The debate between gold and real estate investment has captivated wealth builders for generations. As we navigate through 2025’s complex economic landscape, characterized by persistent inflation pressures, fluctuating interest rates, and geopolitical uncertainties, this question has never been more relevant for investors seeking to preserve and grow their wealth.

Both asset classes have proven their worth over centuries, yet they serve fundamentally different purposes in a diversified portfolio. Real estate offers tangible shelter and potential income generation, while gold provides ultimate liquidity and acts as a monetary hedge against economic instability. Understanding the nuances between these two investment vehicles is crucial for making informed allocation decisions that align with your financial goals.

Historical Performance: Long-Term Returns Comparison

Gold’s 5,000-year history as a store of value provides unparalleled perspective on wealth preservation. According to World Gold Council data, gold has delivered strong long-term returns over the past two decades, with annualized gains significantly outperforming inflation during this period.

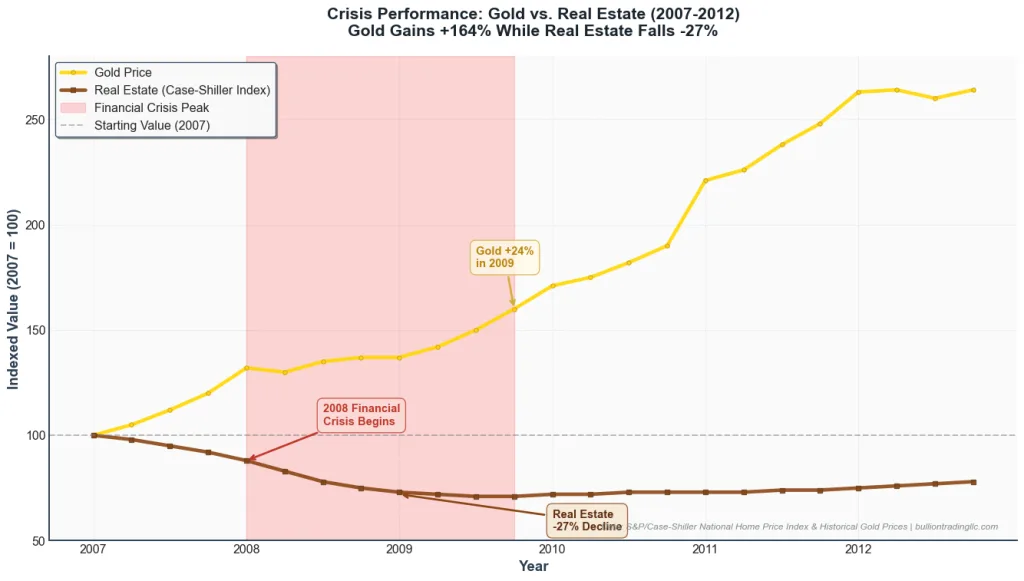

The precious metal’s performance becomes particularly compelling during economic stress. During the 2008 financial crisis, while real estate values declined approximately 27% nationally (per the S&P/Case-Shiller National Home Price Index), gold prices gained approximately 24% in 2009 alone. In 2025, gold has achieved record highs, surging above $3,900-$4,000 per ounce in early October, representing year-to-date gains of approximately 40-50%, as documented in our recent market analysis.

Real estate has also demonstrated robust long-term performance, though with notable cyclical variations. According to the Federal Housing Finance Agency (FHFA), U.S. home prices in the repeat-sales purchase index have appreciated at approximately 4.2-4.3% per year from 1991 through 2023. The median existing single-family home price reached $429,400 in Q2 2025, according to National Association of Realtors (NAR) data. However, returns vary dramatically by location and market conditions. The 2008 housing crash wiped out decades of gains in many markets, with properties not recovering to pre-crisis values until 2016-2017.

During the high-inflation 1970s, gold prices increased from $35 per ounce to $850 by 1980, a staggering 2,329% gain. Real estate also performed well with median home prices rising approximately 166%, though significantly underperforming gold’s explosive growth.

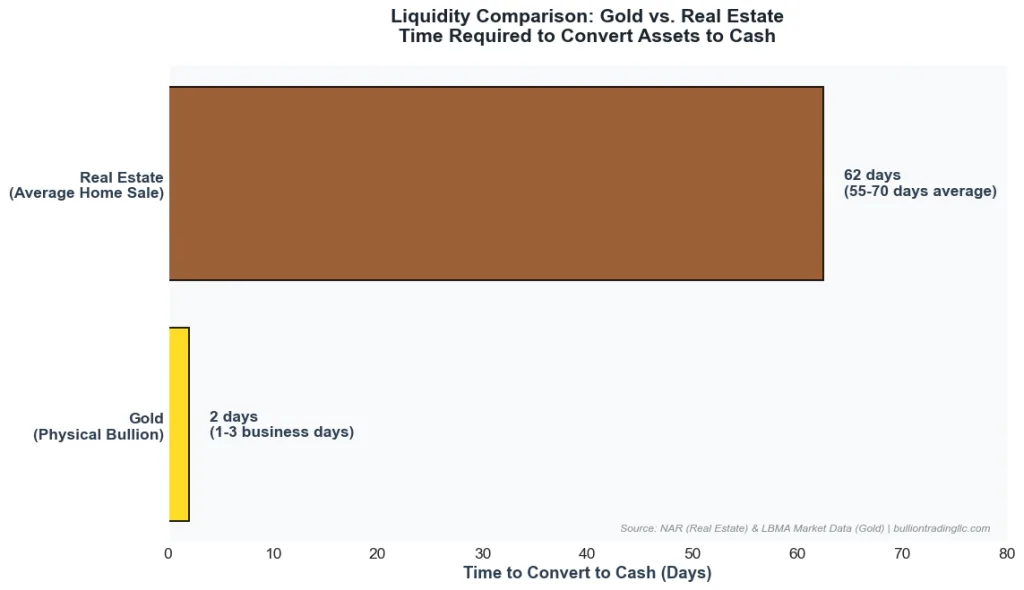

Liquidity: Converting Assets to Cash

Gold’s Unmatched Liquidity

One of gold’s most compelling advantages is its exceptional liquidity. Physical gold bullion can be sold within hours through reputable dealers, with payment typically received within 1-3 business days. The global gold market processes substantial daily trading volumes according to the London Bullion Market Association, ensuring consistent pricing and immediate market access.

