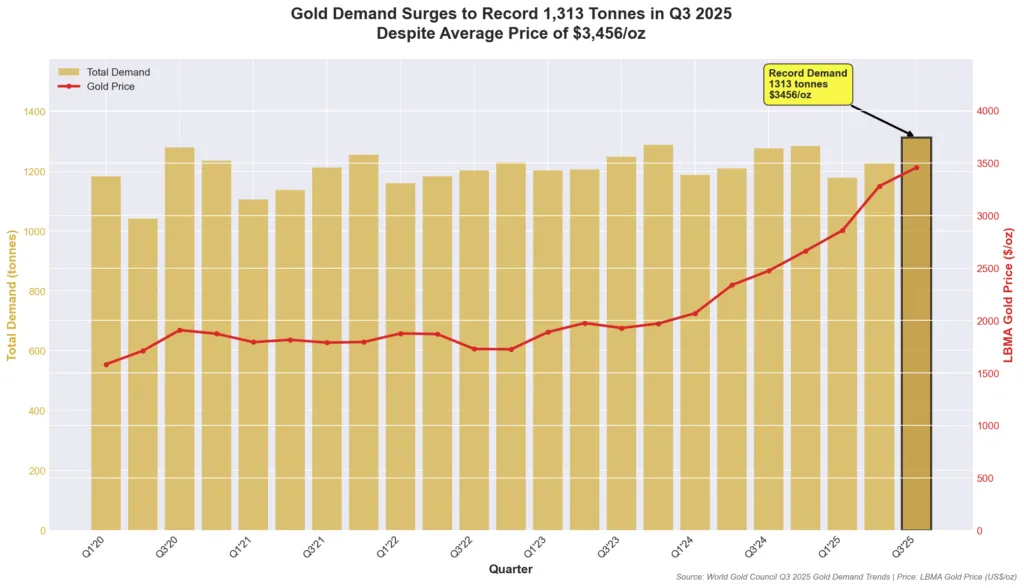

When gold reached record highs above $4,000 per ounce in late 2025, most retail investors hesitated. High prices typically deter buyers, a basic principle of market psychology. Yet total gold demand didn’t collapse, it surged. According to the World Gold Council’s Q3 2025 Gold Demand Trends report, total quarterly demand jumped to 1,313 tonnes in Q3 2025, up 3% year-over-year and marking the highest quarterly total in their entire data series.

This paradox reveals something profound about the current gold market: while the public hesitates at high prices, institutions and central banks, the entities that understand monetary dynamics best, are accumulating gold at an unprecedented pace. The divergence between retail sentiment and institutional behavior tells us more about gold’s true value than any price chart.

The Demand Surge: Record Quarterly Total Despite High Prices

Q3 2025 delivered remarkable numbers that challenge conventional wisdom about price sensitivity in gold markets. Total gold demand reached 1,313 tonnes, representing the highest quarterly demand figure the World Gold Council has recorded since they began comprehensive tracking.

The price environment makes this achievement extraordinary. Gold averaged $3,456.54 per ounce during Q3, up 40% year-over-year and 5% quarter-over-quarter. The LBMA gold price hit 13 new all-time highs during the quarter. Yet demand didn’t collapse, it accelerated. The value measure of demand jumped 44% year-over-year to a record $146 billion in Q3 alone.

