Gold prices held relatively steady on November 24, 2025, as two opposing forces created a balanced market environment that reveals the complex dynamics shaping precious metals in late 2025. On one hand, the U.S. dollar remained firm near a six-month high, which typically weighs on gold prices since gold is dollar-denominated, making it more expensive for holders of other currencies. On the other hand, increasing expectations that the Federal Reserve might cut interest rates soon supported gold, as lower interest rates reduce the opportunity cost of holding non-yielding assets like gold.

Understanding this tug-of-war between dollar strength and rate cut expectations provides crucial insights for investors navigating today’s precious metals market. The interplay reveals fundamental shifts in monetary policy, currency dynamics, and the evolving role of gold in portfolios during periods of economic transition.

According to the World Gold Council’s Q3 2025 Gold Demand Trends report, gold demand reached a record 1,313 tonnes in Q3 2025 despite prices trading near all-time highs. This combination of elevated prices and record demand demonstrates the structural strength underlying gold’s current market position, making the November price stability particularly noteworthy against the backdrop of competing macro forces.

The Dollar Strength Factor: Why Currency Matters for Gold

Understanding the Inverse Relationship

Gold’s price is quoted in U.S. dollars in international markets, creating a mathematical relationship where dollar strength mechanically affects gold prices. When the dollar appreciates against other major currencies, it takes fewer dollars to purchase the same ounce of gold, creating downward price pressure. Conversely, when the dollar weakens, gold prices typically rise in dollar terms.

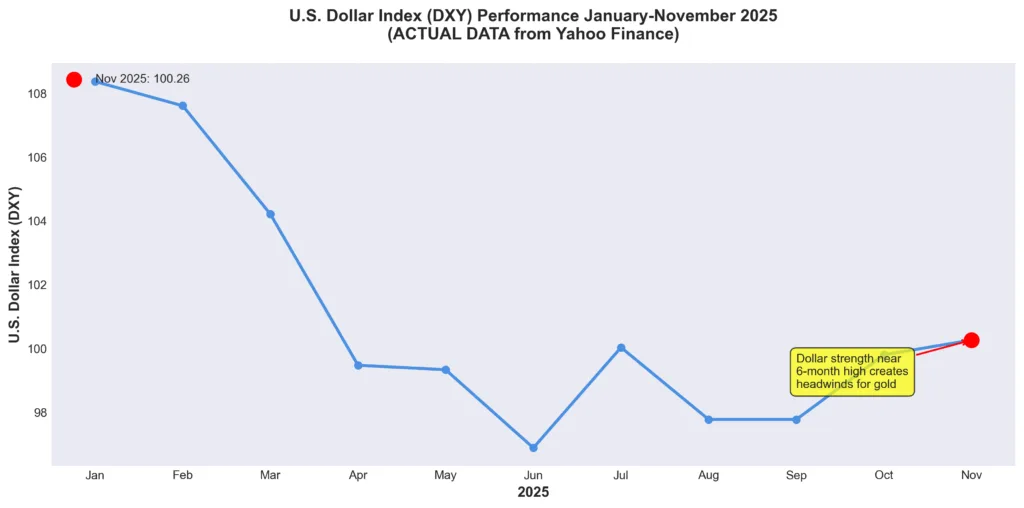

The U.S. Dollar Index (DXY), which measures the dollar against a basket of major currencies including the euro, yen, and pound sterling, provides the standard measure for dollar strength. The DXY reached 100.15 on November 24, 2025, marking a six-month high after recovering from a June low of 96.88. This recovery represents a 3.4% appreciation over five months, signaling that the dollar has strengthened significantly relative to other major currencies during the second half of 2025.

This matters for gold investors because approximately 40-50% of global gold demand comes from markets outside the United States, according to World Gold Council data. When the dollar strengthens, gold becomes more expensive in local currency terms for buyers in India, China, Europe, and other major markets. This price increase in local currencies typically suppresses physical jewelry and retail investment demand in those markets.

However, the relationship isn’t purely mechanical. As examined in our analysis of gold as a liquidity crisis indicator, gold can appreciate even during dollar strength when the underlying drivers relate to financial system stress or monetary policy expectations rather than currency flows alone.

What’s Driving Current Dollar Strength

Several factors have supported dollar strength through late 2025:

U.S. Economic Resilience: While global growth has slowed, the U.S. economy has demonstrated relative resilience compared to Europe and other developed markets. According to Bureau of Economic Analysis GDP data, the U.S. economy continued expanding through 2025 despite elevated interest rates and tightening financial conditions.

