July 1944. The Mount Washington Hotel sits in the mountains of New Hampshire, packed with 730 delegates from forty-four Allied nations. World War II was still going. The outcome on the battlefield was far from settled. And yet these governments were already deciding what money would mean once the shooting stopped. The result was the “Bretton Woods System”: a framework in which the US dollar became the world’s reserve currency, every participating nation pegged its exchange rate to the dollar, and the dollar itself was fixed to gold at exactly $35 per troy ounce. For close to three decades, this arrangement governed how countries traded, settled debts, and stored national wealth. Then, on August 15, 1971, it ended. The effects are still playing out.

Why the world needed a new monetary system

To understand Bretton Woods, you need to understand what preceded it. The 1930s were, monetarily speaking, a sustained catastrophe. Countries responded to the Great Depression by raising tariffs, devaluing their currencies against each other, and erecting trade barriers wherever they could. These competitive devaluations destabilized international commerce without fixing the underlying economic problems. The gold standard, which had already been abandoned by most countries after World War I, never fully recovered. By the early 1940s it was dead in practice if not in name.

American policymakers drew a direct line between this monetary chaos and the political instability that produced the second world war. The thinking went like this: let international economic relations collapse and you get nationalism, resentment, and eventually armed conflict. Build a cooperative framework while there is still goodwill and political will to do so. The planning had to start before the war was over.

Work began in earnest in 1942. Two figures led the technical negotiations: John Maynard Keynes, representing the British Treasury, and Harry Dexter White, the chief international economist at the US Treasury Department. Their visions differed sharply. Keynes wanted a genuinely multilateral global central bank, which he called the Clearing Union, that would issue its own international currency called the “bancor” and penalize both surplus and deficit countries to keep trade balanced. He proposed raising $26 billion for the institution. White had a much more limited idea: a Stabilization Fund financed with a finite pool of national currencies and gold, initially set at $5 billion, with far less autonomous power. The United States would contribute more, but would also control more.

Given that America held roughly three-quarters of the world’s official gold reserves by the war’s end, the outcome was never really in doubt. The final agreement followed the White plan closely. According to the Federal Reserve History, the fund resources were eventually set at $8.5 billion, raised from White’s initial $5 billion figure as a concession to some of Keynes’s concerns about under-capitalization. It was a compromise, but not a symmetrical one.

How the system actually worked

The architecture was straightforward, though the balance it required was anything but. Every participating country agreed to peg its currency to the US dollar within a one-percent band. The dollar was fixed to gold at $35 per troy ounce. The United States committed to converting foreign-held dollars into gold at that price on demand, a promise that became known as “gold convertibility”. The IMF, created alongside the World Bank at Bretton Woods, was tasked with monitoring exchange rates, providing short-term financial support to countries running balance-of-payments deficits, and enforcing the rules. The World Bank’s mandate was reconstruction: funding the rebuilding of war-ravaged economies and the development of poorer nations.

It took over a decade for the system to become fully operational. European countries emerged from the war devastated and chronically short of dollars. The US encouraged currency devaluations to help European exporters earn the dollars they needed, which had the side effect of making American goods appear expensive to the rest of the world. Marshall Plan spending and the cost of maintaining US troops abroad pushed more dollars into global circulation. By 1958, enough recovery had occurred that major currencies became freely convertible, and the Bretton Woods system finally functioned as intended.

The arrangement gave the United States something no other country had: the ability to run persistent trade deficits without facing an immediate currency crisis. Because other nations needed dollars to conduct international trade, they tended to hold them rather than demand gold in exchange. This “exorbitant privilege”, a phrase coined by French Finance Minister Valéry Giscard d’Estaing, meant America could finance domestic programs and overseas military commitments partly by exporting dollars rather than real goods. It was a remarkable position. And, as with most arrangements that good, it contained the seeds of its own undoing.

The Triffin dilemma: why the system was always going to break

Belgian-American economist Robert Triffin identified the structural contradiction in 1960. His argument was simple and, as it turned out, correct. For the Bretton Woods system to work, the world needed an ever-growing supply of dollars to use as international reserves. The only way the United States could supply those dollars was to run persistent balance-of-payments deficits, spending more abroad than it received. As those deficits accumulated, the ratio of foreign-held dollars to American gold reserves would keep deteriorating. Eventually, foreign governments and central banks would lose confidence that the United States could actually honor its commitment to redeem dollars for gold at $35 an ounce. At that point, a run on gold would follow. Triffin presented this analysis to Congress in 1960. It described exactly what happened eleven years later.

