When the world’s largest banks begin issuing blockchain-based tokens representing dollar deposits, it signals more than just technological innovation, it reveals fundamental weaknesses in the existing financial system. JP Morgan’s JPM Coin deposit token, now operating through their Kinexys platform, represents a significant step toward digitizing traditional banking. However, this development simultaneously highlights why physical gold remains irreplaceable as a wealth preservation asset in an increasingly digitized financial landscape.

Understanding the distinction between tokenized banking products and physical precious metals has never been more critical for investors navigating 2025’s complex market environment. As gold reaches new all-time highs above $4,000 per ounce and banks accelerate their blockchain initiatives, the contrast between centralized digital tokens and decentralized physical assets grows increasingly apparent.

What Is JPM Coin and Why Does It Matter?

JP Morgan’s JPM Coin functions as what the bank calls a “deposit token”, a blockchain-based representation of U.S. dollar deposits held at JPMorgan Chase Bank. Unlike cryptocurrencies or stablecoins, JPM Coin represents a direct liability of the bank itself. According to JPMorgan’s official documentation, the token enables near-real-time payments 24/7 among approved institutional clients.

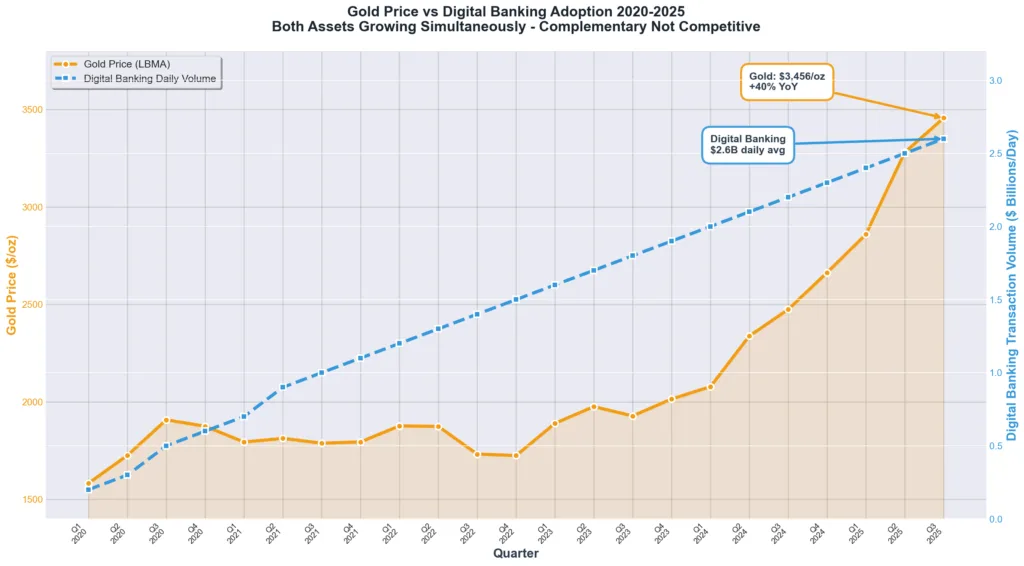

The system has processed over $1.5 trillion in transaction volume since inception, with average daily volumes exceeding $2 billion. These impressive figures demonstrate genuine institutional adoption of blockchain technology for traditional banking functions.

The Architecture of Digital Banking Control

JPM Coin operates on JPMorgan’s proprietary Kinexys platform (formerly called Onyx), a permissioned blockchain network. This architecture reveals the fundamental nature of the system: it moves money faster, operates around the clock, and leverages blockchain technology, but it remains entirely controlled by the issuing bank.

When you hold JPM Coin, you don’t hold currency. You hold a tokenized claim on deposits at JP Morgan. The distinction matters profoundly: if the bank faces difficulties, your digital token faces the same counterparty risk as traditional deposits, despite the technological sophistication of its delivery mechanism.

This represents what many observers call “centralized digitization”, making the existing system faster and more efficient while retaining all the structural dependencies and systemic risks that characterize traditional banking.

The Tokenization Trend: Banks Modernizing Legacy Infrastructure

JPM Coin represents just one example of a broader trend toward tokenizing traditional financial assets. Major financial institutions globally are exploring similar initiatives, recognizing that blockchain technology offers significant operational efficiencies for clearing, settlement, and cross-border payments.

