While gold and silver often dominate precious metals conversations, a lesser-known family of metals quietly powers the backbone of our digital age. The platinum group metals (PGMs) – platinum, palladium, rhodium, ruthenium, iridium, and osmium – are experiencing unprecedented demand from the electronics industry that could fundamentally transform their market dynamics for the next decade and beyond.

The global platinum group metals market was valued at USD 19.50 billion in 2024 and is estimated to reach from USD 20.55 billion in 2025 to USD 31.30 billion by 2033, growing at a CAGR of 5.4% during the forecast period. This isn’t just growth, it’s a fundamental shift positioning these ultra-rare metals at the heart of humanity’s technological evolution.

The Digital Revolution’s Secret Ingredients

Every smartphone, laptop, and data center relies on platinum group metals to function. These remarkable elements possess unique properties that make them irreplaceable in modern electronics: exceptional electrical conductivity, unmatched resistance to corrosion, extreme durability under harsh conditions, and the ability to maintain performance at microscopic scales.

Unlike conventional materials that deteriorate or lose efficiency over time, PGMs maintain their properties even in the most demanding electronic applications. This reliability has made them indispensable as our devices become smaller, faster, and more complex.

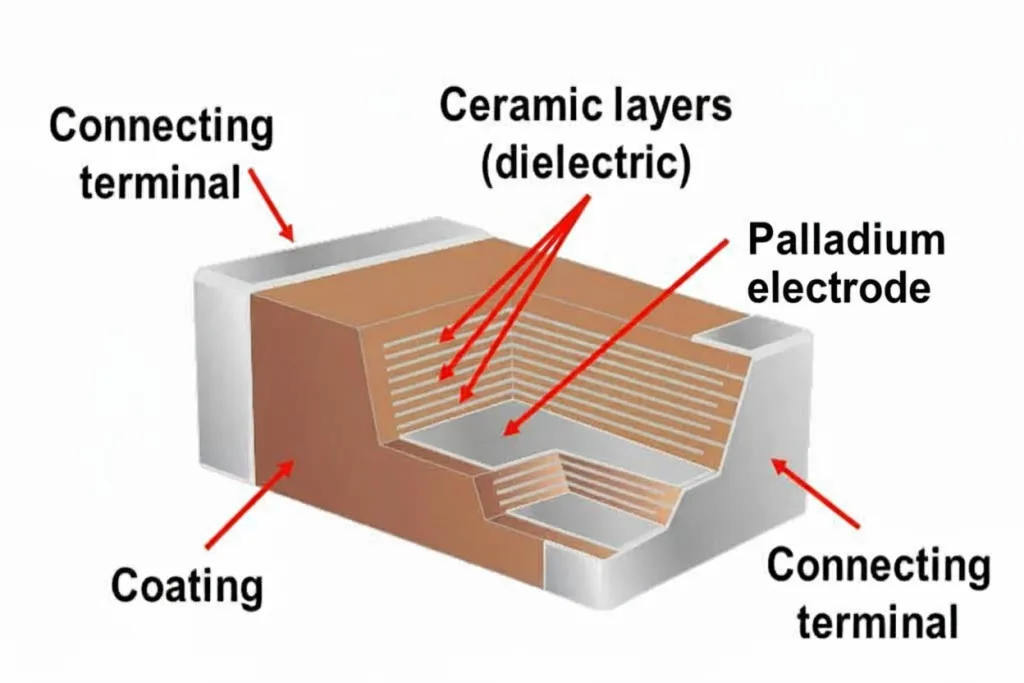

Palladium: The Capacitor King

At the heart of virtually every electronic device lies a component most consumers never see: the multi-layer ceramic capacitor (MLCC). These tiny components, often smaller than a grain of rice, are essential for managing electrical flow in everything from smartphones to electric vehicles. And palladium plays a starring role in their construction.