Through the 1960s, the deficit grew. Vietnam War spending, the cost of maintaining American bases in Europe, and the foreign aid programs of successive administrations pushed dollars overseas at an accelerating rate. European and Japanese economies had rebuilt their industrial bases and were increasingly competitive with American exports. Demand for dollars as a trading currency was growing more slowly than the supply of them. The numbers were turning against the system.

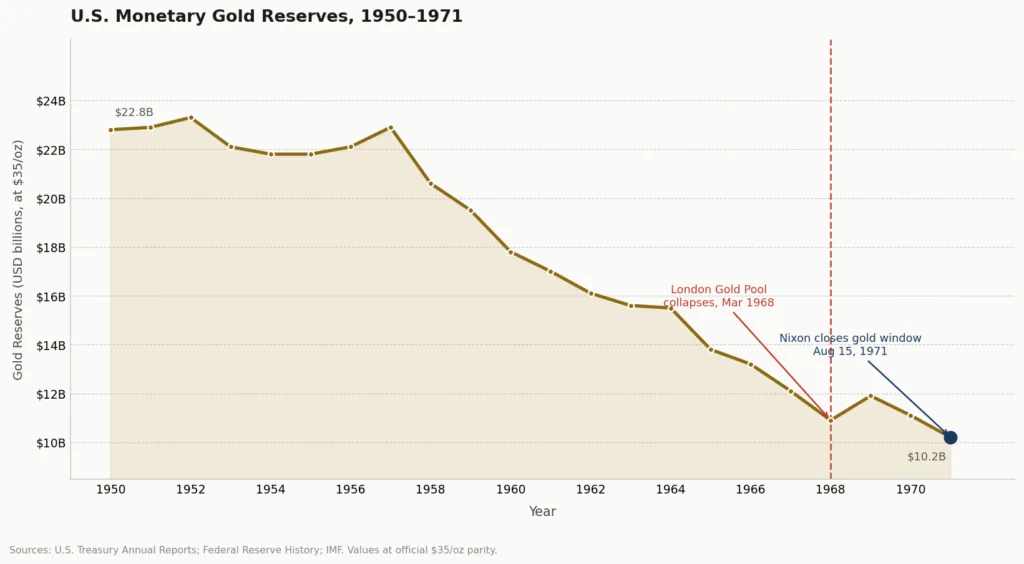

The London Gold Pool, formed in November 1961 by eight central banks including the United States, tried to hold the gold price at $35 per ounce through coordinated open-market interventions. It worked for six years. Then in March 1968, France withdrew from the pool after Britain devalued sterling and a gold run broke out across European markets. The pool collapsed. The remaining seven members agreed to a two-tiered arrangement: central banks would settle debts among themselves at $35 per ounce, but private gold markets would be left to find their own price. This was widely understood as a holding action, not a fix. Washington’s relationship with gold has always been complicated, shaped by decades of policy decisions that tried to suppress the metal’s market price when it was politically inconvenient to acknowledge what the dollar was actually worth.

By 1971, foreign-held dollar claims exceeded the entire US gold stock. The United States literally could not honor its commitments if major creditors called them in simultaneously. West Germany abandoned its dollar peg in May 1971. France, which had been aggressively redeeming dollars for gold under de Gaulle’s directive since the mid-1960s, accelerated its demands. Switzerland redeemed gold directly from the US Treasury. The run Triffin had predicted a decade earlier was underway.