Interest Rate Differentials: Even as expectations build for Federal Reserve rate cuts, U.S. interest rates remain elevated relative to other major economies. The European Central Bank and Bank of Japan maintain significantly lower policy rates, creating yield differentials that support dollar demand from international investors seeking higher returns.

Safe Haven Flows: Geopolitical tensions and global economic uncertainty have driven safe haven flows toward U.S. dollar assets. Despite concerns about U.S. fiscal deficits, the dollar retains its status as the world’s primary reserve currency, attracting capital during periods of global stress.

As detailed in our examination of household debt crisis impacts, the U.S. faces significant structural challenges including record household debt exceeding $18.59 trillion. However, these longer-term concerns compete with near-term dollar support from relative economic strength and interest rate differentials.

Federal Reserve Rate Cut Expectations: The Countervailing Force

Why Lower Interest Rates Support Gold

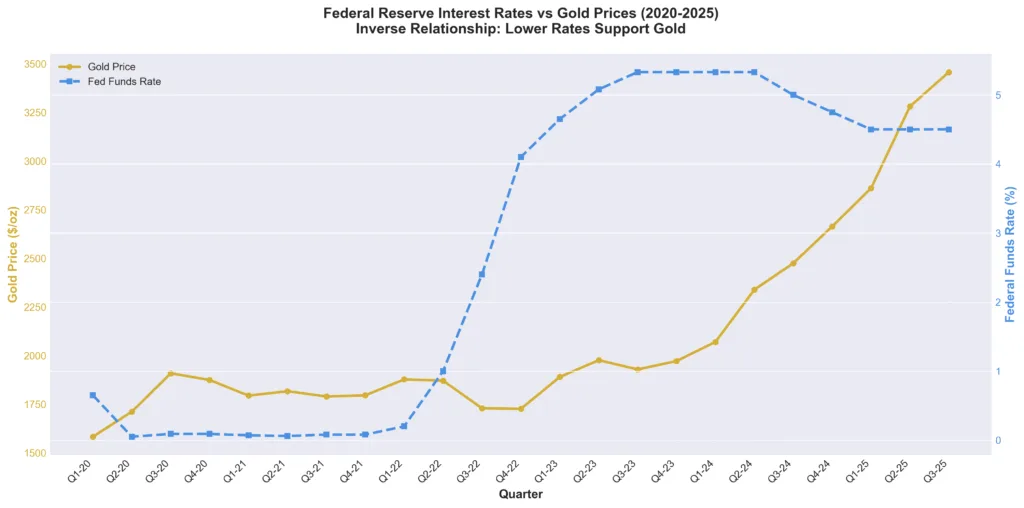

Gold pays no interest or dividend, which creates what economists call an “opportunity cost” for holding the metal. When interest rates rise, investors can earn significant returns from bonds, savings accounts, or other interest-bearing assets, making non-yielding gold relatively less attractive. Conversely, when rates decline, the opportunity cost of holding gold decreases, improving its relative appeal.

The relationship extends beyond simple opportunity cost. Lower interest rates typically signal several conditions that support gold appreciation:

Easier Monetary Conditions: Rate cuts expand money supply and credit availability, potentially weakening currency purchasing power over time. Gold’s fixed supply makes it attractive as currencies potentially lose value through monetary expansion.

Economic Growth Concerns: Central banks typically cut rates in response to economic weakness or recession fears. During such periods, gold’s safe haven characteristics become more valuable for portfolio diversification.

Real Interest Rate Compression: The “real” interest rate (nominal rate minus inflation) determines gold’s true opportunity cost. According to Federal Reserve economic data, when real rates decline or turn negative, gold historically performs well because investors aren’t sacrificing positive inflation-adjusted returns by holding the metal.

As examined in our analysis of Fed liquidity stress and gold, the Federal Reserve’s policy decisions extend beyond simple interest rate levels to encompass balance sheet management, quantitative easing programs, and emergency liquidity facilities. All these tools ultimately affect gold’s investment appeal.

Current Rate Cut Expectations and Why They Matter

The market’s expectation for Federal Reserve rate cuts in late 2025 and early 2026 reflects several converging factors:

Inflation Progress: After peaking above 9% in 2022, inflation has declined substantially though it remains above the Fed’s 2% target. According to Bureau of Labor Statistics Consumer Price Index data, core inflation (excluding food and energy) has proven persistently sticky around 3-4% through much of 2025. However, the trajectory shows progress that could give the Fed room to ease policy.

