For decades, the global gold market operated on a simple but fragile architecture. Bullion banks in London held vast quantities of “paper gold” on their balance sheets through unallocated accounts, essentially IOUs backed by fractional reserves of physical metal. The system worked because regulations treated these gold liabilities as essentially costless for the banks to carry. Basel III changed that. And the ripple effects are still reshaping the gold market today.

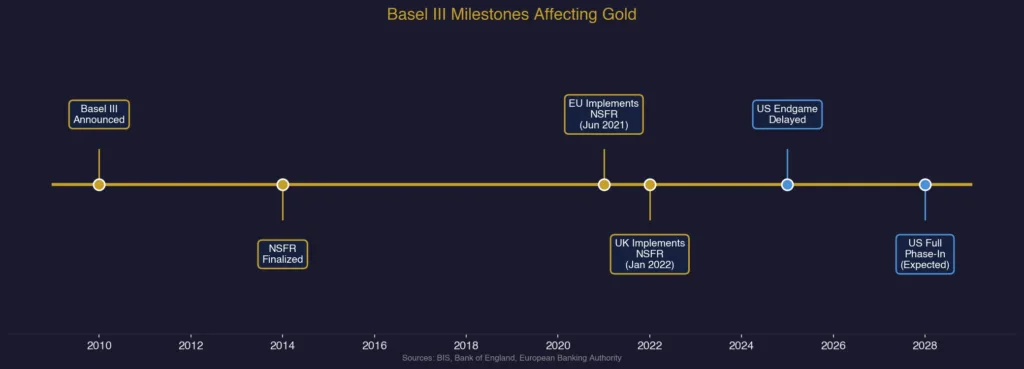

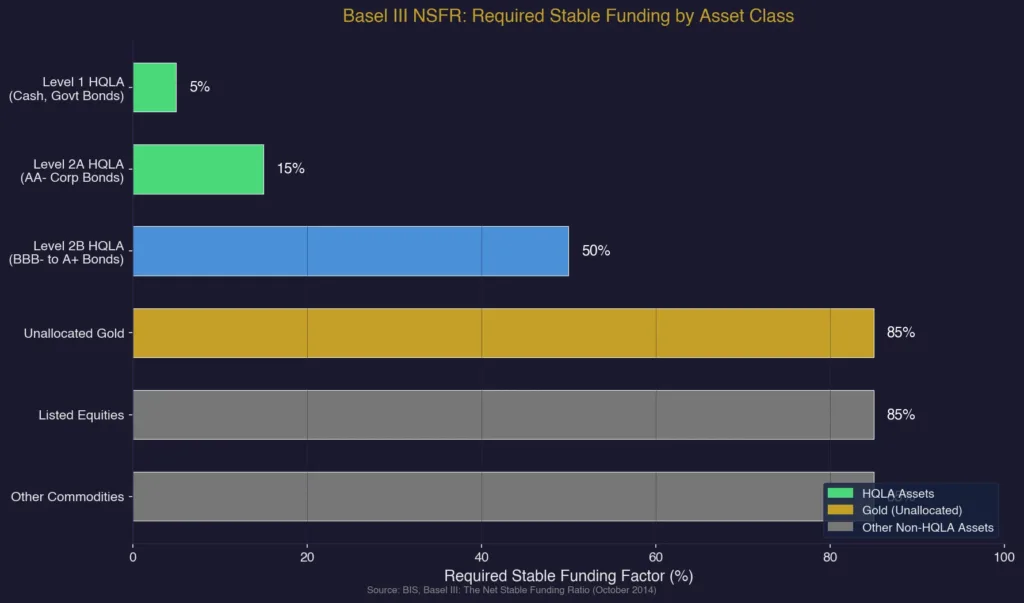

The Basel III banking framework, developed by the Basel Committee on Banking Supervision in response to the 2007-2009 financial crisis, introduced sweeping new rules on how banks fund their assets and manage liquidity. One of the less-discussed but most consequential changes involves the treatment of gold on bank balance sheets. Specifically, the Net Stable Funding Ratio (NSFR), finalized in October 2014, assigned physical and unallocated gold an 85% Required Stable Funding (RSF) factor. That single number has quietly become one of the most powerful structural forces in precious metals markets.

Meanwhile, the World Gold Council has spent years making the case that gold deserves recognition as a High Quality Liquid Asset (HQLA) under the related Liquidity Coverage Ratio (LCR). While gold has not yet received that official classification, the debate is far from settled. And the ongoing Basel III implementation, combined with record central bank gold buying and prices above $4,700 per ounce in April 2026, has brought the question of gold’s regulatory status back into sharp focus.