Central Banks: The Strategic Accumulators

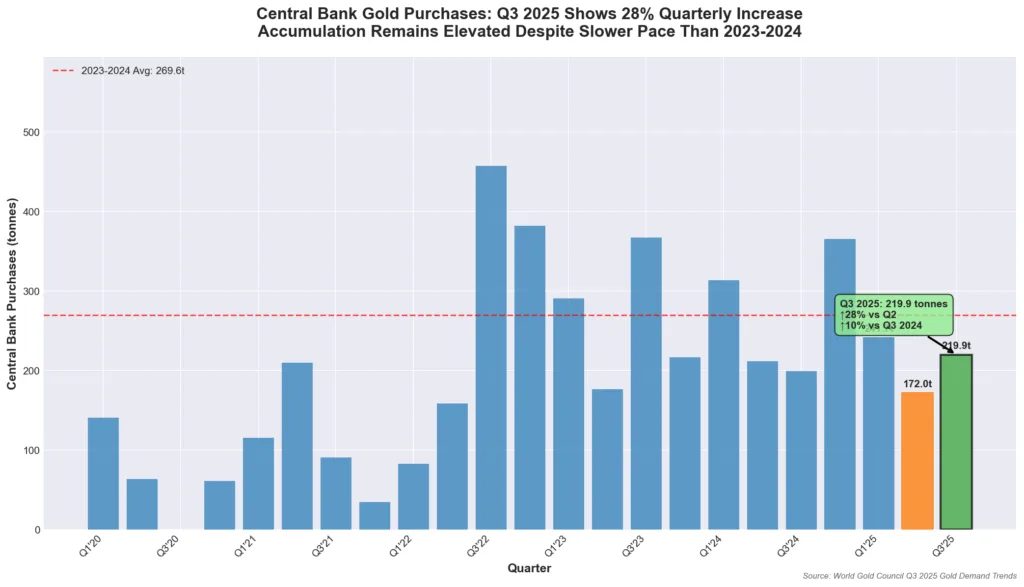

Central bank gold purchases represent perhaps the most significant structural driver in today’s gold market. These aren’t speculators chasing momentum, these are sovereign institutions with decades-long investment horizons making strategic decisions to diversify reserves away from dollar-heavy portfolios.

Q3 2025 saw central banks purchase 219.9 tonnes of gold, up 28% from Q2’s 172 tonnes and 10% higher than Q3 2024’s 199.5 tonnes. Year-to-date through Q3 2025, central banks accumulated 634 tonnes. While this represents a slower pace than 2023-2024’s record-breaking years (which saw over 1,000 tonnes purchased annually), it remains dramatically elevated compared to historical norms.

According to the World Gold Council’s Central Bank Gold Reserves survey, emerging market central banks cite currency diversification, inflation concerns, and geopolitical risk as primary motivations for gold accumulation.

This buying creates permanent demand that doesn’t reverse with price corrections. Unlike ETF flows that can swing dramatically based on sentiment, central bank gold enters vaults where it typically remains for decades. Each quarter of sustained official sector buying represents metal permanently removed from the liquid market.

