Gold crossed $5,405 per ounce in January 2026 before pulling back, and the narrative in financial media focused almost entirely on retail investors, ETF inflows, and central bank buying. Mostly left out of that conversation: the role of sovereign wealth funds, the massive state-owned investment vehicles that together manage more than $12 trillion in assets worldwide. These are not speculative buyers. When they move, they move slowly and deliberately, and the data from the past two years suggests they have been moving toward gold.

Understanding why that shift is happening, and how it fits into the broader structural story behind gold’s record-breaking run, matters for any investor trying to understand where prices could go from here.

What Is a Sovereign Wealth Fund?

The term gets used loosely, so it is worth being precise. A sovereign wealth fund (SWF) is a state-owned investment fund or entity that manages a country’s accumulated surplus capital, typically from oil revenues, trade surpluses, or foreign exchange reserves. The mandate varies by fund: some are set up purely to invest for future generations, others to stabilize government revenues, others to fund domestic development.

Sovereign wealth funds are distinct from a country’s central bank, though the line can blur. Central banks manage foreign exchange reserves with a primary focus on liquidity and capital preservation. Sovereign wealth funds typically have a longer time horizon and a broader investment universe that can include equities, private assets, infrastructure, and yes, commodities including gold. The Sovereign Wealth Fund Institute defines them as government-owned investment funds that are not central banks and not conventional public pension funds, though some sit close to both.

The Scale of Sovereign Capital

Numbers help here. According to the SWFI’s latest fund rankings, the ten largest sovereign wealth funds collectively manage a staggering concentration of state capital. Norway’s Government Pension Fund Global sits at the top with over $2 trillion in assets. SAFE Investment Company of China holds nearly $1.95 trillion. China Investment Corporation manages approximately $1.57 trillion. The Abu Dhabi Investment Authority has $1.13 trillion. Kuwait’s fund, Singapore’s GIC, and Saudi Arabia’s Public Investment Fund each hold between $900 billion and $1.1 trillion.

Even if gold represents a 1% allocation across these funds collectively, that translates to roughly $120 billion in demand. At current prices near $4,560 per ounce, that figure buys around 830 tonnes of gold, roughly equivalent to the entire official sector purchase volume in 2025. The math alone explains why institutional behavior matters so much to the gold market.

Why Gold, and Why Now?

Several structural forces have converged to make gold a more attractive holding for sovereign institutions, and 2025 brought most of them to a head simultaneously.

The Geopolitical Shock That Changed the Calculus

The February 2022 freezing of approximately $300 billion in Russian central bank reserves by Western governments sent a signal that state-owned assets held abroad are not immune from seizure during geopolitical conflict. For sovereign wealth funds in the Middle East, Asia, and emerging markets, this was not an abstract risk scenario. It was a live demonstration that foreign exchange reserves denominated in dollars, euros, or British pounds could be rendered inaccessible at the discretion of another government.

Gold held in domestic vaults cannot be frozen by a foreign government. It carries no counterparty risk of this type. For funds increasingly focused on sanctions exposure and geopolitical diversification, this characteristic has moved from a theoretical advantage to a practical necessity. The World Gold Council’s Central Bank Gold Reserves Survey 2025 found that 85% of respondents cited gold’s performance during times of crisis as a highly or somewhat relevant factor in their decision to hold it. That number reflects a community that has recently lived through exactly such a crisis.

Dollar Doubt Is Growing

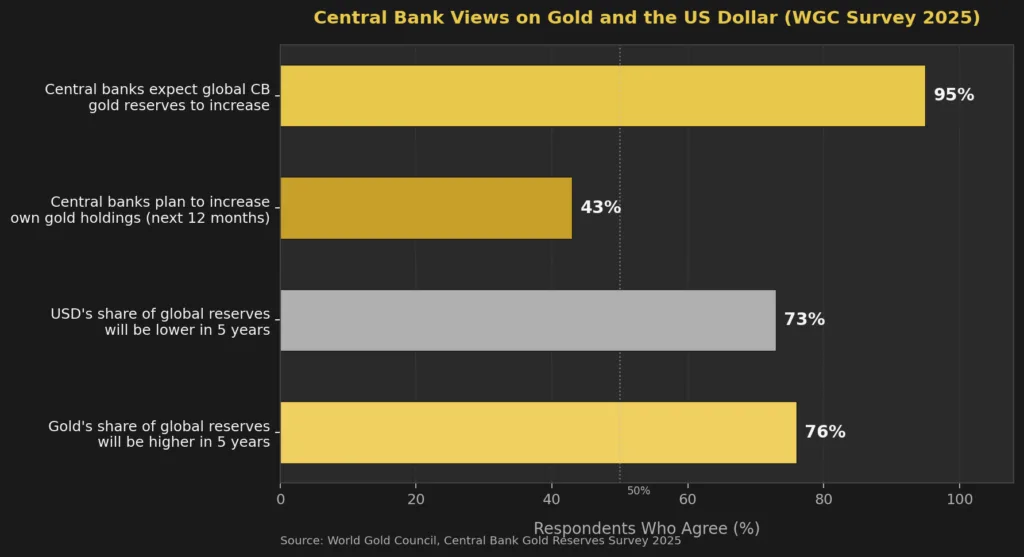

The dollar’s dominance in global reserves has eroded gradually for decades, but the pace of concern has accelerated. The WGC’s 2025 survey found that 73% of central bank respondents expect the US dollar’s share of global reserves to be lower five years from now, up meaningfully from prior years. At the same time, 76% expect gold’s share to be higher over the same period.