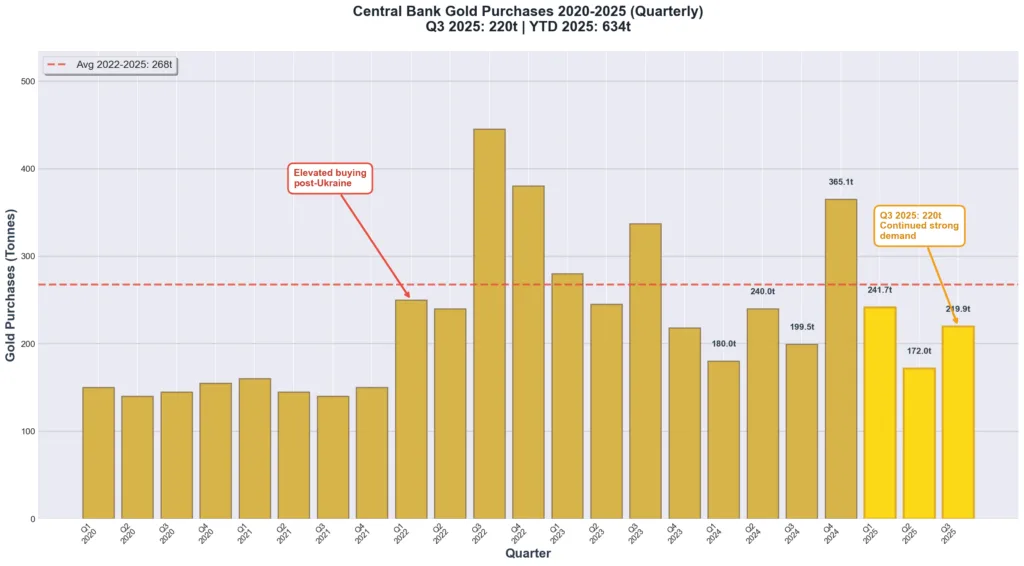

World Gold Council data from Q3 2025 shows that while financial innovation accelerates, gold demand simultaneously reached record levels, 1,313 tonnes in Q3 alone, valued at $146 billion. This parallel trend suggests investors view digital banking innovation and physical gold ownership as complementary rather than competitive strategies.

The Paradox of Digital Gold Tokens

Attempts to tokenize gold itself reveal the limitations inherent in digitizing physical assets. Paxos Gold (PAXG), one of the most established tokenized gold products, offers each token backed by one fine troy ounce of LBMA-certified gold stored in London vaults. The product works well for specific use cases requiring quick settlement or fractional ownership.

However, tokenized gold fundamentally transforms the nature of gold ownership. You no longer hold physical metal, you hold a digital claim to metal held by a custodian. This introduces several layers of dependency:

- Custodial risk: Your claim depends on the custodian maintaining proper storage and records

- Platform risk: The blockchain platform must remain operational and accessible

- Redemption risk: Converting tokens back to physical metal involves procedures, fees, and potential delays

- Regulatory risk: Changes in regulations could affect your ability to access or transfer tokens

As the saying goes among precious metals advocates: “If you don’t hold it, you don’t own it.” Tokenization, regardless of how sophisticated, creates a separation between the holder and the physical asset.

Why Physical Gold Offers Unique Advantages

The case for physical gold ownership in 2025 rests not on rejecting digital innovation, but on recognizing the distinct value propositions of different asset classes. Physical gold offers characteristics that tokenized or digital alternatives fundamentally cannot replicate.

Final Settlement Outside the System

Physical gold held in your possession or in allocated storage under your control represents final settlement. There’s no counterparty standing between you and your asset. No bank needs to remain solvent, no blockchain needs to operate, no custodian needs to maintain records. The metal simply exists, holding value regardless of institutional continuity.

This quality becomes particularly valuable during periods of systemic stress. History repeatedly demonstrates that when financial systems face severe pressure, claims and contracts can fail while physical assets maintain their status. Recent analysis of gold’s behavior during liquidity crises shows that physical metal acts as a systemic insurance policy precisely when digital systems become most vulnerable.

24/7 Accessibility Without Intermediaries

While JPM Coin offers 24/7 operation, it requires the bank’s systems to remain functional and your account to remain in good standing. Physical gold requires no such dependencies. It remains accessible regardless of:

- Banking hours or system maintenance

- Account freezes or restrictions

- Payment network disruptions

- Geopolitical restrictions on cross-border transfers

- Changes in terms of service or fee structures

The 2025 household debt crisis, with U.S. household debt reaching $18.59 trillion, illustrates why asset ownership independent of the credit system matters. When leverage reaches extreme levels throughout the economy, assets that don’t depend on institutional solvency or credit availability offer unique protection.

Inflation and Currency Debasement Hedge

Digital dollar tokens, whether issued by JP Morgan or other institutions, remain denominated in and redeemable for U.S. dollars. They may move faster and settle more efficiently, but they offer zero protection against dollar devaluation or monetary expansion.

