If you follow gold prices, you have probably come across the term “COMEX” dozens of times. Commentators quote COMEX prices, analysts worry about COMEX inventory levels, and traders reference COMEX open interest when sizing up the gold market. Most of them assume you already know what it is and how it works.

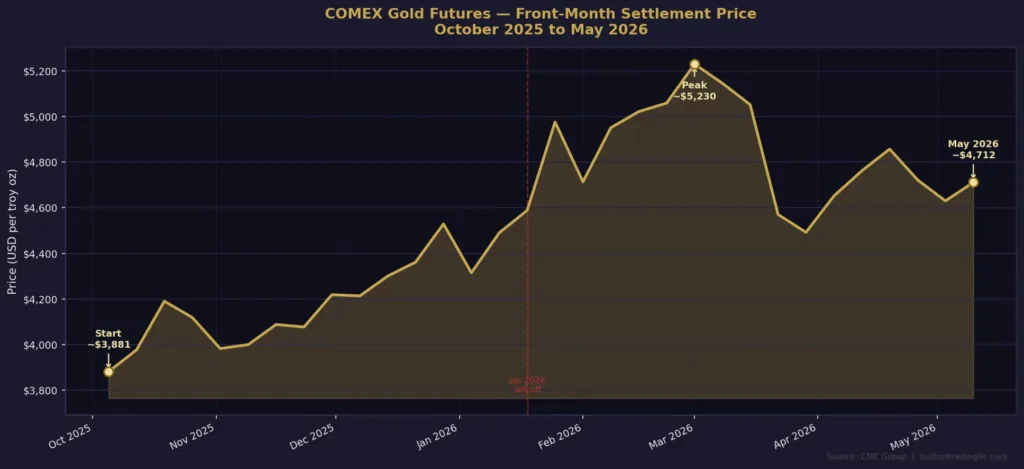

Most people don’t. That’s a real problem, because COMEX gold futures directly set the floor for what you pay for physical coins and bars. With gold trading above $4,700 per ounce as of May 2026, the mechanics behind that number actually matter.

The two markets are connected but not the same, and that difference shows up in the premium you pay every time the basis moves.

What Is COMEX?

COMEX stands for Commodity Exchange. It was founded in New York in 1933 through the merger of four smaller exchanges: the National Metal Exchange, the Rubber Exchange of New York, the National Raw Silk Exchange, and the New York Hide Exchange. In 1994, COMEX merged with the New York Mercantile Exchange (NYMEX), and in 2008, CME Group acquired the combined entity. Investopedia’s overview of COMEX covers this history in detail.

Today, COMEX is a division of CME Group, the world’s largest derivatives marketplace. Gold, silver, copper, and several other metals trade there as standardized contracts on a regulated exchange.

The prices discovered on COMEX serve as the global benchmark for gold. When media outlets report a gold price, they are usually quoting the COMEX front-month futures price or a spot price derived from it. The London Bullion Market Association (LBMA) runs its own LBMA Gold Price benchmark, set twice daily through an electronic auction process, but the two markets stay closely connected through arbitrage. When prices diverge significantly between New York and London, capital and metal flow between markets to close the gap, usually quickly. We covered how those two systems interact in our earlier piece on COMEX and LBMA gold pricing.

What a Gold Futures Contract Actually Is

A futures contract is a legally binding agreement to buy or sell a specific quantity of a commodity at a set price on a specific future date. The textbook definition, but the practical version is simpler: you are making a bet on where gold prices will be at a future date, and the bet is binding.

