The precious metals market is generating headlines that might alarm investors: gold and silver lease rates have spiked to unprecedented levels in 2025, with silver lease rates reaching as high as 35% per annum and gold experiencing similar tightness. Retail dealers report shortages of popular coins and small bars, while social media amplifies concerns about a potential metals crisis. However, the reality behind these elevated lease rates tells a far more nuanced story, one of supply chain bottlenecks and temporary tightness rather than the catastrophic shortage some fear.

Understanding what’s actually happening in the gold and silver markets requires looking beyond sensational headlines to examine the mechanics of lease rates, the structure of precious metals supply chains, and the distinction between physical scarcity and logistical constraints. For investors navigating today’s volatile markets, this distinction could mean the difference between panic-driven decisions and strategic positioning.

What Are Gold and Silver Lease Rates?

At their core, gold and silver lease rates represent the cost of borrowing physical precious metals in the wholesale market. When banks, refiners, or industrial users need immediate access to metal they don’t currently possess, they can lease it from entities holding physical inventory, typically central banks, bullion banks, or large institutional holders.

The lease rate reflects supply and demand dynamics for immediately deliverable metal. When physical metal is readily available in the sizes and locations needed, lease rates remain low. However, when deliverable inventory tightens, whether due to strong demand, logistical constraints, or inventory being locked in the wrong form or location, lease rates spike.

According to LBMA analysis, elevated lease rates indicate “tightness” in the market, a temporary supply-demand imbalance for deliverable metal, rather than an absolute shortage. This distinction is crucial for understanding current market conditions.

The 2025 Lease Rate Surge: What’s Actually Happening

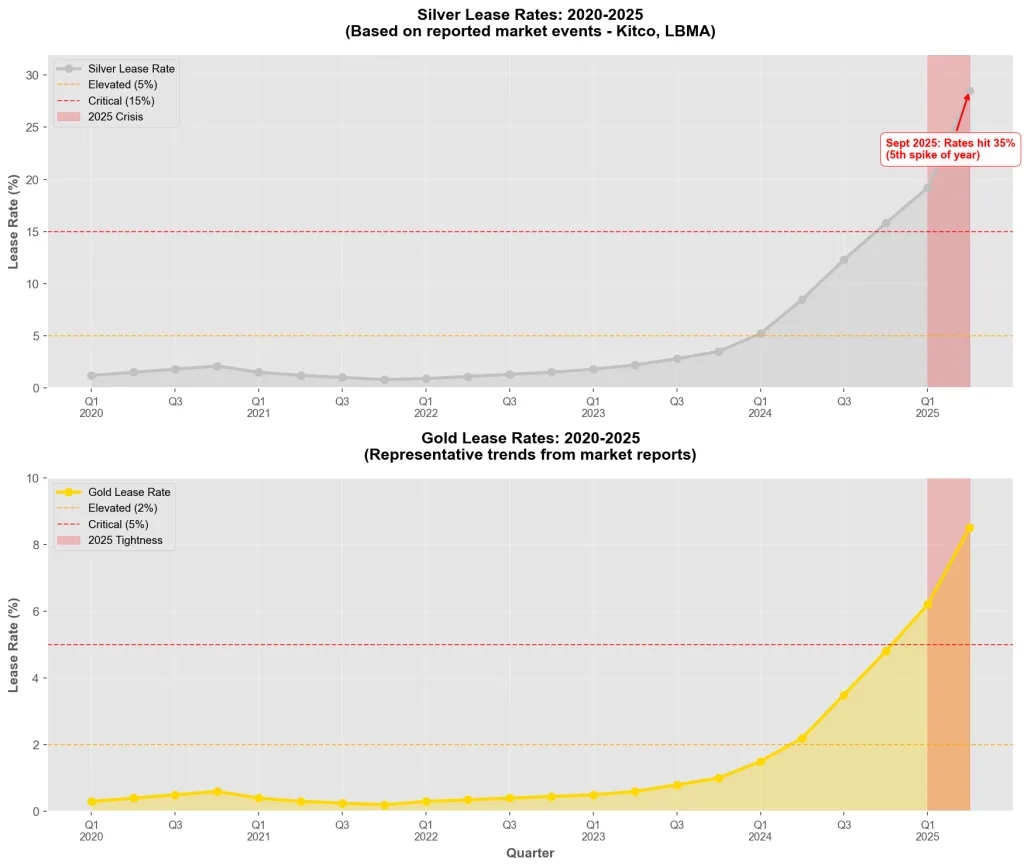

The precious metals market experienced dramatic tightness throughout 2025, with lease rates reaching levels that captured global attention. In September, silver lease rates spiked for the fifth time this year, with Bernard Dahdah, Precious Metals Analyst at Natixis, noting that silver’s go-forward rate reached unusual levels in negative territory around 1.2%.

