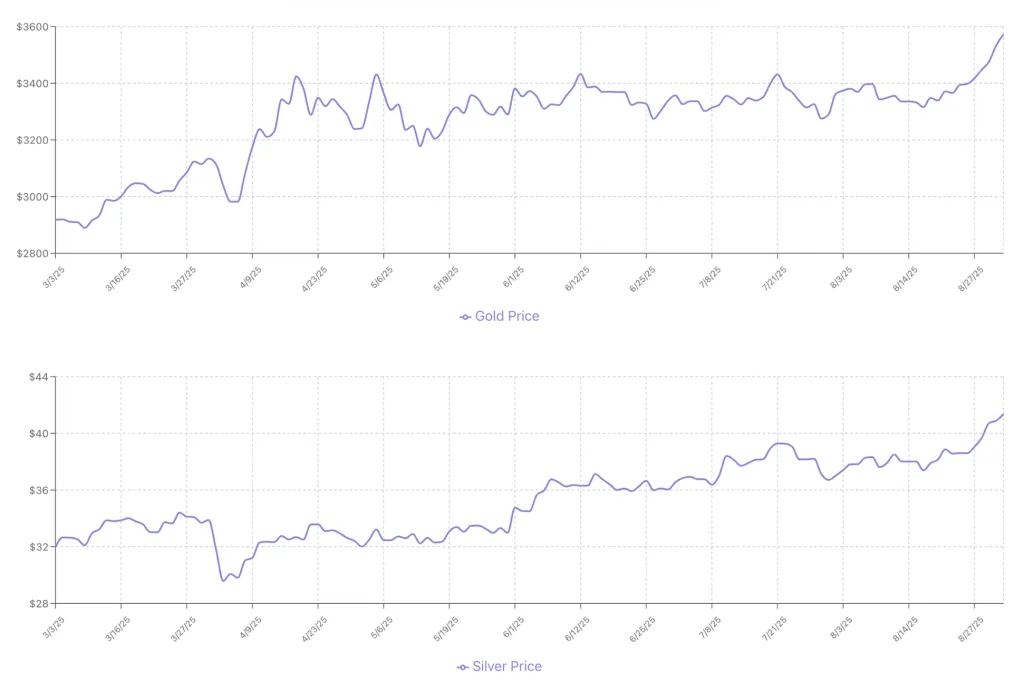

Silver has demonstrated exceptional strength throughout 2025, building on its momentum from 2024. Through the first six months of 2025, silver bullion gained an impressive 24.94%, following its 21.46% rise in 2024. This performance becomes even more notable when compared to gold’s already strong showing during the same period.

The price dynamics tell a compelling story of silver’s momentum. From approximately $30 per ounce at the beginning of 2025, silver has surged to trading levels around $40-41.40 per ounce by late August 2025, representing gains that have outpaced gold’s percentage increases despite gold reaching absolute record highs above $3,500 per ounce.

The Fifth Consecutive Year of Supply Deficits

The fundamental driver behind silver’s exceptional performance lies in an increasingly acute supply-demand imbalance. The silver market is forecast to record another significant deficit for the fifth consecutive year in 2025, with industrial demand remaining the key catalyst for this favorable dynamic.

According to the Silver Institute’s latest projections, the global silver deficit is expected to narrow by 21% to 117.6 million troy ounces in 2025 due to a 1% fall in demand and a 2% increase in total supply. While this represents some improvement from 2024’s deficit of 148.9 million ounces, it still marks a substantial structural imbalance that continues to support higher prices.

The persistence of these deficits is particularly noteworthy given that new mining projects typically require 3-5 year lead times, meaning supply cannot quickly respond to higher prices or increased demand. This structural constraint provides a strong foundation for continued price appreciation.

Industrial Demand Reaches New Records

The industrial sector’s appetite for silver continues to break records, driven primarily by green economy applications and technological innovation. Silver industrial demand rose 4 percent in 2024 to 680.5 million ounces, reaching a new record high for the fourth consecutive year. This trend shows no signs of slowing in 2025.

Silver industrial fabrication is forecast to grow by 3 percent this year, with solar panel manufacturing continuing to be a major driver. The photovoltaic sector alone consumes approximately 20% of global silver supply, and with the accelerating transition to renewable energy, this demand is expected to grow substantially.

Beyond solar applications, silver’s unique properties make it indispensable in:

- Electric vehicle components and charging infrastructure

- 5G telecommunications equipment

- Medical devices and antimicrobial applications

- Artificial intelligence hardware and data centers

- Advanced electronics and semiconductor manufacturing

Critical Mineral Designation: A Game-Changing Development

Perhaps the most significant development for silver in 2025 has been its official designation as a critical mineral by the United States government. As noted in our recent market analysis, silver was formally added to the US Critical Minerals List as of August 26, 2025, bringing the total list to 54 minerals.

This classification represents a fundamental shift in how silver is viewed by policymakers and could have far-reaching implications:

- Potential government stockpiling initiatives

- Priority access to mining permits and development support

- Enhanced supply chain security measures

- Increased investment in domestic production capabilities

- Strategic importance in national security planning

This new status acknowledges silver’s dual role beyond its traditional precious metals classification, recognizing its strategic importance in critical technologies and infrastructure.

