With gold prices establishing new floors above $4,300 per ounce and silver trading near $60, the most common question we receive at our NYC bullion desk has shifted dramatically. Five years ago, investors asked, “Should I buy precious metals?” Today, in the shadow of a $38 trillion national debt and persistent inflation, the question is far more urgent: “How much gold and silver is enough?”.

The answer in late 2025 and 2026 is fundamentally different than it was during the “Great Moderation” of the past few decades. The traditional “5% insurance” allocation, long the standard advice from conservative financial planners, is being stress-tested by a $38 trillion national debt load and a structural shift in global monetary policy. When central banks themselves are accumulating gold at a pace of over 1,000 tonnes annually for three consecutive years, effectively voting against their own fiat currencies, individual investors are right to reassess their own exposure.

This guide provides a comprehensive analysis of portfolio allocation. We will move beyond simple rules of thumb to examine the data behind the “efficient frontier“, the strategic split between gold and silver, and how to determine the right mix for your specific financial goals.

The New Baseline: Why 5% May No Longer Be Enough

For decades, the standard recommendation for precious metals allocation ranged between 5% and 10% of a total investment portfolio. The logic was simple: hold enough to hedge against inflation, but not enough to drag down returns during equity bull markets. This advice worked well in an era of falling interest rates and low inflation.

However, the economic environment of 2025 challenges this minimal allocation. We are currently witnessing the breakdown of the traditional “60/40” portfolio (60% stocks, 40% bonds). Historically, bonds acted as a hedge against stock market volatility; when stocks fell, bonds typically rose. But as we detailed in our analysis of the government debt crisis, this correlation has flipped. In a world of fiscal dominance, where government deficits drive monetary policy, inflation hurts both stocks and bonds simultaneously.

When the two main engines of a portfolio fail to offset each other, the need for a truly non-correlated asset grows. Gold is that asset. It has zero counterparty risk and historically moves independently of financial assets during systemic stress.

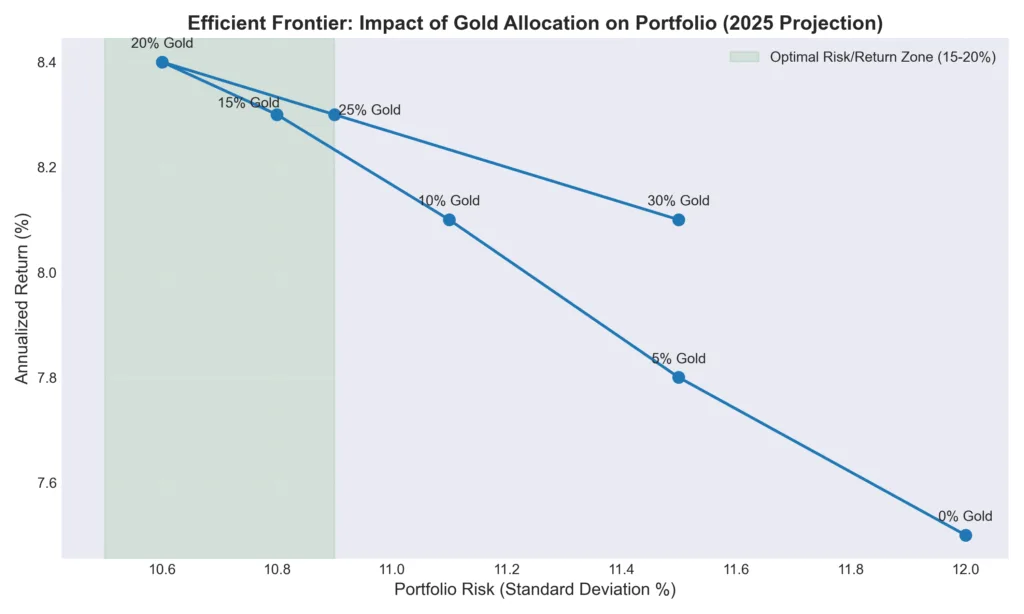

What the Data Says: The Efficient Frontier

There is a concept in modern portfolio theory called the “efficient frontier“, the optimal mix of assets that maximizes returns for a given level of risk. In the past, adding 5% gold to a portfolio was considered sufficient to push a portfolio toward this frontier.

Rigorous analysis of portfolio performance in the 2020s suggests that the “sweet spot” for gold allocation has shifted higher. Data indicates that portfolios with a 15% to 20% allocation to precious metals have historically achieved higher risk-adjusted returns than those with lower allocations, particularly during periods of high inflation or negative real interest rates; where inflation exceeds bond yields.

We categorize allocation strategies into three distinct tiers:

- Conservative Allocation (5-10%): This remains the baseline for “insurance”. It is designed to protect purchasing power against moderate inflation but may not provide significant capital appreciation if the metals market enters a mania phase.

- Balanced Allocation (10-20%): This is the new standard for the prudent investor. It provides meaningful portfolio ballast. If equities correct by 20%, a 15% gold position that appreciates can significantly dampen the overall portfolio drawdown.