How Basel III Changed the Economics of Bank Gold Holdings

To understand why Basel III matters so much for gold, you need to understand how the bullion banking system worked before the rules changed. In the London Over-the-Counter (OTC) gold market, the world’s largest wholesale gold marketplace, most gold traded through unallocated accounts. When a client deposited gold in an unallocated account at a bullion bank, they did not own specific bars. Instead, the bank owed them a certain quantity of gold, similar to how a bank deposit works with cash. The client became an unsecured creditor of the bank, and the gold went onto the bank’s balance sheet as both an asset and a liability.

For the banks, this was extraordinarily efficient. Under the old regulatory regime, the funding cost of carrying these unallocated gold positions was minimal. Banks could create new unallocated gold obligations without needing to back them fully with physical metal, allowing a system where the volume of paper gold claims vastly exceeded the amount of physical gold in London vaults. The LBMA has historically reported daily gold clearing volumes in the hundreds of billions of dollars, dwarfing the physical metal actually available for delivery.

The NSFR changed the calculus. Under the rule, any asset on a bank’s balance sheet requires a corresponding amount of stable funding, proportional to the asset’s RSF factor. For unallocated gold, that factor is 85%. In practical terms, this means that for every $100 million of unallocated gold a bank holds on its balance sheet, it now needs $85 million in stable funding (equity, long-term debt, or stable deposits) to back it. That is a real, significant cost that simply did not exist before.

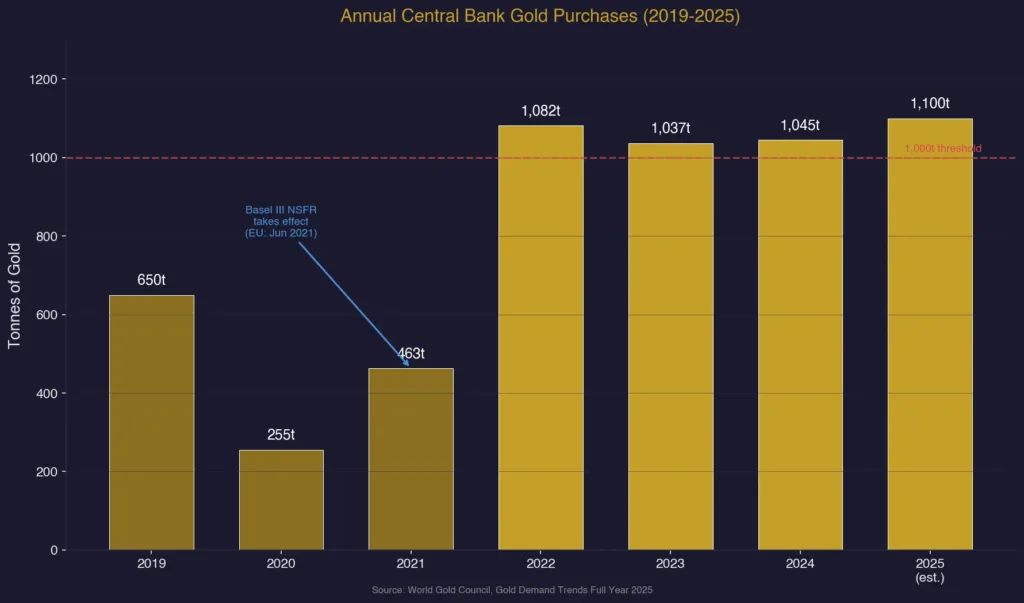

The European Union was the first major jurisdiction to implement the NSFR, with the rules taking effect on June 28, 2021. The United Kingdom followed on January 1, 2022, through the Prudential Regulation Authority (PRA). The timing matters because London is the heart of the global gold OTC market, and the PRA’s implementation directly affected the bullion banks that dominate gold trading worldwide. In the United States, the Basel III Endgame rules were originally expected to take effect by mid-2025, but facing fierce industry pushback, the timeline has been delayed and a full phase-in is not expected before 2028.

The Shift From Unallocated to Allocated Gold

The most tangible impact of the NSFR on the gold market has been a structural push away from unallocated gold and toward allocated gold. The distinction matters enormously. In an allocated gold account, the client owns specific, identifiable gold bars stored in a vault. The gold does not appear on the bank’s balance sheet because the bank is merely a custodian, not a debtor. And because allocated gold is off-balance-sheet, the 85% RSF factor does not apply.

This creates a straightforward financial incentive for banks: if they shift clients from unallocated to allocated accounts, they free up funding capacity and reduce their NSFR compliance costs. Over the past several years, this is exactly what the market has observed. Multiple bullion banks have encouraged or required clients to convert unallocated holdings into allocated accounts. The trend accelerated after the UK’s NSFR implementation in early 2022.

For the broader gold market, this shift has profound implications. When gold moves from unallocated to allocated status, it goes from being a fungible liability on a bank’s books to a physically segregated asset that cannot be lent or rehypothecated without the owner’s explicit permission. In other words, the “velocity” of paper gold declines. Less recycling of the same metal through multiple fractional claims means that the overall volume of synthetic gold supply shrinks relative to physical demand. And when synthetic supply contracts, the fundamental supply-demand balance tilts in favor of higher prices.