MLCCs for Automotive Electronics Market was valued at 12800 million in 2024 and is projected to reach US$ 19680 million by 2032, at a CAGR of 6.5% during the forecast period. This explosive growth in automotive applications alone demonstrates palladium’s critical importance to our technological infrastructure.

The automotive sector’s transformation is particularly striking. Modern vehicles, especially electric and autonomous models, require thousands of MLCCs for their sophisticated electronic systems. Battery management systems, power inverters, autonomous driving sensors, and infotainment displays all depend on palladium-containing capacitors to function reliably.

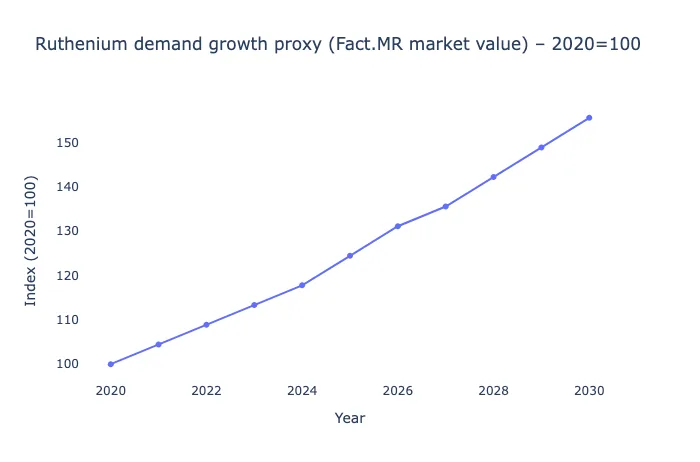

Ruthenium: The Data Storage Champion

While cloud computing and artificial intelligence capture headlines, few realize that ruthenium, one of the rarest elements on Earth, makes modern data storage possible. This ultra-rare metal has become indispensable to the hard disk drive industry, where it enables the massive storage capacities required for today’s data-hungry world.

Cloud computing expansion directly drives ruthenium consumption, with International Data Corporation (IDC) projecting hard disk sales to increase by 16% in 2025. This surge reflects the exponential growth in data generation from AI applications, streaming services, and enterprise cloud computing.

Johnson Matthey expects ruthenium demand to rise by 2% in 2025, with strong demand for hard disks for data centre expansions. The metal’s unique properties allow hard drives to achieve higher storage densities, making it possible to store more information in smaller spaces, a critical requirement as data centers strive for efficiency.

Platinum and Iridium: The Reliability Guardians

In applications where failure isn’t an option, medical devices, aerospace electronics, and critical infrastructure systems, platinum and iridium provide unmatched reliability. These metals form protective coatings on electrical contacts and serve as catalyst materials in specialized sensors.

Platinum’s role extends beyond traditional electronics into emerging technologies. Fuel cell systems for backup power in data centers, quantum computing components, and next-generation semiconductor manufacturing all rely on platinum’s unique properties. As these technologies scale from laboratory curiosities to commercial applications, platinum demand from the electronics sector is poised for significant growth.

The Supply Challenge: A Tightening Market

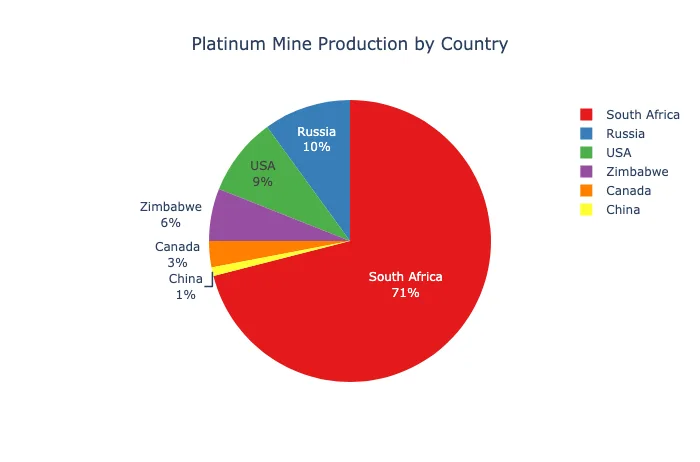

The surge in electronic applications creates a fascinating supply-demand dynamic for PGMs. Unlike gold, which can be mined as a primary product, most platinum group metals come as byproducts of platinum and nickel mining, primarily from South Africa and Russia.