“In layman’s terms, it means that the party borrowing silver is actually willing to pay rather than earn interest from the counterparty with which it will swap its USD for silver,” Dahdah explained. Meanwhile, those leasing out silver earned around 5.5% on a three-month basis, reflecting the premium for immediately available metal.

By October 2025, the situation intensified further. BullionVault reported that silver’s one-month lease rate almost tripled to reach more than 19% per annum, with subsequent spikes reaching 35% as silver prices touched new all-time highs above $50 per ounce.

Gold experienced similar tightness, though less extreme than silver. The combination of record prices, gold repeatedly breaking through $4,000 per ounce, and strong physical demand created conditions where immediately deliverable metal commanded substantial premiums.

These elevated rates prompted dramatic statements from market observers. “Silver squeeze is on. This is serious,” declared Bruce Ikemizu, former Tokyo precious metals banking director and current head of the Japan Bullion Market Association, as lease rates reached unprecedented levels.

Understanding the Supply Chain Bottleneck

The current market tightness stems not from a disappearance of gold and silver, but from a complex supply chain bottleneck affecting how metal flows through the global precious metals infrastructure. This bottleneck has multiple components that compound each other’s effects.

Refining Capacity and Prioritization

When metal prices surge, as they have throughout 2025, refiners face a flood of material to process. Industry reports indicate that silver refiners are building up significant backlogs as Americans liquidate jewelry, flatware, coins, and other silver items in response to 14-year price highs.

Refiners operate with clear efficiency priorities. Large institutional bars, 1,000-ounce silver bars and 400-ounce gold bars that meet London Bullion Market Association (LBMA) good delivery standards, take precedence because they can be processed more efficiently and serve the wholesale market where most metal trades.

Small retail products like one-ounce coins and bars require different production processes, specialized equipment, and more labor per ounce of output. When refiners are overwhelmed with raw material and orders for large bars, production of small retail forms naturally falls behind.

One bullion wholesaler this year apologized to customers, warning that processing times for silver batches had extended by a full week compared to just months earlier. This represents a significant but manageable delay, nothing like the six-month backlogs seen during the January 1980 silver peak, when COMEX futures traded at a 25% discount to spot prices because metal couldn’t be refined quickly enough to deliver against expiring contracts.

Geographic and Form Mismatches

The precious metals market faces another challenge: metal exists, but not always where or how it’s needed. London remains the world’s central storage and trading hub for wholesale bullion, but strong demand in specific markets creates localized tightness.

According to LBMA’s Q2 2025 Precious Metals Market Report, the dynamics of metal flows between trading centers significantly impact lease rates. When metal is locked in long-term storage, held as industrial inventory, or located in the wrong geographic market, it becomes effectively unavailable for immediate lending or delivery, even though it physically exists.

The Exchange for Physical (EFP) Premium

The dramatic widening of the Exchange for Physical (EFP) spread, the difference between COMEX futures prices and London spot prices, tells a revealing story. Natixis analysts noted that silver’s EFP expanded from a historic average of 25 cents to as much as $1.10 per ounce, suggesting extraordinarily strong U.S. demand for physical material.

This premium indicates that metal is flowing westward to New York from London at unprecedented rates. However, by October 2025, this pattern reversed, with New York futures trading at a discount to spot, suggesting over-supply in the U.S. and encouraging metal to flow back to London. These fluctuations reflect temporary imbalances in metal distribution rather than fundamental shortage.

Industrial and Investment Demand: A Perfect Storm

The 2025 tightness in precious metals markets reflects the convergence of multiple powerful demand drivers that are straining refining and distribution capacity simultaneously.

Silver’s Industrial Demand Surge

Sprott’s Silver Investment Outlook reveals that industrial demand accounts for 59% of silver usage, with the electrical and electronics sector emerging as the biggest demand driver. This sector’s silver consumption increased 51% since 2016, driven by solar photovoltaics, consumer electronics, automotive applications, and 5G networks.

Solar PV-specific demand alone accounted for 17% of total silver demand in 2024, compared to 5.6% in 2015, representing an annualized growth rate of 12.6%. China increased its solar capacity by 45% in 2024, creating enormous demand for silver used in panel manufacturing.