Gold’s Case for HQLA Status

Beyond the NSFR, an even bigger question looms: should gold be classified as a High Quality Liquid Asset under the Liquidity Coverage Ratio (LCR)? The LCR requires banks to hold enough HQLA to cover net cash outflows over a 30-day stress period. Currently, Level 1 HQLA includes cash, central bank reserves, and certain sovereign debt, assets that receive a 0% haircut. Level 2 HQLA includes corporate bonds and certain other securities, with haircuts of 15% to 50%. Gold is not included in any HQLA category.

The World Gold Council has long argued that gold meets the criteria for HQLA classification. Their position rests on several measurable characteristics. Gold trades in deep, liquid markets around the clock. The London gold market alone clears an estimated $30 to $50 billion in transactions daily. Gold prices have shown low correlation with traditional risk assets during stress periods, which is precisely when HQLA is needed. And unlike corporate bonds, gold carries zero credit risk because it is no one’s liability.

If gold were ever classified as HQLA, even at Level 2B with a 50% haircut, the impact would be transformative. Banks would have a regulatory incentive to hold physical gold as part of their liquidity buffers, creating a massive new source of institutional demand. A 2019 World Gold Council research paper estimated that even modest HQLA-driven allocations across the global banking system could generate hundreds of tonnes of annual demand. In the current market, where central banks are already buying more than 1,000 tonnes per year, that additional demand would further tighten an already strained supply picture.

The argument against HQLA status is not trivial, however. Regulators have pointed out that gold prices can be volatile in the short term, and that gold does not generate cash flows the way government bonds do. Converting gold to cash in a stress scenario requires a sale on the open market, which introduces price risk. These are legitimate concerns, and they explain why gold has not yet received the designation despite meeting many other HQLA criteria.

Central Banks Are Already Treating Gold as a Reserve Asset

While the regulatory debate about HQLA classification continues, central banks have effectively answered the question with their actions. According to World Gold Council data, central banks globally purchased over 1,000 tonnes of gold in each of 2022, 2023, 2024, and 2025. This buying wave, the most sustained in modern history, began accelerating after Russia’s foreign reserves were frozen by Western sanctions in February 2022. The message was clear: sovereignty requires assets that cannot be seized, frozen, or devalued by another government’s policy decisions.

Poland’s central bank has been among the most aggressive, with Governor Adam Glapinski publicly targeting a reserve allocation of 20% in gold. China’s People’s Bank of China added gold to its reserves for 18 consecutive months between late 2022 and early 2024, and has resumed reported purchases in 2025 after a brief pause. India, Turkey, Czech Republic, Singapore, and numerous other central banks have also been consistent buyers.

This central bank behavior is directly relevant to the Basel III gold HQLA debate. Central banks, the institutions that set and enforce banking regulations, are themselves accumulating gold at record levels as a core reserve asset. The disconnect between how sovereigns treat gold (as essential to financial security) and how their regulators classify it for commercial banks (as a non-HQLA commodity) is becoming harder to explain.

What This Means for Gold Prices and Investors

The Basel III NSFR’s impact on gold prices works through several channels, none of them flashy or immediate, but all structurally powerful. The shift from unallocated to allocated gold reduces the amount of synthetic gold supply in the market. The increased funding cost of holding unallocated positions discourages the kind of large-scale short selling that historically acted as a price suppressant. And the ongoing debate about HQLA classification keeps alive the possibility of a regulatory catalyst that could unlock significant new institutional demand.

These regulatory forces are compounding on top of other structural drivers. Geopolitical instability, from the ongoing reverberations of the Iran-Strait of Hormuz crisis to persistent U.S.-China tensions, continues to support safe-haven demand. Fiscal deficits in the United States and Europe show no sign of reversal, maintaining the inflationary backdrop that historically favors gold. And central bank buying remains a steady, price-insensitive source of demand that absorbs supply regardless of short-term price movements.

For individual investors, the practical takeaway is straightforward. The regulatory environment is moving in a direction that favors physical, allocated gold over paper claims. The system that allowed banks to create nearly unlimited synthetic gold supply at minimal cost is being systematically dismantled by Basel III. That does not mean gold prices can only go up. Markets are complex, and short-term corrections are inevitable. But the structural floor under gold prices is being reinforced by forces much larger than any single trade or market cycle.

The Basel III gold HQLA debate may seem like a technocratic detail, the kind of regulatory plumbing that most investors never think about. But it is reshaping the foundation of how gold trades, who holds it, and how much of it needs to exist in physical form. In a world where the largest financial institutions are being forced to fund their gold positions with real capital, and where central banks are buying physical metal at a pace not seen in living memory, the regulatory tailwinds behind gold are not going away anytime soon.