These expectations feed directly into sovereign wealth fund strategy. The IMF’s Currency Composition of Official Foreign Exchange Reserves (COFER) data already shows a gradual multi-year decline in the dollar’s share of global reserves. When fund managers at institutions with decades-long mandates see that trend and believe it will continue, they look for assets that do not depend on any single currency’s credibility. Gold is the most natural answer.

Portfolio Diversification at Scale

Beyond the geopolitical arguments, the basic portfolio logic for gold strengthened considerably across 2024 and 2025. Traditional reserve assets, primarily government bonds, delivered poor returns during the inflationary period that began in 2022, while gold returned 44% in dollar terms in 2025 alone. For SWFs with long-horizon mandates and boards that must justify performance, a metal that set 53 new all-time highs in a single year becomes much easier to allocate to. The WGC survey confirmed that 81% of central bank respondents consider gold’s diversification properties a relevant factor in holding it, and 80% value its role as a long-term store of value.

The Numbers Tell a Clear Story

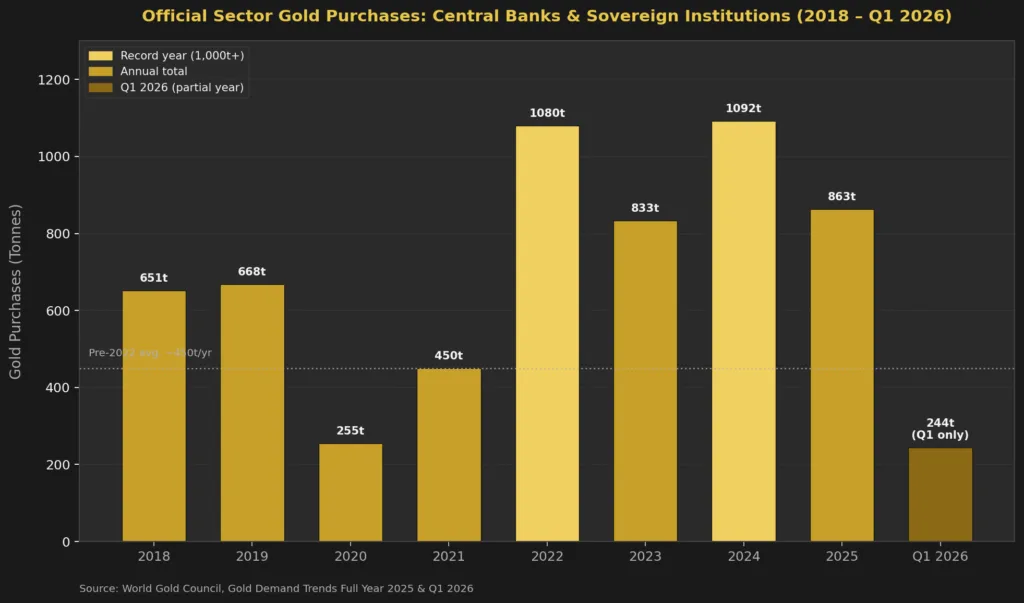

What we can document most precisely is the central bank side of official sector gold buying, since those purchases are disclosed to the IMF. According to the World Gold Council’s Gold Demand Trends: Full Year 2025, central banks bought 863 tonnes of gold in 2025. That followed 1,092 tonnes in 2024 and 833 tonnes in 2023. The three-year run of purchases above 800 tonnes per year is entirely without precedent in the modern era; the decade preceding 2022 averaged 400 to 500 tonnes annually.

In Q1 2026, the pace continued. The WGC’s Q1 2026 Gold Demand Trends report recorded 244 tonnes of central bank purchases in the first quarter, up 17% quarter-on-quarter, with Poland adding 31 tonnes and Uzbekistan adding 25 tonnes as the two largest individual buyers in the period. Notably, the WGC uses the term “central banks and other official institutions” in its accounting, which explicitly includes sovereign wealth fund-linked entities that manage official reserves.

The WGC’s 2025 survey of 73 central banks recorded that a record 43% of respondents planned to increase their own gold holdings over the next 12 months, up sharply from 29% in 2024. Crucially, not a single respondent expected their gold reserves to decrease.