Labor Market Cooling: The previously overheated labor market has cooled considerably from 2022-2023 extremes. While unemployment remains relatively low, the pace of job creation has slowed and wage growth has moderated, suggesting less inflationary pressure from the labor market.

Banking System Stress: As detailed in our analysis of Fed liquidity stress, the banking system has shown signs of strain with increased usage of the Federal Reserve’s Standing Repo Facility and other emergency lending facilities. These stress signals often precede policy easing as the Fed prioritizes financial stability.

Political and Economic Pressures: With U.S. national debt exceeding $38 trillion, approximately 125% of GDP, the government faces substantial debt service costs. Interest payments on the national debt exceeded $1.2 trillion in fiscal year 2024, creating political pressure for lower rates to reduce borrowing costs.

The CME FedWatch Tool, which tracks market expectations for Federal Reserve policy based on futures pricing, showed significant probability of rate cuts by early 2026 as of November 2025. These expectations provide support for gold prices even as the dollar remains strong in the near term.

The Balancing Act: Why Gold Held Steady

Technical Factors Supporting Stability

The relative stability in gold prices on November 24, 2025, reflects a technical standoff between competing forces. Market analysis from Kitco metals trading data shows that gold found support at key technical levels even as dollar strength created headwinds.

This stability demonstrates what technical analysts call “consolidation”, a period where prices trade within a range as markets digest previous gains and await catalysts for the next major move. After gold’s substantial appreciation through 2024 and into 2025, with the metal reaching a record high of $4,381 per ounce on October 30, 2025, according to Reuters reporting, a period of consolidation represents healthy market behavior rather than weakness.

As examined in our analysis of gold bull market corrections, temporary price stability or modest pullbacks within ongoing bull markets serve essential functions: resetting overbought technical conditions, clearing speculative excess, and creating entry points for new buyers who will support the next leg higher.

Fundamental Demand Remains Robust

Despite the competing pressures from dollar strength and rate cut expectations, gold’s fundamental demand picture remains exceptionally strong, providing a floor under prices.

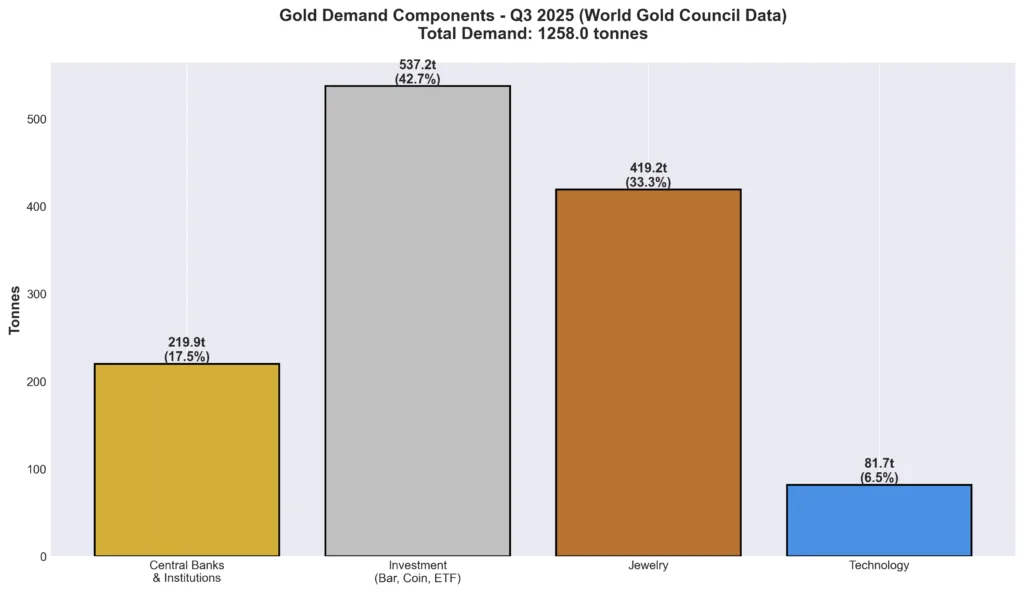

Central Bank Accumulation: According to World Gold Council data, central banks purchased 634 tonnes of gold in the first nine months of 2025 (January through September). At this pace, full-year 2025 central bank purchases could potentially approach or exceed 800 tonnes, which would mark the fourth consecutive year of elevated official sector accumulation. As detailed in our analysis of who’s buying all the gold, this institutional buying at record price levels signals profound conviction about gold’s long-term value proposition.