August 15, 1971: the night Nixon closed the gold window

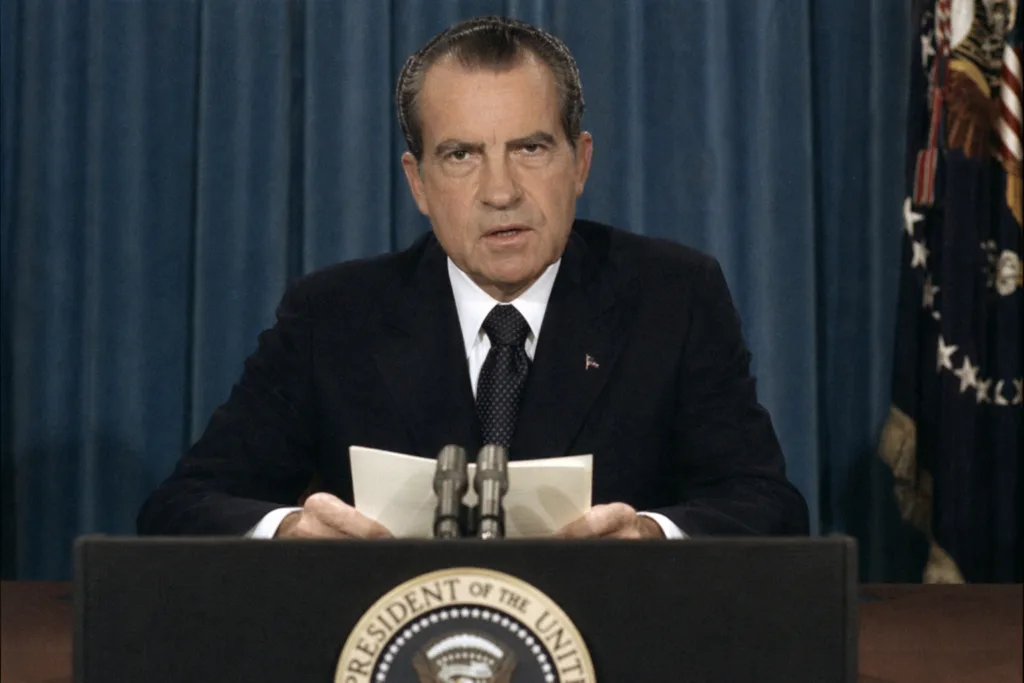

From August 13 to 15, 1971, Nixon gathered fifteen advisers at Camp David. The group included Federal Reserve Chairman Arthur Burns, Treasury Secretary John Connally, and a relatively young Paul Volcker, then serving as Undersecretary for International Monetary Affairs. They worked through the options and settled on a plan that Burns initially resisted, fearing the international fallout.

On the evening of August 15, Nixon addressed the nation and announced three things: the gold window was closed, a ninety-day freeze on wages and prices would take effect immediately, and a ten-percent import surcharge was being imposed. “I am determined that the American dollar must never again be a hostage in the hands of international speculators”, he said in that televised address. Foreign governments could no longer trade their dollar reserves for gold. The dollar became a fiat currency, its value backed not by a fixed quantity of metal but by the word of the US government and the depth of American financial markets.

The full story of how this single announcement dismantled a twenty-seven year monetary order is worth examining closely. The Nixon Shock and its consequences for gold markets did not fully materialize overnight. A final attempt to preserve fixed exchange rates, the Smithsonian Agreement of December 1971, technically raised the gold peg to $38 per ounce and realigned major currencies. It lasted about fifteen months. In March 1973, Germany, Japan, and the other major industrialized economies let their currencies float. As the Federal Reserve History documents, this was the moment the Bretton Woods system formally ended, though in practice it had been dead since August 1971.

What Bretton Woods left behind, and why it still matters

The world that emerged from 1973 runs on floating fiat currencies. No government promises to redeem its currency for gold. The IMF still operates, transformed from a rules-enforcer into a lender of last resort. The World Bank still funds development projects. The dollar remains the world’s primary reserve currency, but its grip on that role now rests on geopolitical weight, financial network effects, and a lack of credible alternatives rather than any gold promise.

For gold itself, the end of Bretton Woods was a release from three decades of artificial price suppression. In 1971, the official rate was $35 an ounce. By January 1980, the spot price touched $850. The metal was finally free to trade as a market asset, reflecting actual supply, demand, and investor sentiment rather than a bureaucratically fixed rate determined in 1944.

The deeper question Bretton Woods raises is about monetary discipline. The gold peg was an external constraint on American fiscal policy. As long as it existed, the United States could not run deficits indefinitely without eventually facing a gold drain and a potential currency crisis. Once that constraint was removed, the incentive to maintain fiscal balance weakened considerably. US federal debt stood at roughly $400 billion in 1971. It now exceeds $36 trillion. The relationship between the Federal Reserve, the gold standard, and government debt is not just historical trivia. It is the backstory for why central banks around the world have been quietly rebuilding their gold reserves since at least 2010, net buyers every year for over a decade.

The Bretton Woods experiment showed that gold-backed monetary systems can hold together for decades when the anchor country maintains discipline and the system serves everyone’s interests. It also showed that when those conditions stop holding, no amount of international cooperation can keep the structure standing. Whether the current dollar-based system faces its own version of that reckoning, and what gold’s role would be in the aftermath, is a question that serious investors and central banks are still very much working through.