South Africa will supply 71% of global primary ruthenium in 2025, according to Johnson Matthey. This geographic concentration creates supply chain vulnerabilities that could amplify price movements as demand accelerates.

The mining challenge is compounded by the complexity of PGM extraction. These metals occur in extremely low concentrations, requiring the processing of vast amounts of ore to produce even small quantities. New mine development takes years and billions in investment, meaning supply cannot quickly respond to demand surges.

The Technology Acceleration Factor

Several technological megatrends are converging to drive unprecedented PGM demand from the electronics sector:

5G and Beyond

The rollout of 5G networks requires massive infrastructure investments in base stations, antennas, and switching equipment, all containing PGMs. Each 5G base station uses significantly more electronic components than its 4G predecessor, multiplying the demand for palladium-containing capacitors and platinum-based connectors.

Artificial Intelligence and Machine Learning

AI’s computational demands are driving explosive growth in data center construction. These facilities require not just vast arrays of hard drives containing ruthenium, but also sophisticated cooling systems, power management electronics, and backup systems, all utilizing various PGMs.

Internet of Things (IoT)

Billions of connected devices, from smart home sensors to industrial monitoring equipment, each contain tiny amounts of PGMs. While individual device consumption is minimal, the sheer volume of IoT deployments creates substantial aggregate demand.

Electric and Autonomous Vehicles

Beyond the well-documented battery revolution, electric vehicles require sophisticated electronic control systems that dwarf traditional vehicles in complexity. Autonomous driving capabilities add layers of sensors, processors, and communication systems, each requiring PGM-containing components.

Investment Implications for Precious Metals Portfolios

For precious metals investors, the electronics revolution in PGMs presents unique opportunities distinct from traditional gold and silver investments:

Industrial Demand Dominance

Unlike gold, where investment and jewelry demand predominate, PGMs derive most of their value from industrial applications. This creates price dynamics less correlated with traditional precious metals drivers like monetary policy or currency fluctuations.

Supply Inelasticity

The Platinum Group Metals Market size is estimated at 637.51 tons in 2025, and is expected to reach 805.16 tons by 2030, at a CAGR of 4.75% during the forecast period. This relatively modest supply growth compared to exploding demand suggests potential for significant price appreciation.

Technology Leverage

PGM prices benefit from technological advancement rather than being threatened by it. As electronics become more sophisticated and ubiquitous, PGM consumption intensifies, creating a positive feedback loop for demand.

Portfolio Diversification

PGMs offer exposure to technology sector growth while maintaining the tangible asset characteristics precious metals investors value. This unique position provides portfolio benefits unavailable from either pure technology investments or traditional precious metals.

The Green Technology Multiplier

The electronics demand story intersects powerfully with the green energy transition. Renewable energy systems require sophisticated electronic controls, from solar inverter systems to wind turbine management computers. Energy storage systems, smart grids, and electric vehicle charging infrastructure all depend heavily on electronic components containing PGMs.

This creates a multiplier effect: green technologies drive both direct PGM demand (like platinum in fuel cells) and indirect demand through their electronic control systems. As governments worldwide accelerate renewable energy adoption to meet climate commitments, this dual demand driver could prove particularly powerful.

The Critical Materials Recognition

Governments globally are recognizing PGMs as critical materials essential for economic competitiveness and national security. The United States, European Union, and China have all identified platinum group metals as strategic resources requiring secure supply chains.

This recognition is leading to policy initiatives that could further support PGM markets, including strategic stockpiling programs, recycling incentives, domestic production support, and research into more efficient PGM utilization. These policies could provide additional price support beyond pure market dynamics.