- Aggressive Allocation (20-30%+): Typically for investors who view the current monetary system as fundamentally unstable or those using metals as their primary savings vehicle rather than a speculative asset. This level is common among those who prioritize “return of capital” over “return on capital”.

Gold vs. Silver: Finding the Right Split

Once you determine your total precious metals allocation, the next critical decision is the ratio between gold and silver. This is not a one-size-fits-all calculation; it depends entirely on your tolerance for volatility and your investment objectives.

The Case for Gold: Stability and Wealth Preservation

Gold is the bedrock of a precious metals portfolio. It is significantly less volatile than silver and acts as the ultimate store of value. It is a Tier 1 asset for central banks, pension funds, and sovereign wealth funds. These institutions hold gold for liquidity and safety, not necessarily for profit.

For investors prioritizing wealth preservation, lower volatility, and high liquidity, a portfolio weighted heavily toward gold (75% Gold / 25% Silver) is prudent. Gold is your “sleep well at night” asset.

The Case for Silver: Growth and Industrial Leverage

Silver is the high-octane component. While gold is money, silver is both money and an indispensable industrial commodity. As we examined in our report on silver supply tightness, silver is currently in its seventh year of structural deficit. With industrial demand from solar photovoltaics, electric vehicles, and AI-driven electronics consuming nearly 60% of annual supply, silver offers significant upside potential that gold does not.

However, silver is the “devil’s metal” when it comes to volatility. It can drop 10% in a week just as easily as it can rise 10%. A 50/50 split between gold and silver is a common strategy for investors who want to capture silver’s growth potential while maintaining gold’s stability.

The Gold-Silver Ratio as a Guide

Strategic Insight: One of the best tools for determining your split is the Gold-Silver Ratio. With the ratio currently hovering near 70-72, silver remains historically undervalued relative to gold. The modern average is closer to 65, and the geological ratio (how it comes out of the ground) is roughly 8:1.

When the ratio is high (above 80), many strategic investors overweight silver. When it drops low (below 50), they may swap silver for gold. At current levels, the ratio suggests silver may have more room to run in the near term, justifying a slightly higher silver allocation for growth-oriented investors.

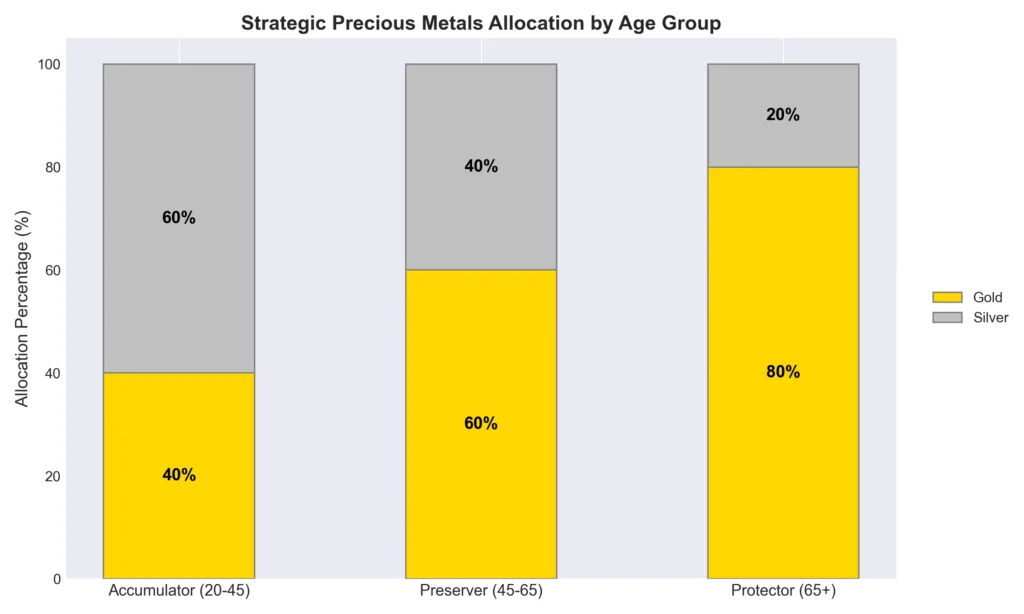

Allocation by Age and Strategy

Your allocation should evolve with your life stage. The old “100 minus your age” rule for stock allocation can be adapted for precious metals, but with a twist: as you age, your need for stability (gold) increases, while your capacity for volatility (silver) decreases.

The Accumulator (Ages 20-45)

Younger investors often have lower capital but a longer time horizon. They are still earning income, which allows them to ride out volatility.

- Strategy: Focus on growth and accumulation.

- Allocation: May lean heavier into silver (40% Gold / 60% Silver) due to its lower absolute price point and higher growth potential.

- Action: Use dollar-cost averaging to build positions. Since gold bars are expensive, consider fractional gold coins or silver rounds to maintain consistent monthly buying. This demographic should view price dips as buying opportunities.