This industrial demand is non-discretionary and price-inelastic in the short term. Manufacturers building solar panels or electric vehicles cannot simply pause production when metal becomes tight; they must secure supply regardless of cost, putting upward pressure on lease rates as they scramble for immediately available metal.

Investment Demand Compounds Pressure

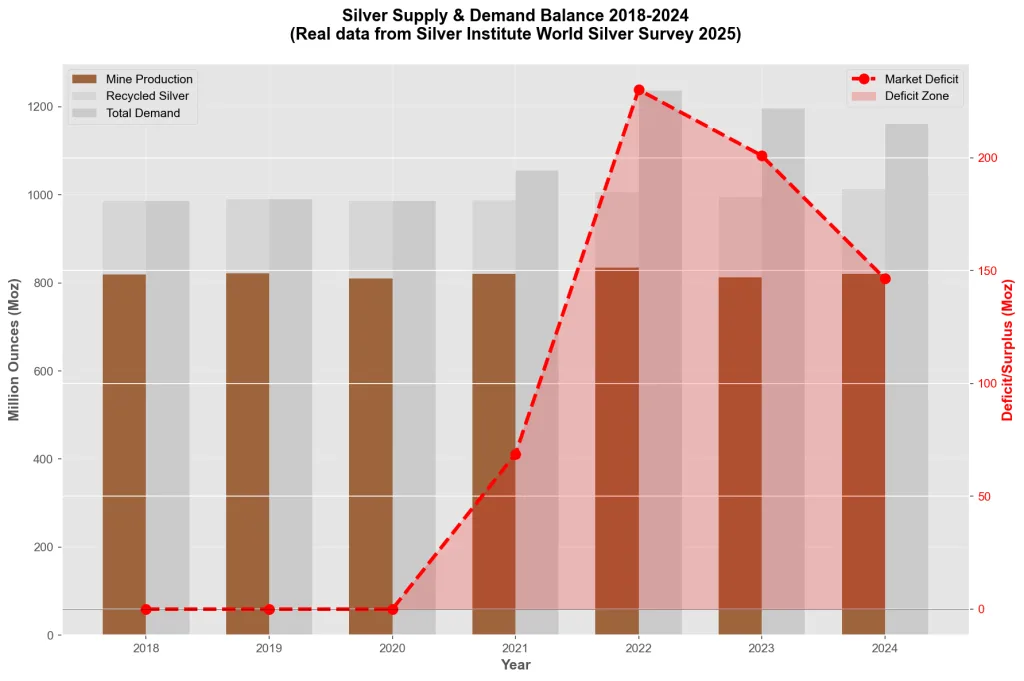

Alongside industrial demand, investment flows intensified throughout 2025. In the first half of the year alone, global silver-backed exchange-traded products experienced net inflows reaching 95 million ounces. The giant SLV silver ETF expanded to its largest size since September’s three-year highs, requiring 15,415 tonnes of metal to back its shares, equivalent to more than seven months of global silver mine output.

According to the Silver Institute, since 2019, more than 1.1 billion ounces have been drawn from “available mobile inventory” to satisfy both industrial demand and ETP backing requirements. This represents metal that was readily accessible for lending or trading being locked into forms where it cannot easily re-enter the liquid market.