Looking Forward: The Next Decade

The convergence of multiple technology trends positions platinum group metals for potentially explosive demand growth through 2035. Consider the scale of transformation ahead:

Data storage requirements are doubling every two years, driving relentless ruthenium consumption. Electric vehicle production is projected to increase ten-fold by 2035, multiplying palladium demand from automotive electronics. 5G networks will require millions of new base stations globally, each packed with PGM-containing components. Artificial intelligence applications are just beginning their growth trajectory, with computational demands growing exponentially.

The Recycling Factor

Unlike many industrial materials, PGMs retain their value and properties through recycling. Electronic waste recycling is becoming increasingly sophisticated, allowing recovery of PGMs from end-of-life devices. However, the rapid growth in electronic device deployment means recycling alone cannot meet surging demand.

The recycling challenge is particularly acute for newer applications. While catalytic converter recycling is well-established, recovering PGMs from complex electronic assemblies remains technically challenging and economically marginal. As PGM prices rise, recycling economics improve, but significant infrastructure investment will be required to capture these materials effectively.

Investment Strategies for the PGM Revolution

For investors looking to capitalize on the electronics-driven PGM boom, several approaches merit consideration:

Physical Metal Ownership

Direct ownership of platinum and palladium provides pure exposure to price movements. However, rhodium, ruthenium, and iridium markets are less accessible to retail investors, typically requiring specialized dealers and storage arrangements.

Mining Equity Exposure

Investing in PGM mining companies offers leveraged exposure to metal prices, though with additional operational and geographic risks. South African miners dominate global production, providing focused exposure but also political and currency risks.

Technology Integration Plays

Companies specializing in electronic components and materials offer indirect exposure to PGM demand growth. These firms often have pricing power that allows them to pass through raw material costs while benefiting from volume growth.

The Risk Factors

While the long-term demand outlook appears robust, investors should consider several risk factors:

Substitution efforts continue, though no materials have successfully replaced PGMs at scale. Economic downturns could temporarily reduce electronics demand, creating price volatility. Geopolitical tensions affecting South Africa or Russia could disrupt supply chains. Technology breakthroughs might reduce PGM requirements per device, though this could be offset by volume growth.

The Investment Timeline

The PGM electronics story is fundamentally long-term, driven by structural technology trends rather than cyclical factors. Investors should view PGM allocation as a multi-year position aligned with the ongoing digital transformation of the global economy.

Short-term volatility is likely as markets digest supply disruptions, demand surprises, and technology developments. However, the underlying trend toward greater electronic complexity and ubiquity provides a powerful secular tailwind for PGM demand.

The Bottom Line

Platinum group metals stand at the intersection of multiple transformative trends: digital revolution, green energy transition, transportation electrification, and artificial intelligence expansion. Their unique properties make them irreplaceable in critical electronic applications, while their rarity and supply constraints create compelling investment dynamics.

As electronic devices proliferate from smartphones to data centers, from electric vehicles to IoT sensors, PGM consumption is entering uncharted territory. The combination of surging demand and constrained supply creates market conditions that could support significantly higher prices over the coming decade.

For precious metals investors, PGMs offer a unique value proposition: exposure to technology sector growth while maintaining the tangible asset characteristics that make precious metals attractive portfolio components. Unlike traditional precious metals driven by monetary factors, PGMs benefit directly from technological advancement and adoption.

The electronics revolution is creating unprecedented demand for platinum group metals that extends far beyond traditional industrial applications. As our world becomes increasingly digital and connected, these remarkable metals transition from industrial commodities to strategic assets essential for technological progress. For investors willing to look beyond conventional precious metals, PGMs offer unique exposure to the most powerful trends shaping our technological future.

At Bullion Trading LLC, we help investors navigate these evolving market dynamics while understanding both opportunities and risks. Whether you’re diversifying beyond gold and silver or building focused exposure to technology-critical metals, platinum group metals represent a compelling addition to precious metals portfolios positioned for the digital age.