Investors: Dramatic Acceleration in Physical and ETF Demand

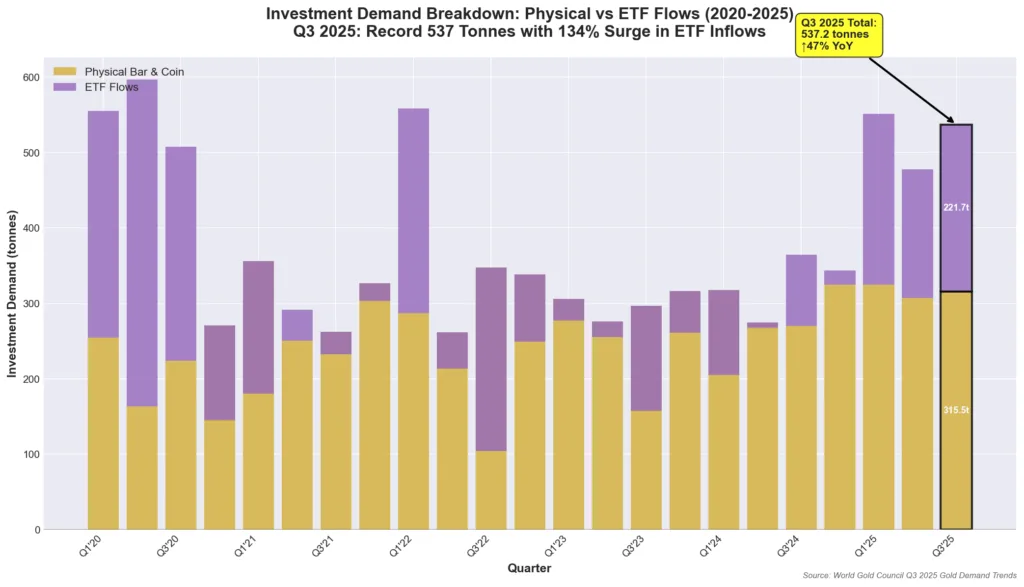

Investment demand delivered the most dramatic surge in Q3 2025. Total investment demand reached 537.2 tonnes, up 47% year-over-year from Q3 2024’s 364.8 tonnes and 13% higher than Q2 2025’s 477.5 tonnes.

Physical Bar and Coin Demand

Physical bar and coin demand totaled 315.5 tonnes in Q3, up 17% year-over-year. This marks the fourth consecutive quarter with bar and coin demand exceeding 300 tonnes, a threshold that historically indicates robust retail and high-net-worth individual interest.

The breakdown reveals strong across-the-board demand:

- Gold bars: 237.1 tonnes, up 19% year-over-year

- Official coins: 31.7 tonnes, flat year-over-year

- Medals and imitation coins: 46.7 tonnes, up 17% year-over-year

The consistency of physical demand above 300 tonnes per quarter throughout 2025 suggests sophisticated investors maintain conviction despite elevated prices. As detailed in our analysis of gold and silver lease rates, the physical market experienced periodic tightness in 2025 as strong demand tested refining capacity.

ETF Inflows: The Institutional Signal

Gold-backed exchange-traded products experienced dramatic inflows of 221.7 tonnes in Q3 2025, representing a stunning 134% increase from Q3 2024’s 94.7 tonnes. This marks a complete reversal from 2022-2023 when ETFs experienced persistent outflows.

ETF investors typically represent institutional players, pension funds, wealth managers, endowments, making tactical allocation decisions. When these sophisticated investors reverse years of outflows and begin accumulating aggressively at record prices, it signals fundamental reassessment of gold’s role in portfolio construction.

Year-to-date through Q3 2025, gold ETFs attracted 619 tonnes of inflows. The record ETF inflows in September 2025 totaling $17 billion represented the largest monthly inflow ever recorded.