Central banks possess confidential data about financial system health and operate with multi-decade time horizons. Their sustained accumulation at prices near all-time highs suggests they view current levels as attractive relative to long-term risks from currency debasement, fiscal unsustainability, and monetary system fragility.

Investment Demand Surge: Investment demand reached 537 tonnes in Q3 2025, up 47% year-over-year according to World Gold Council data. This includes physical bar and coin demand of 315 tonnes plus significant ETF inflows of 222 tonnes. Gold-backed exchange-traded products experienced their largest monthly inflow ever in September 2025, totaling $17 billion, demonstrating institutional conviction despite elevated prices.

Supply Constraints: Mine production growth remains anemic despite gold reaching record price levels above $4,300 per ounce in late October. World Gold Council supply data shows mining output increased only 2% year-over-year through 2025. Declining ore grades, extended development timelines for new projects, and capital intensity constraints limit the supply response to strong demand, providing structural price support.

Historical Context: Similar Episodes and Their Resolution

The 2019 Playbook

A similar dynamic played out in late 2019 when gold faced competing pressures from a strengthening dollar and emerging signs of Federal Reserve policy easing. After the September 2019 repo crisis revealed banking system liquidity stress, the Fed began expanding its balance sheet through Treasury bill purchases while maintaining its policy rate.

Gold initially consolidated around $1,470-1,550 per ounce through late 2019 as markets processed these mixed signals. However, once the Fed’s pivot toward easing became unmistakable in early 2020 (accelerated by the COVID crisis), gold surged to new all-time highs above $2,060 by August 2020, representing a gain exceeding 40% from the late 2019 consolidation levels.

The lesson: periods where gold holds steady amid competing pressures often precede sustained appreciation once the direction of monetary policy becomes clear and currency debasement concerns dominate short-term dollar strength.

The 1970s Precedent

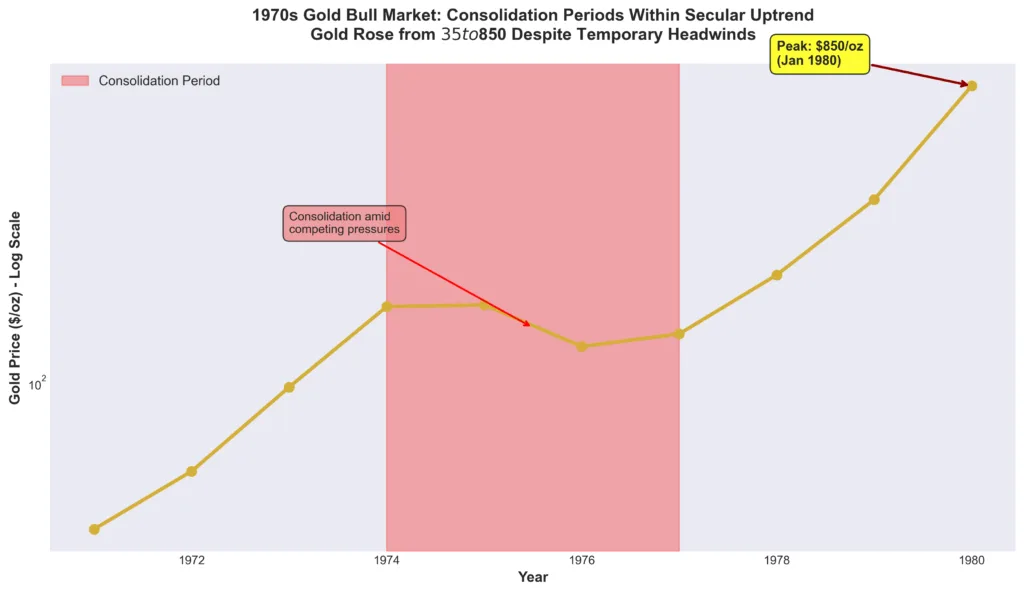

The legendary 1970s gold bull market featured numerous episodes where competing forces created temporary price stability before gold resumed its advance. As examined in our analysis of structural bull markets, the period from 1971 to 1980 saw gold rise from $35 per ounce to over $850, but this journey included five corrections exceeding 15%, numerous periods of consolidation, and times when dollar strength created headwinds.