The Preserver (Ages 45-65)

Investors in their peak earning years or approaching retirement. They have accumulated wealth and cannot afford a 50% drawdown right before retirement.

- Strategy: Balance growth with protection.

- Allocation: A balanced mix (60% Gold / 40% Silver). This captures the upside of silver while anchoring the portfolio in gold.

- Action: Focus on moving accumulated wealth into Precious Metals IRAs to maximize tax advantages. This is the stage to convert speculative assets (like high-flying tech stocks) into permanent holdings.

The Protector (Ages 65+)

Retirees focused on income, liquidity, and estate planning. Volatility is the enemy here.

- Strategy: Maximum stability and liquidity.

- Allocation: Heavy gold weighting (80% Gold / 20% Silver). Gold is far less bulky to store and easier to liquidate in large amounts than silver.

- Action: Prioritize highly liquid sovereign coins like American Eagles or Gold Buffaloes. These are recognizable worldwide and easy for heirs to handle. Avoid numismatics or complex collectibles that require expert knowledge to sell.

Savings vs. Investment: The “Insurance” Perspective

A critical distinction often missed is the difference between investing in metals and using metals as savings. This mental shift is crucial for understanding allocation.

If you view gold and silver purely as an investment to sell for a profit in six months, you are speculating. However, if you view them as savings, a tier of liquidity outside the banking system, the allocation logic changes completely. You don’t “invest” in a savings account; you park money there for safety. Gold is simply a savings account that cannot be debased by inflation.

We recommend a “liquidity tier” approach to determine how much to hold:

- Tier 1 (Fiat Cash): Keep 3-6 months of living expenses in fiat currency for immediate bills, rent, and minor emergencies. This is for utility, not wealth preservation.

- Tier 2 (Hard Savings/Insurance): Once your cash buffer is full, excess savings can be allocated to physical gold and silver. This portion is not “traded”; it is held as a long-term store of purchasing power. This is your “personal central bank” reserve.

- Tier 3 (Investment): Equities, real estate, and other risk assets. These are for growth.

In a world where the purchasing power of the dollar is eroding at a structural rate, holding “too much” cash in Tier 1 is a guaranteed loss. Moving Tier 2 savings into gold is not “risking” money; it is protecting it from the silent theft of inflation.

Paper vs. Physical: The Allocation Trap

When calculating your allocation, a common mistake is treating “paper gold” (ETFs, futures contracts, mining stocks) as identical to physical metal. They are not.

Paper Gold is a financial instrument. It exposes you to counterparty risk, the risk that the other party (the bank, the fund manager, the exchange) cannot fulfill their obligation. In a liquidity crisis, paper claims on gold can be settled in cash rather than metal.

Physical Gold is a tangible asset. It has zero counterparty risk. If you hold it, you own it. There is no board of directors, no management fee, and no bankruptcy court that can take it from you.

Recommendation: For your core “insurance” allocation (the 10-20% discussed above), we strongly recommend physical metal in your possession or in allocated, segregated storage. Mining stocks and ETFs can be used for speculative plays (Tier 3), but they should not count toward your Tier 2 safety allocation.

Common Allocation Mistakes to Avoid

Even seasoned investors can stumble when building a precious metals portfolio. Here are three common pitfalls to avoid:

1. Counting Jewelry as Bullion

While high-karat jewelry (22k or 24k) has value, it is not an efficient investment vehicle due to high fabrication costs and lower liquidity compared to coins and bars. Do not count your wedding ring or gold chains toward your 15% portfolio allocation.

2. Ignoring the Exit Strategy

Don’t buy 100 ounces of silver if you might need to pay a $2,000 emergency bill next week. Silver is bulky and can have wider buy/sell spreads. Ensure you have enough fractional gold or smaller silver denominations to liquidate small amounts if necessary, rather than having to sell a single large 1-kilo gold bar.

3. “All or Nothing” Thinking

Some investors get paralyzed waiting for the perfect price to go “all in”. Others sell everything the moment prices dip. The most successful investors use Dollar Cost Averaging (DCA). By buying a fixed dollar amount every month regardless of price, you smooth out volatility and build a substantial position over time without the stress of market timing.

Conclusion: Personalizing Your Number

There is no single magic number, but the data is clear: the risks of under-allocation are significantly higher than the risks of over-allocation.

With the U.S. debt trajectory accelerating and central banks buying gold at record rates, a 15% allocation to precious metals represents a prudent baseline for the modern investor. This is no longer a fringe idea; it is a rational response to a changing monetary order.

Whether you choose to lean into silver for its industrial upside or anchor yourself in gold for its monetary stability, the key is to move from abstract theory to physical possession. In an era of digital illusions and paper promises, gold remains the only financial asset that is not someone else’s liability.

Whether you are starting with a single ounce of silver or rebalancing a seven-figure portfolio, Bullion Trading LLC offers the inventory and expertise to help you reach your allocation goals. Visit us online or at our NYC location to discuss your strategy.