Who Stopped Buying? Jewelry Consumers Feel the Price Pressure

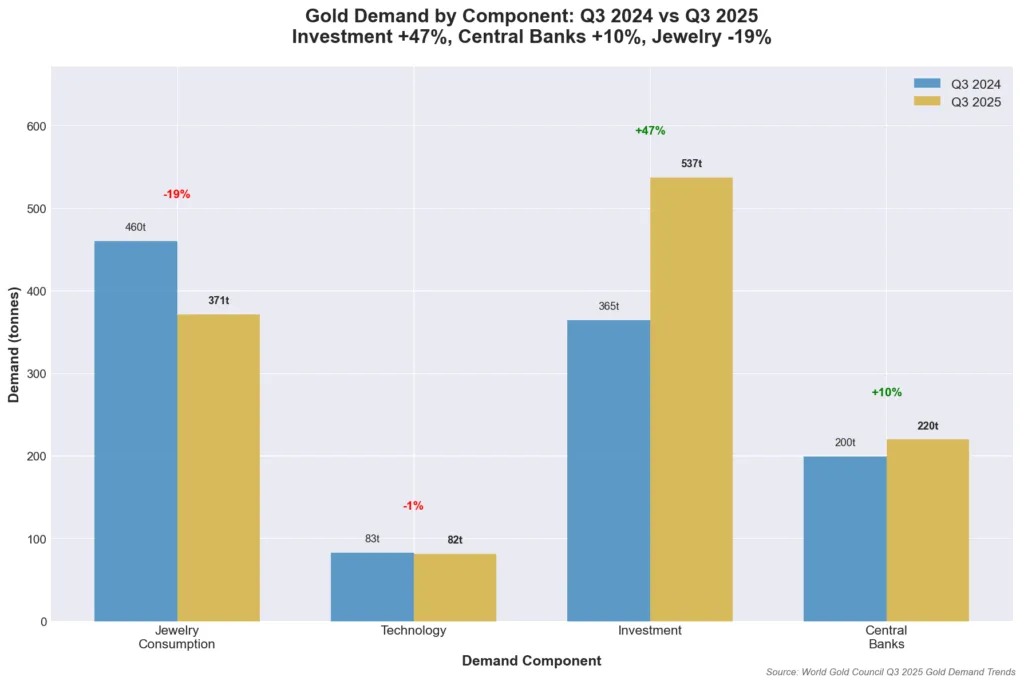

While investment and central bank demand surged, jewelry fabrication declined significantly. Global jewelry fabrication fell to 419.2 tonnes, down 23% year-over-year. Jewelry consumption specifically dropped 19% to 371.3 tonnes from 460 tonnes in Q3 2024.

This represents the sixth consecutive quarter of double-digit year-over-year declines in jewelry demand. High prices, while failing to deter institutional and sovereign buyers, have significantly impacted retail jewelry consumers, particularly in price-sensitive markets like India and China.

The divergence is logical. A central bank diversifying $50 billion in reserves cares about long-term currency risk, not whether gold trades at $3,400 or $3,500 per ounce. A bride purchasing a wedding ring faces direct price sensitivity, every $100 increase translates to meaningfully more expensive jewelry.

This jewelry weakness reinforces the broader narrative: price-sensitive demand collapsed while price-insensitive demand surged, exactly what you’d expect when sophisticated buyers view gold as monetary protection rather than discretionary consumption.

Why They’re Buying: The Fundamental Drivers

Understanding who’s buying is incomplete without understanding why. The motivations driving record central bank and institutional accumulation reflect deep structural concerns:

Persistent Inflation and Real Yield Compression

Despite aggressive rate hiking cycles, inflation has proven remarkably sticky. U.S. CPI inflation continues running above the Federal Reserve’s 2% target. Real yields, the return on bonds after inflation, remain compressed. As detailed in our analysis of Federal Reserve policy and gold prices, the Fed began cutting rates in September 2025 while inflation persisted above target, creating negative or near-zero real yields across much of the yield curve.

Fiscal Deterioration and Debt Dynamics

The U.S. national debt exceeds $38 trillion as of November 2025, representing approximately 125% of GDP. Annual interest payments now exceed $1.2 trillion, consuming roughly 17% of federal revenue. These dynamics create a “debt trap” where high debt levels require low interest rates to remain serviceable, but low rates risk accelerating inflation. Either outcome supports gold appreciation.

Geopolitical Fragmentation and De-Dollarization

The international monetary system is experiencing its most significant transformation since the 1970s. Central banks, particularly in emerging markets, are diversifying reserves. Gold offers a neutral reserve asset that doesn’t carry counterparty risk or political exposure. When a central bank holds U.S. Treasuries, those assets can be frozen by U.S. government action. Physical gold stored in domestic vaults cannot.

Banking System Concerns

The March 2023 banking crisis demonstrated how quickly confidence can evaporate. Physical gold carries zero counterparty risk, it maintains value independent of any institution’s solvency.

Supply Side: Why Production Can’t Keep Pace

While demand surged, supply growth remained modest. Total gold supply reached 1,313 tonnes, up just 3% year-over-year. Mine production reached 976.6 tonnes in Q3 2025, up only 2% despite record prices above $4,000 per ounce.

Several structural factors constrain production growth:

- Declining ore grades: Average gold ore grades have declined significantly, meaning miners must process more ore to extract the same amount of gold

- Extended development timelines: From discovery to production, new gold mines require 7-15 years due to permitting and environmental reviews

- Capital intensity: Lower ore grades and deeper deposits require larger, more expensive mining operations

- Geopolitical risk: Many high-potential deposits exist in unstable regions, deterring investment

These constraints mean supply cannot rapidly respond to demand surges. Strategic buyers are absorbing more than 60% of global mine production, and they’re doing so at record prices without hesitation.