Throughout these temporary setbacks, the fundamental drivers remained intact: persistent inflation, currency debasement through monetary expansion, fiscal deficits, and geopolitical uncertainty. Investors who maintained conviction in these structural factors, rather than being shaken out by short-term volatility or competing technical pressures, captured the full magnitude of gold’s appreciation.

Current conditions feature striking similarities: inflation running above central bank targets, massive fiscal deficits, mounting debt levels across household and government sectors, and a Federal Reserve caught between fighting inflation and supporting growth. These structural factors suggest the current consolidation represents a pause within an ongoing trend rather than a fundamental reversal.

What This Means for Gold Investors

Short-Term Noise Versus Long-Term Signal

The competing pressures of dollar strength and rate cut expectations create short-term price volatility and consolidation, but they don’t alter the fundamental case for gold allocation within diversified portfolios. As examined in our analysis of gold’s job in investment strategy, gold serves distinct portfolio functions that remain valuable regardless of short-term price movements:

Portfolio Diversification: Gold’s low correlation with stocks and bonds provides diversification benefits particularly during periods of financial stress when traditional assets decline simultaneously.

Inflation Hedge: With inflation remaining above central bank targets despite aggressive rate hikes, gold’s historical role as an inflation hedge remains relevant. Even as the Fed potentially cuts rates, inflation concerns persist, supporting gold’s appeal.

Currency Debasement Protection: Regardless of whether the dollar is strong or weak in the near term, the long-term trajectory of currency debasement through monetary expansion and fiscal deficits supports gold’s role as a store of value with fixed supply.

Systemic Insurance: As detailed in our analysis of banking system stress, gold provides insurance against financial system fragility that becomes particularly valuable when credit markets face strain or banking system stability comes into question.

Strategic Positioning Considerations

Current market dynamics suggest several considerations for investors:

Dollar-Cost Averaging: Periods of consolidation where competing forces create stability offer attractive conditions for systematic accumulation. Dollar-cost averaging removes the pressure to time perfect entries while ensuring consistent exposure to long-term trends.

Physical Ownership Benefits: During periods of monetary policy transition and currency uncertainty, physical gold in coins and bars provides ownership without counterparty risk. Physical metal maintains value regardless of institutional solvency or financial system stress, characteristics that become particularly valuable during uncertain times.

Patience With Timing: Investors without immediate need can benefit from patience, recognizing that the resolution of competing pressures between dollar strength and rate cut expectations will eventually tilt decisively in one direction. Historical precedent suggests that once monetary policy direction becomes clear, gold responds decisively.

Complement With Silver: As examined in our analysis of the gold-silver ratio, silver provides leverage to gold price moves while offering additional industrial demand drivers. The precious metals complex benefits from similar monetary dynamics while offering diversification within the asset class.

Conclusion: Navigating Competing Pressures

Gold prices holding steady on November 24, 2025, amid competing pressures from dollar strength and rate cut expectations tells an important story about the current precious metals market. Rather than representing weakness or indecision, this stability demonstrates gold functioning as a sophisticated asset that responds to multiple fundamental factors simultaneously.

The dollar’s strength near six-month highs creates mechanical headwinds for dollar-denominated gold prices, particularly affecting international demand as gold becomes more expensive in local currency terms. However, increasing expectations for Federal Reserve rate cuts provide countervailing support by reducing the opportunity cost of holding non-yielding assets and signaling potentially easier monetary conditions ahead.

Historical precedent from similar episodes in 2019 and throughout the 1970s bull market suggests that periods of consolidation amid competing pressures often precede sustained appreciation once monetary policy direction becomes clear and structural factors reassert dominance over near-term technical pressures.

The fundamental case for gold allocation remains intact regardless of short-term price movements. Central banks continue accumulating metal at record prices, investment demand surges despite elevated valuations, and supply growth remains constrained by geological and economic factors. These structural drivers suggest current consolidation represents a healthy pause within an ongoing trend rather than a fundamental reversal.

Whether you’re establishing initial precious metals positions or expanding existing holdings, Bullion Trading LLC offers comprehensive gold and silver solutions backed by market expertise and commitment to investor education. In a market environment where gold navigates competing pressures from dollar strength and rate cut expectations, strategic allocation to physical precious metals ensures your portfolio benefits from gold’s unique characteristics regardless of which force ultimately prevails.