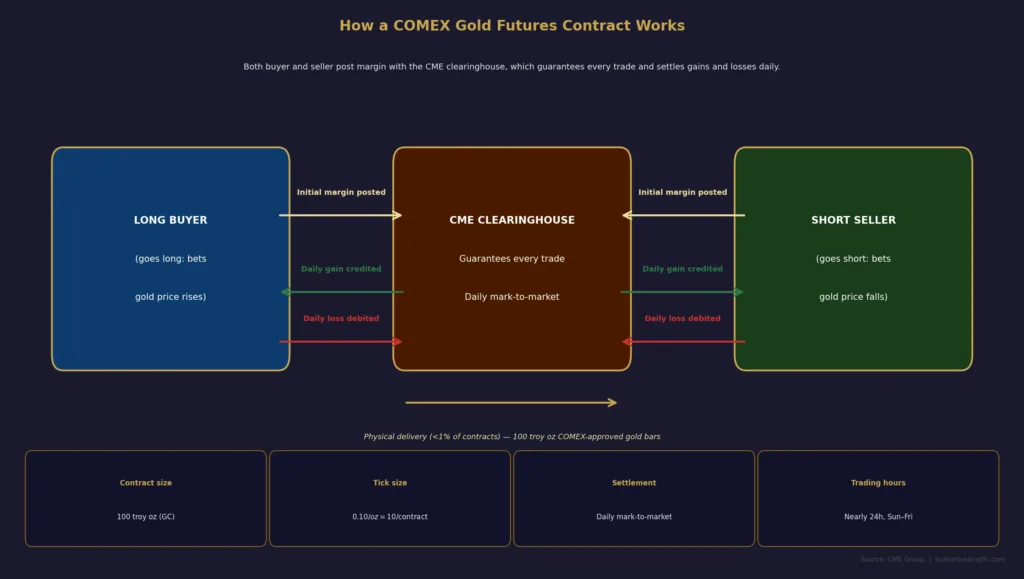

According to the official COMEX gold futures contract specifications, a single standard gold futures contract (ticker symbol: GC) covers 100 troy ounces of gold, quoted in U.S. dollars and cents per troy ounce. With gold at $4,730 per ounce, one contract controls a notional value of $473,000. The minimum price increment is $0.10 per troy ounce, which equals $10 per contract. Every dollar gold moves, your position gains or loses $100.

Contracts are available for delivery in several months throughout the year. The most actively traded months are typically the nearest upcoming delivery months, called “front-month” contracts. As a front-month contract approaches expiration, trading volume shifts to the next scheduled month. The full list of listed contracts is available on the CME Group gold page.

One thing that catches beginners off guard is that gold futures are not traded on a traditional stock exchange like the NYSE. They trade on CME Globex, an electronic platform that is open nearly 24 hours a day, Sunday through Friday, with a 60-minute break each day. That near-continuous access is part of the point: when news breaks in Asia at 3 a.m. New York time, the futures market adjusts immediately. Physical dealers, by contrast, are closed.

Margin, Leverage, and the Daily Settlement

You do not need $473,000 to trade one gold futures contract. That is the entire point of leverage in futures markets.

CME Group sets initial margin requirements (the deposit needed to open a position) and maintenance margin requirements (the minimum balance you must maintain while holding it). These figures change based on volatility, so rather than cite a number that will be outdated, check the current requirements directly on the CME Group gold contract page. The point is that initial margin is a small fraction of the contract’s full notional value. That fraction is the leverage.

That leverage works in both directions. If gold rises $50 per ounce, a long position gains $5,000 on an initial outlay that might be a fraction of that. If gold drops $50 per ounce, the loss is equally real and equally fast. If your account falls below the maintenance margin threshold, you receive a margin call requiring you to add funds or close the position. This is not optional.

What makes futures different from stocks is mark-to-market daily settlement. At the close of each trading session, the exchange calculates the settlement price and credits gains or debits losses directly to each account. There is no “holding through a loss” until things recover, not in the way a stock investor might. The CFTC’s primer on futures trading basics explains how brokers are required to segregate customer funds and adjust accounts daily to current market value. For someone on the right side of a move, this means cash appearing in your account regularly. For someone on the wrong side, it means cash leaving.

Contract Months and the Rolling Process

Each COMEX gold futures contract has a delivery month. As that month approaches, traders who have no intention of receiving or delivering physical gold need to act. Most either close their position outright or “roll” it forward, meaning they sell the expiring contract and simultaneously buy the next active one.

Rolling is routine, but it creates predictable patterns. In the days before expiration, open interest in the front month drops sharply while the next month picks up. Volume can look strange to someone not expecting it. Prices between contract months also differ slightly, a relationship called “contango” when later months trade at a premium to nearer ones, which is the normal state for gold because of financing and storage costs.

Understanding the roll matters practically if you are watching COMEX data to interpret dealer premiums or spot price movements. A sudden widening between two contract months can signal something unusual happening in the physical market, as we described in detail in our analysis of gold and silver lease rates in 2025.