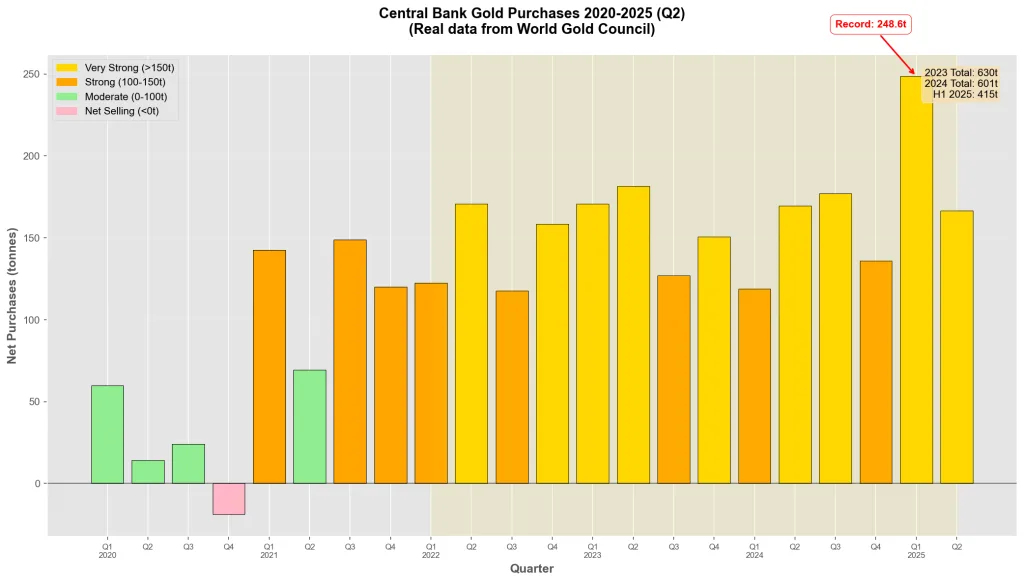

For gold, World Gold Council data shows central banks continuing to accumulate metal at near-record pace, with year-to-date purchases exceeding 800 tonnes and on track for another record year. This institutional demand removes metal from the pool available for private lending and trading.

Lease Rate Spikes Signal Tightness, Not Depletion

Market analysts with decades of experience emphasize a critical distinction that often gets lost in dramatic headlines: elevated lease rates indicate temporary tightness in deliverable inventory, not disappearance of the metals themselves.

The LBMA’s research on lease rates explains that spikes typically occur when metal exists but faces temporary obstacles to immediate delivery, wrong location, wrong form, or tied up in uses that prevent immediate lending.

Analysts from Sprott, Kitco, and other reputable sources consistently emphasize this point. The issue is one of timing and transformation, not fundamental scarcity. Metal locked in 1,000-ounce bars in London vaults cannot instantly become one-ounce coins in American dealers’ showcases, but that doesn’t mean the metal doesn’t exist.

Historical Context: Previous Tightness Episodes

The precious metals market has experienced similar episodes before, providing useful perspective on current conditions. In January 1980, silver’s price spike to $50 created refining backlogs of up to six months. Futures contracts traded at massive discounts to spot, and existing coins sold for 70% of melt value because payment was immediate rather than after months of refining delays.

Conversely, during the 2008 financial crisis, available supplies couldn’t satisfy demand when silver dropped from $18 to $10 per ounce. Fabricators extended delivery times to four months after payment, and 90% silver coins traded at premiums as high as 35% above spot because they were immediately available while newly manufactured products were not.

In both cases, the market eventually rebalanced. Refiners caught up with backlogs, premiums normalized, and metal flowed to where demand was strongest. The current tightness, while significant, reflects similar dynamics operating in a market with strong but not unprecedented demand.

An Illustrative Analogy: The Refinery as Factory

To understand why tight markets don’t mean metals are running out, consider an analogy to a different type of supply chain challenge: the toilet paper panic of 2020.

When COVID-19 lockdowns began, consumers rushed to stock up on toilet paper, creating empty shelves in retail stores. Did this mean the world was running out of paper? Of course not. The raw materials, wood pulp and production capacity, remained abundant. The problem was that manufacturers had optimized their supply chains for steady, predictable demand, producing large commercial rolls for offices and schools alongside smaller retail packages for homes.

When demand suddenly shifted entirely to retail packages as people stayed home, manufacturers couldn’t instantly reconfigure production lines. They prioritized large, efficient production runs, and it took weeks to rebalance supply to match the new demand pattern. Toilet paper existed in warehouses and on factory floors, just not in the right form or location for panicked consumers.

Precious metals refiners face remarkably similar dynamics. When prices surge and demand patterns shift rapidly, refiners prioritize large institutional bars that move efficiently through the system. Retail investors seeking one-ounce products experience delays not because silver and gold are disappearing, but because refining capacity is allocated to where it’s most productive.

The analogy isn’t perfect, precious metals markets are far more complex, but it captures the essential truth: supply chain bottlenecks create temporary scarcity of specific products without indicating fundamental depletion of the underlying commodity.

What This Means for Precious Metals Investors

Understanding the true nature of elevated lease rates and market tightness has important implications for investment strategy and decision-making.

Elevated Premiums Are Temporary

Premiums on small coins and bars will likely remain elevated until refiners work through current backlogs and catch up with retail demand. However, these premiums reflect temporary production constraints rather than permanent scarcity. Investors paying substantial premiums today should recognize they’re paying for immediate availability and convenience, not for metal that’s fundamentally scarce.