Gold, conversely, maintains purchasing power over long time horizons precisely because it exists outside the monetary system. With central banks purchasing 634 tonnes year-to-date in 2025 and the gold price reaching record levels above $4,000 per ounce, institutional recognition of gold’s monetary role continues strengthening.

Privacy and Financial Autonomy

Blockchain-based banking tokens, operating on permissioned networks, create perfect transaction records. Every movement of JPM Coin gets recorded, tracked, and potentially monitored. For legitimate commercial purposes, this transparency offers benefits. However, it also represents total surveillance of financial activity.

Physical gold transactions, particularly in allocated storage or direct possession, offer far greater privacy. While regulatory requirements apply to dealers and large transactions, physical metal doesn’t create permanent, traceable records of every subsequent transfer or movement.

As programmable currencies and central bank digital currencies (CBDCs) advance globally, the option to hold wealth in non-programmable, non-surveillable forms may prove increasingly valuable.

The Irony: Banks Building Digital Rails While Holding Physical Metal

Perhaps the most revealing aspect of bank tokenization initiatives is what financial institutions do with their own balance sheets. While JP Morgan pioneers digital dollar tokens for client use, major banks maintain significant involvement in physical precious metals markets.

JPMorgan serves as an approved vault operator for COMEX gold and silver, storing thousands of tonnes of physical metal backing futures contracts. This dual strategy, building digital infrastructure while maintaining large physical precious metals positions, suggests sophisticated financial institutions recognize the enduring value of physical assets even as they digitize currency.

The AI job displacement trends affecting 2025 labor markets add another dimension to this analysis. As technological change accelerates and economic uncertainty increases, the appeal of assets outside the digital ecosystem strengthens rather than weakens.

Central Banks Choose Physical Over Digital

Perhaps the most compelling evidence for physical gold’s superiority comes from central bank behavior. These institutions have access to every form of financial technology, unlimited counterparties, and the ability to create any synthetic exposure they desire. Yet they overwhelmingly choose physical gold.

According to World Gold Council Q3 2025 data, central banks purchased 220 tonnes in Q3 alone, maintaining elevated buying for the fourth consecutive quarter. Year-to-date purchases of 634 tonnes continue a multi-year trend of aggressive accumulation.

Central banks could hold gold exposure through derivatives, ETFs, or future tokenized products. They choose physical metal because it offers characteristics that synthetic exposure cannot provide:

- No counterparty risk

- Final settlement asset in international reserves

- Proven store of value across regimes and crises

- Liquidity independent of financial system operation

- Political neutrality and universal acceptance

When the institutions that manage national reserves consistently choose physical metal over digital alternatives, it sends a powerful message about relative value propositions.

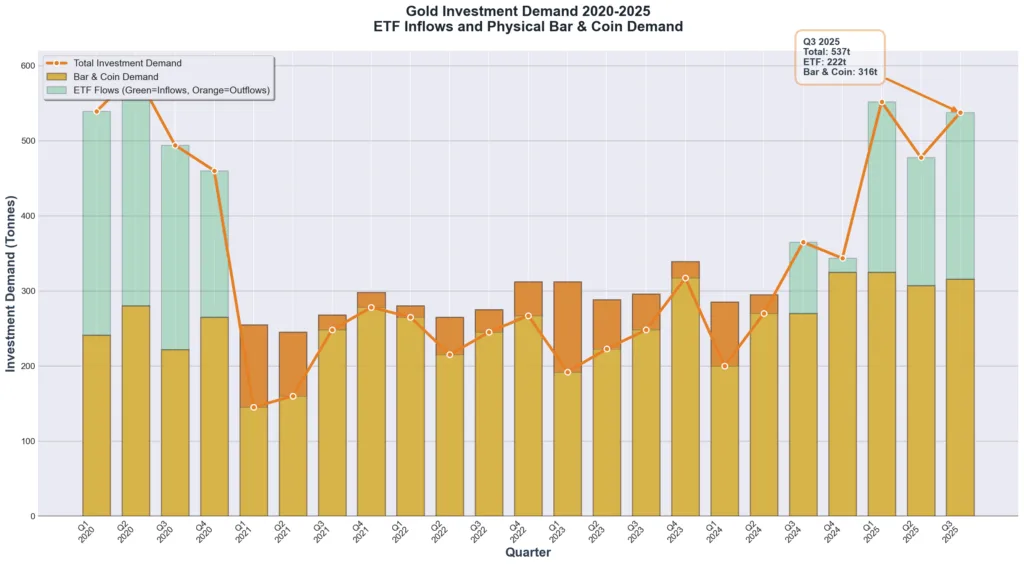

Investment Demand Drives Gold to New Records

While banks build digital infrastructure, investors have pushed gold to unprecedented price levels. The LBMA gold price averaged $3,456.54 per ounce in Q3 2025, up 40% year-over-year, and has since exceeded $4,000 per ounce in November 2025.