Market Implications: What This Means for Investors

The Q3 2025 demand data carries significant implications for investors evaluating precious metals exposure:

1. The Public Is Wrong at Market Inflection Points

Retail jewelry demand collapsed at record prices while institutional accumulation accelerated. As detailed in our analysis of why investors buy gold, when sophisticated institutions with multi-decade time horizons buy aggressively despite record prices, dismissing gold because “it’s expensive” reflects retail investor thinking, not institutional strategy.

2. Strategic Accumulation Provides Price Support

Price-insensitive demand from central banks and institutional investors creates durable support during corrections. The October 2025 correction found support quickly precisely because strategic buyers viewed weakness as opportunity rather than trend change.

3. Supply Constraints Support Multi-Year Appreciation

With mine production growing just 2% annually despite record prices, and strategic buyers absorbing over 60% of annual production, the supply-demand imbalance supports sustained price appreciation over multi-year timeframes.

4. Diversification Rationale Strengthens

Gold’s low correlation with traditional financial assets becomes increasingly valuable as stock market valuations reach extremes and bond markets face persistent inflation concerns.

Strategic Considerations for Portfolio Construction

For investors evaluating precious metals allocation in light of Q3 2025 demand trends:

Physical Gold Provides Pure Exposure: Physical gold in coins and bars offers direct ownership with zero counterparty risk. Popular sovereign coins like American Gold Eagles provide high liquidity, while larger bars offer lower premiums for substantial positions.

Gold ETFs Offer Liquidity: Gold-backed ETFs provide liquid exposure suitable for tactical allocations. The record Q3 2025 ETF inflows demonstrate institutional preference for this vehicle.

Precious Metals IRAs: IRS-approved Precious Metals IRAs allow holding physical gold in tax-advantaged retirement accounts, combining benefits of physical ownership with retirement account tax treatment.

Dollar-Cost Averaging: Making regular purchases regardless of price reduces timing risk and ensures exposure to gold’s long-term appreciation potential while minimizing psychological stress of market timing.

Conclusion: Following the Smart Money

Q3 2025 gold demand data tells a clear story: while price-sensitive retail consumers hesitated, price-insensitive institutional buyers, central banks, pension funds, sovereign wealth funds, accumulated gold at record pace. Total demand reached the highest quarterly level in the World Gold Council’s data series despite gold trading near record prices.

Central banks bought 220 tonnes, up 28% quarter-over-quarter. Investment demand surged 47% year-over-year to 537 tonnes, driven by both physical purchases and dramatic ETF inflows of 222 tonnes. Meanwhile, jewelry consumption declined 19% as high prices impacted discretionary buyers.

This divergence reveals fundamental market truths. The entities with the longest time horizons, deepest analytical resources, and best understanding of monetary dynamics are buying aggressively at record prices. They’re not speculating on short-term moves, they’re responding to structural concerns about currency stability, inflation persistence, fiscal deterioration, and geopolitical fragmentation.

When central banks accumulate gold despite elevated prices, they’re sending a signal about the future of fiat currency systems. When institutional investors reverse years of outflows and begin adding gold exposure aggressively, they’re reassessing portfolio construction in light of unprecedented monetary and fiscal conditions.

The retail investor facing record prices and asking “isn’t gold expensive?” reveals a fundamental misunderstanding. For entities buying gold as monetary insurance against systemic risks, questions about “expensive” versus “cheap” miss the point. The question is whether the conditions warranting gold ownership exist. Q3 2025 demand data suggests sophisticated buyers overwhelmingly answer “yes.”

Whether you’re establishing initial precious metals positions or expanding existing holdings, Bullion Trading LLC offers comprehensive solutions backed by market expertise and commitment to investor education. From popular gold coins to large institutional bars, our extensive inventory serves every investment strategy.