Not All Sovereign Funds Are the Same

The sovereign wealth fund universe is not monolithic, and the relationship with gold differs meaningfully depending on a fund’s mandate, geography, and governance structure.

Norway’s Government Pension Fund Global is the largest in the world, but its investment mandate deliberately excludes commodities including gold. Its framework, set by the Norwegian government and managed by Norges Bank Investment Management, focuses on global equities and fixed income, with a small property allocation. Gold simply has no place in that mandate, regardless of geopolitical trends. This is worth knowing because Norway often gets cited as a benchmark for sovereign investment, and the absence of gold there should not be read as evidence that SWFs in general are uninterested.

Gulf funds tell a different story. The Kuwait Investment Authority, one of the world’s oldest sovereign wealth funds, has historically maintained exposure to gold as part of its reserve and diversification strategy. The Abu Dhabi Investment Authority’s publicly disclosed framework includes real assets and alternatives, a category that can encompass physical gold and gold-linked instruments. Saudi Arabia’s Public Investment Fund, while primarily focused on domestic economic transformation under Vision 2030, manages a portion of its assets in global financial markets where gold fits within a broader alternatives allocation.

In Asia, Singapore’s GIC does not publicly break down its portfolio at the asset class level, but its stated approach to real assets and inflation-sensitive instruments leaves room for gold exposure. China’s sovereign funds present a specific case: the People’s Bank of China has been one of the most active gold buyers in the world, and the boundary between central bank reserve management and CIC’s investment activities within China’s overall sovereign capital structure is not always cleanly separated in practice.

The Dollar Question: A Structural Shift

The de-dollarization discussion has been overhyped in many corners of the financial media, but the data from official institutions suggests something real is happening, just slowly. According to IMF COFER data, the dollar’s share of global foreign exchange reserves declined from around 71% in 2000 to approximately 57% by 2024. That is a significant long-run shift, even if it has been gradual and the dollar remains completely dominant.

The countries driving most of the non-dollar diversification are also the countries running the largest sovereign wealth funds: Gulf oil exporters, China, and several emerging market nations in Asia and Central Asia. When these fund managers reduce dollar exposure, they face a limited menu of alternatives with the liquidity, depth, and independence from political risk that gold provides. The euro, yen, and renminbi each carry their own dependencies. Gold is the asset that belongs to no one’s balance sheet.

What This Means for Gold Prices

The relationship between sovereign wealth fund strategy and gold prices operates at a timescale most retail investors underestimate. These institutions do not trade in and out of positions for short-term gain. When a fund with a multi-decade mandate decides to raise its gold allocation, it accumulates over months or years, smoothing its purchases to avoid moving the market. That kind of demand is structurally supportive rather than volatile.

The World Gold Council’s Gold Outlook 2026 noted that investors and central banks alike increased their gold allocations throughout 2025, seeking diversification and stability amid ongoing geoeconomic uncertainty. The report observed that gold’s role as a portfolio diversifier and source of stability remains the central justification for continued institutional accumulation, even at prices that would have seemed extraordinary a few years ago.

The math of marginal demand is worth thinking through clearly. According to WGC data, total annual gold mine supply runs at roughly 3,600 to 3,700 tonnes per year. When official sector institutions alone purchase 863 tonnes in a single year, and when that number looks set to remain elevated, the structural impact on the supply-demand balance is hard to dismiss. If sovereign wealth funds in aggregate added just 0.5% more gold exposure to their collective portfolios, that would represent demand equivalent to multiple months of global mine output entering the market over a relatively short period.

The Long View

Sovereign wealth funds are not going to abandon gold because the price dipped $200 or interest rates moved 25 basis points. Their time horizons are measured in decades, their mandates are tied to national policy objectives, and the factors driving their interest in gold, geopolitical risk, dollar uncertainty, inflation concerns, crisis performance, have if anything grown more relevant in the current environment. The WGC’s survey finding that 95% of central bank respondents expect global gold reserves to continue rising is a strong forward-looking signal. Sovereign wealth funds, which share many of the same concerns and often work alongside or within the same institutional frameworks as their countries’ central banks, are reading the same environment.

For retail investors holding physical gold, this context matters. You are not alone in your assessment that gold belongs in a portfolio right now. The funds managing the world’s largest pools of state capital are reaching a similar conclusion, just at a much larger scale.

Conclusion: Size Matters

The sovereign wealth fund story in gold is not one of a sudden rush or a dramatic announcement. It is quieter and more durable than that. Massive pools of government capital are shifting, slowly and deliberately, toward an asset that offers what very few others can: independence from the political decisions of any single country, proven performance through crises, and a finite supply that no treasury can print more of. When institutions managing $12 trillion collectively start moving in the same direction, the price effects play out over years, not days.

The record buying by official sector institutions since 2022, the growing expectations of further accumulation, and the structural shift away from dollar-denominated assets in global reserves are all pointing in the same direction. For gold, that direction is up, and the buyers driving it are among the most patient and well-capitalized investors on earth.