This price appreciation occurred alongside massive investment flows. Gold-backed ETFs saw inflows of 222 tonnes in Q3 2025 alone, while bar and coin demand remained above 300 tonnes for the fourth consecutive quarter at 316 tonnes.

The structural bull market in gold reflects multiple converging factors that digital tokens don’t address:

- Persistent inflation concerns despite central bank tightening

- Geopolitical tensions and de-dollarization trends

- Fiscal unsustainability and sovereign debt concerns

- Banking system fragility revealed by regional bank failures

- Currency debasement through continued monetary expansion

Understanding Gold’s Job in Your Portfolio

The investment case for physical gold doesn’t rest on competing with or replacing digital banking innovations. Rather, as explored in our analysis of gold’s job in investment strategy, gold serves distinct portfolio functions:

- Systemic insurance: Protection when financial systems face stress

- Currency debasement hedge: Maintaining purchasing power across monetary regimes

- Diversification: Low correlation with traditional financial assets

- Long-term wealth preservation: Maintaining value across generations

Digital banking tokens may execute these jobs better for daily transactions or short-term settlement. They cannot replicate gold’s performance when the financial system itself comes under pressure.

Tokenization Can’t Improve Perfection

There’s a fundamental philosophical point underlying the physical gold versus tokenized asset debate: some things don’t improve through digitization because their value lies precisely in existing outside digital systems.

Gold has served as money and wealth storage for over 5,000 years without requiring upgrades, protocols, or technical infrastructure. This is a feature, not a bug. Attempts to “improve” gold through tokenization add efficiency for certain use cases while eliminating the core characteristics that make gold valuable in the first place.

It’s similar to claiming that scanning the Mona Lisa and creating an NFT “improves” the painting. You may have created a more tradeable, more divisible digital asset, but you haven’t improved the original, you’ve created something different that serves different purposes.

The Question of Use Case

This analysis doesn’t suggest tokenized assets or digital banking innovations lack value. They solve real problems around payment efficiency, settlement speed, and operational costs. For international corporate treasury management or high-frequency trading operations, JPM Coin-type solutions offer genuine advantages.

However, for the distinct use case of long-term wealth preservation, portfolio insurance, and protection against systemic risk, physical gold offers characteristics that digital alternatives cannot replicate. The two asset classes serve different purposes and aren’t directly competitive.

Looking Ahead: Digital Innovation and Physical Assets

The future likely includes both accelerating digital innovation in financial services and sustained demand for physical precious metals. These trends complement rather than compete with each other.

As central bank digital currencies (CBDCs) advance, programmable money becomes technically feasible, and financial surveillance capabilities expand, the attributes of physical gold, privacy, autonomy, final settlement outside the system, may become more valuable rather than less.

Similarly, as AI-driven economic disruption creates uncertainty about future employment patterns and income distribution, assets that maintain value regardless of credit system stability offer unique protection.

Conclusion: Different Tools for Different Jobs

JP Morgan’s success with JPM Coin demonstrates that blockchain technology offers genuine value for improving traditional banking operations. The platform’s $1.5 trillion in transaction volume proves that institutional clients benefit from faster settlement, 24/7 operation, and improved efficiency.

However, this technological achievement doesn’t diminish, and may actually strengthen, the case for physical gold ownership. Digital banking tokens, regardless of their sophistication, remain claims on fiat currency maintained by centralized institutions. They make the existing system more efficient without addressing fundamental concerns about currency debasement, counterparty risk, or systemic fragility.

Physical gold offers a fundamentally different value proposition: final settlement, no counterparty risk, independence from institutional continuity, and 5,000 years of proven wealth preservation. These characteristics become more valuable, not less, as financial systems grow more complex, interconnected, and digitally dependent.

The record gold demand in Q3 2025, with 1,313 tonnes valued at $146 billion, suggests investors globally recognize this distinction. Central banks continue accumulating physical metal despite having access to every possible form of synthetic exposure.

For investors building resilient portfolios in 2025’s uncertain environment, the answer isn’t choosing between digital innovation and physical assets, it’s understanding that different tools serve different purposes. Digital banking solutions may optimize operational efficiency, but physical gold provides insurance against systemic risk that tokenized alternatives simply cannot replicate.

Whether you’re looking to establish initial precious metals positions or expand existing holdings, Bullion Trading LLC offers comprehensive solutions across the spectrum from small retail coins to large institutional bars. Our extensive inventory of gold, silver, platinum, and palladium products, combined with market expertise and commitment to investor education, helps you navigate the complex intersection of traditional finance, digital innovation, and time-tested wealth preservation strategies.