Physical Delivery: Who Actually Gets the Gold

Less than 1% of COMEX gold futures contracts result in physical delivery of gold. That figure comes directly from the exchange, and it matters because it explains the purpose of the market. Most participants, including hedge funds, commodity trading advisers, mining companies, bullion banks, and speculators, close positions before delivery. They use futures to hedge price exposure or speculate on direction. They are not interested in receiving 100-ounce gold bars at a New York depository.

When delivery does occur, the mechanics are specific. A short seller intending to deliver must hold gold in a COMEX-approved depository, evidenced by electronic depository warrants or warehouse receipts. The gold must meet COMEX good delivery standards: a minimum purity of 99.5% for gold bars, produced by COMEX-approved refiners, and conforming to strict weight and dimension requirements.

The process begins on the First Notice Day, which falls several days before the contract’s last trading date. Long position holders who want to take delivery signal their intent. The exchange matches buyers and sellers, and two business days after the short submits its delivery notice, the warrant transfers to the buyer at the settlement price from the notice date.

For a retail investor who accidentally holds a long futures position into the delivery period without intending to take delivery, the situation becomes expensive and complicated to resolve. Tracking your contract’s expiration calendar is not optional.

Micro Gold Futures: A More Accessible Entry Point

CME Group offers Micro Gold futures (ticker: MGC) with a contract size of 10 troy ounces, one-tenth of the standard contract. At $4,730 per ounce, one Micro Gold contract represents a notional value of around $47,300, with proportionally lower margin requirements. For individual investors who want price exposure to gold through the futures market without committing to a full standard contract, these smaller instruments are worth knowing about. Details on the Micro Gold contract are available on the CME Group Micro Gold page.

That said, the mechanics are identical to the standard contract: daily settlement, margin calls, expiration. The numbers are smaller; the risks work exactly the same way. Anyone treating Micro Gold futures as a safe, beginner-friendly substitute for physical metal is in for an unpleasant lesson.

What COMEX Prices Mean for Physical Bullion Buyers

The COMEX futures price is not the retail price on a dealer’s website, but it sets the floor for it. The difference between the two is called the “basis”. Under normal conditions, futures trade at a modest premium to spot, reflecting the cost of financing and storage between now and the delivery date. The spread is usually small and predictable.

When the basis widens or inverts, it signals something unusual. In early 2025, the basis between COMEX gold futures and London spot prices widened dramatically as U.S. demand for physical delivery surged, pushing New York futures to a premium that reached several hundred dollars per ounce above London spot at its peak. The arbitrage that followed pulled large quantities of metal from London vaults into the COMEX delivery system. That kind of basis move flows directly into what dealers charge for physical coins and bars.

There is also the Exchange for Physical (EFP), a mechanism that allows traders to switch between a futures position and a spot physical position. When EFP premiums are wide, it tells you that physical metal in New York is commanding a premium over paper contracts, which is a different signal than the published “spot price” might suggest. The relationship between COMEX and the physical market is not always obvious from headline prices alone.

COMEX Futures vs. Physical Gold: Not the Same Thing

Some commentators frame this as a contest between “paper gold” and “real gold”, with futures portrayed as instruments disconnected from physical metal. That framing has a kernel of truth, but it’s not the whole story.

COMEX futures serve real purposes. Gold miners use them to lock in sale prices for future production. Dealers hedge inventory. Speculators provide the liquidity that makes the market run. That price discovery process feeds into what you pay at a dealer, even if you never open a trading account.

Physical gold doesn’t come with any of those complications. No counterparty, no expiration, no margin calls, no broker standing between you and the metal. For most people, that simplicity is the whole point of owning it.

Understanding COMEX does not make you a futures trader. It makes you a more informed buyer of the physical product, because you understand what sets the price you pay, how that price moves, and why the premium above spot fluctuates in ways that sometimes seem disconnected from the daily headlines.

The Practical Takeaway

Strip away the jargon and a COMEX gold futures contract is not that complicated. One hundred troy ounces, priced in dollars per ounce, settled against the market every day, with less than 1% ever resulting in actual metal changing hands. The market exists to let producers, dealers, and traders shift price risk to whoever wants to take the other side, and it does that at enormous scale: CME Group reports the equivalent of nearly 27 million ounces traded daily, roughly 30 times the volume of the largest gold ETF.

For anyone buying physical gold: COMEX is where the price gets set. The leverage, the margin calls, the rolling, the delivery mechanics all flow into the price of the coins in your safe. Watching COMEX is watching the engine room. Knowing how it works beats wondering why the price moved while you were reading the morning news.