Historical precedent suggests that when lease rates eventually normalize, which analysts expect as supply chains adjust, premiums on retail products will compress. This creates timing considerations for both buyers and sellers.

Large-Scale Metal Still Exists

Investors should recognize that the physical market may appear squeezed at the retail level while large-scale metal continues to trade actively in wholesale form. The LBMA reports record trading activity and substantial vault holdings throughout 2025’s price surge.

This suggests that the market’s fundamental structure remains sound. The challenge is converting wholesale inventory into retail forms quickly enough to satisfy surging demand, a logistical problem rather than an existential crisis.

Strategic Positioning Considerations

For investors building long-term precious metals positions, current market conditions suggest several strategic considerations:

Diversification Across Product Types: Consider balancing holdings between large institutional-style bars (which trade closer to spot) and smaller retail products (which offer liquidity and divisibility but carry higher premiums). Bullion Trading LLC offers comprehensive options across this spectrum.

Patience With Timing: Investors not facing immediate need might benefit from patience, allowing supply chains to catch up and premiums to normalize. Those accumulating positions can use dollar-cost averaging to smooth out timing risk across the volatility.

Understanding Product Availability: Different product types face different supply dynamics. Government-minted coins from the U.S. Mint, Royal Canadian Mint, or Perth Mint face production constraints different from privately minted rounds or cast bars. Understanding these differences helps set realistic expectations about availability and premiums.

Fundamental Focus: Perhaps most importantly, investors should focus on fundamental drivers rather than short-term supply chain noise. The long-term case for precious metals allocation, portfolio diversification, inflation hedging, currency debasement concerns, geopolitical uncertainty, remains independent of temporary tightness in lease rates or retail product availability.

Looking Ahead: When Will Tightness Ease?

While predicting exact timing is impossible, several factors suggest that current market tightness will eventually moderate:

Refining Capacity Adjustment: Refiners are responding to strong demand by increasing production of retail products. As backlogs clear and production ramps, retail availability will improve.

Price-Driven Supply Response: High prices encourage metal flows from consumers back to refiners. Reports indicate significant selling from jewellery holders in Turkey, Greece, Hong Kong, and other markets as consumers capitalize on record prices. This metal, once refined, will re-enter available inventory.

Demand Moderation: If prices stabilize or decline from current highs, investment demand through ETPs and retail purchases may moderate, reducing pressure on supply chains.

Policy Clarity: Some tightness in silver markets stems from uncertainty about potential U.S. tariffs on critical minerals. Bernard Dahdah of Natixis notes that the Section 232 investigation is scheduled for mid-October release and could provide clarity that allows lease rates to retreat rapidly.

Analysts like Nicky Shiels at MKS Pamp note that silver prices trading more than 30% above their 200-day moving average historically precede corrections, which would relieve pressure on physical markets. However, the structural factors supporting precious metals, central bank buying, industrial demand growth, inflation concerns, suggest any correction might be temporary.

Conclusion: A Crisis of Logistics, Not Supply

The dramatic spike in gold and silver lease rates throughout 2025 tells a story of market tightness, supply chain stress, and temporary bottlenecks, not the catastrophic shortage that sensational headlines might suggest. Physical gold and silver continue to exist in substantial quantities, stored in vaults worldwide and embedded in countless industrial and consumer products.

The challenge facing today’s precious metals market is one of transformation and transportation: converting large wholesale bars into small retail products, moving metal from surplus markets to deficit markets, and processing unprecedented volumes of scrap material being sold by consumers responding to record prices. These are real constraints creating real impacts on availability and pricing, but they’re fundamentally different from the metals “running out.”

For investors, this distinction matters enormously. Panic-driven decisions based on shortage fears risk buying at peak premiums or selling positions prematurely. A clear-eyed understanding of market mechanics, recognizing that elevated lease rates indicate temporary tightness rather than permanent depletion, enables more strategic decision-making.

The precious metals market has weathered similar episodes before and emerged with fundamentals intact. Current tightness will eventually ease as supply chains adjust, refining capacity catches up, and metal flows to where it’s most valued. In the meantime, investors should focus on fundamentals, maintain long-term perspectives, and avoid confusing logistical bottlenecks with existential crisis.

Whether you’re looking to take advantage of current market conditions or build strategic positions for long-term portfolio diversification, Bullion Trading LLC offers comprehensive precious metals solutions backed by market expertise and commitment to investor education. Our extensive inventory of gold, silver, platinum, and palladium products provides options across the spectrum from large institutional bars to popular retail coins.