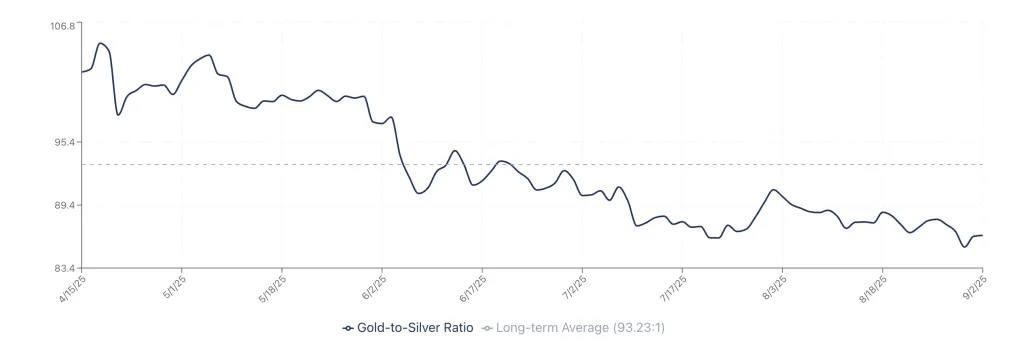

The Gold-Silver Ratio Signals Opportunity

The gold-silver ratio is hovering at around 86:1, indicating that silver is on sale when priced in gold. As of June 2025, the GSR was approximately 92, well above its long-term historical average.

Historically, when the ratio becomes this distorted, it tends to snap back toward the mean, which has averaged closer to 60-70 in recent decades. This suggests significant potential for silver to outperform gold as the ratio normalizes, providing an additional catalyst for price appreciation beyond fundamental supply-demand dynamics.

Investment Demand Strengthens Alongside Industrial Usage

While industrial applications drive the fundamental demand story, investment demand for silver has also shown remarkable strength. Physical silver investment, including bars and coins, has surged as investors recognize both the metal’s industrial importance and its potential as an inflation hedge.

The trend toward taking physical delivery of precious metals, which we’ve observed intensifying throughout 2025, has been particularly pronounced in silver markets. Exchange-traded funds (ETFs) backed by physical silver have seen steady inflows, while retail demand for silver coins and bars remains robust across major markets.

Supply Constraints Intensify the Squeeze

On the supply side, silver faces unique challenges that compound the deficit situation:

- Approximately 70% of silver production comes as a byproduct of other mining operations (primarily copper, lead, and zinc), meaning production cannot easily scale up in response to price signals

- Primary silver mines face declining ore grades and rising production costs

- Geopolitical tensions and trade policies affect supply chains, particularly given concentration in key producing regions

- Environmental regulations increasingly constrain new mine development

These structural supply limitations suggest that even with modest increases in mine production forecast for 2025, the market will struggle to close the demand gap in the near term.

Market Outlook and Price Projections

Leading financial institutions maintain bullish outlooks for silver, with many analysts projecting continued outperformance relative to gold. Historically, silver has outperformed gold during 12 major crisis events since 1979, benefiting from dual investment and industrial demand.

The combination of:

- Persistent supply deficits extending into their fifth year

- Record industrial demand driven by green technology

- Critical mineral designation providing policy support

- An elevated gold-silver ratio suggesting relative undervaluation

- Growing investment demand for physical metal

creates a compelling case for continued price appreciation through the remainder of 2025 and beyond.

Risk Factors and Considerations

While the outlook for silver appears highly favorable, investors should consider potential headwinds:

- Global economic slowdown could temporarily reduce industrial demand

- Dollar strength might create short-term price pressure

- Volatility remains higher in silver than gold markets

- Potential demand substitution in some industrial applications if prices rise too rapidly

However, the structural supply deficit and growing importance of silver in critical technologies suggest these risks are likely to create buying opportunities rather than sustained price weakness.

Strategic Positioning for the Silver Surge

The current environment presents several key considerations for precious metals investors:

Silver’s Dual Advantage: Unlike gold’s primarily monetary role, silver benefits from both safe-haven demand and industrial growth drivers, providing multiple catalysts for appreciation.

Supply Deficit Reality: With five consecutive years of deficits and limited near-term supply response capability, the fundamental case for higher prices remains intact.

Critical Infrastructure Play: Silver’s new critical mineral status positions it as essential to national security and technological advancement, potentially attracting new categories of strategic investors.

Relative Value Opportunity: The elevated gold-silver ratio suggests silver offers superior upside potential for investors looking to gain precious metals exposure.

The Bottom Line

Silver’s outperformance of gold’s already impressive rally reflects a unique confluence of factors that extend well beyond typical precious metals dynamics. The persistent supply deficit, now in its fifth year, combined with record industrial demand and new critical mineral recognition, creates a compelling investment narrative that’s increasingly difficult to ignore.

For investors seeking exposure to precious metals, silver’s combination of industrial indispensability and monetary characteristics offers a differentiated opportunity in today’s market environment. While gold maintains its traditional role as the ultimate safe-haven asset, silver’s diverse demand drivers and structural supply constraints position it for potentially superior returns as we move through the remainder of 2025 and beyond.

The formal recognition of silver as a critical mineral marks a watershed moment that could reshape market dynamics for years to come, providing additional support beyond traditional supply-demand fundamentals. As industrial applications continue to expand and supply struggles to keep pace, silver’s rally appears to have strong foundations for continuation.

At Bullion Trading LLC, we help clients understand these evolving market dynamics and position appropriately for silver’s unique opportunity in the current environment of persistent supply deficits and surging industrial demand.