For investors seeking the best types of gold for investment, government-minted coins like American Gold Eagles and Canadian Maple Leafs offer the highest liquidity due to widespread recognition. The entire transaction, from price agreement to shipping, can be completed in under 48 hours.

Real Estate’s Illiquidity Challenge

Real estate represents one of the least liquid major asset classes. The National Association of Realtors reports that the average home sale takes 55-70 days from listing to closing under normal market conditions, and potentially months longer in buyer’s markets.

Transaction costs compound real estate’s illiquidity. Selling property typically incurs 8-10% in total costs including real estate commissions (5-6%), closing costs (2-3%), repairs (1-3%), and transfer taxes (0.5-2%). These substantial costs mean real estate must appreciate significantly before generating positive returns, whereas gold transactions typically involve premiums of 1-5% over spot price.

Initial Capital Requirements and Accessibility

Gold’s Low Barrier to Entry

Gold investment requires minimal initial capital, making it accessible across all wealth levels. At Bullion Trading LLC, investors can begin building their precious metals portfolio with as little as $1,000, acquiring fractional-ounce coins or smaller bars.

This scalability allows for dollar-cost averaging strategies that reduce timing risk. Gold’s divisibility, available from 1-gram bars to 400-ounce bars, provides unprecedented flexibility. Furthermore, gold requires no financing, eliminating leverage risk and interest expense.

Real Estate’s Substantial Capital Barrier

Real estate demands significant upfront capital. The median existing single-family home price reached $429,400 in Q2 2025 (per NAR data). With a 20% down payment, buyers need approximately $85,880 in liquid capital, plus additional reserves for closing costs and repairs.

This creates concentration risk, as most investors can only afford one or two properties. Most rely on mortgage financing, introducing leverage risk that amplifies both gains and losses. The 2008 crisis saw millions of homeowners with negative equity, owing more than their properties’ worth.

Ongoing Costs and Maintenance

Gold’s operating costs are remarkably low. Once purchased, gold requires only secure storage, bank safe deposit boxes ($60-300 annually) or professional vault storage (0.5-1% of value annually). Gold requires no maintenance, generates no utility bills, needs no repairs, and never depreciates. A gold bar purchased today will have identical characteristics in 100 years.

Real estate ownership entails numerous recurring costs. Experts estimate that homeowners spend between 1–4% of their home’s value on maintenance and repair annually.

Additional costs include:

- Property Taxes: Averaging 1.1% nationally ($4,805 annually for median home)

- Insurance: Averaging $1,428 annually

- HOA Fees: Often $2,400-4,800 annually

- Major Repairs: Roof replacement ($8,000-20,000), HVAC ($5,000-10,000) every 10-20 years

These carrying costs mean real estate must appreciate 3-5% annually just to break even, whereas gold’s minimal costs allow nearly all price appreciation to translate into investor gains.

Income Generation and Tax Implications

Gold produces no income stream. Unlike dividend-paying stocks or rental properties, gold generates no cash flow while held. However, the World Gold Council notes that gold’s price appreciation has historically compensated for its absence of yield, particularly during inflationary environments.

Investment real estate offers potential rental income. National Association of Realtors data shows investment properties typically generate gross rental yields of 6-10% annually, though net yields after expenses typically range from 2-5%. However, rental income comes with vacancy risk, tenant issues, and management burden.

Tax Considerations

Physical gold faces capital gains tax upon sale, with the IRS classifying precious metals as “collectibles” subject to a maximum 28% long-term rate. However, no tax applies until sale, allowing decades of compound growth without annual tax drag.

Real estate enjoys numerous tax advantages: mortgage interest deduction, property tax deduction (up to $10,000 SALT), depreciation over 27.5 years, 1031 exchanges for deferring gains, and capital gains exclusion of $250,000 ($500,000 married) on primary residences. However, these advantages come with significant complexity and record-keeping requirements.

Risk Factors and Market Volatility

Gold prices fluctuate daily based on currency movements, interest rates, inflation expectations, and geopolitical events. According to data, gold’s 90-day volatility in mid-2025 has ranged from 17-22%. However, gold typically exhibits negative correlation with risk assets during market stress, making its volatility valuable for portfolio diversification.

Key gold price drivers include real interest rates, U.S. dollar strength, central bank policy, and geopolitical uncertainty. Modern gold investors benefit from transparent global pricing, ensuring fair price discovery even during volatile periods.

While real estate experiences less day-to-day price visibility, its volatility over complete market cycles can be substantial. The S&P CoreLogic Case-Shiller Index declined 27.4% from peak to trough during 2007-2012, with many individual markets experiencing 40-50% declines.

Real estate’s illiquidity amplifies volatility’s impact. Additional risk factors include local market dependence, natural disasters, regulatory changes, demographic shifts, interest rate sensitivity, and maintenance catastrophes. The Federal Housing Finance Agency provides extensive data on housing market volatility.

The Verdict: Which Investment Is Better?

After comprehensive analysis, the conclusion becomes clear: neither gold nor real estate is universally “better”, each serves distinct purposes within properly structured portfolios.

Choose Gold as Primary Focus If You:

- Prioritize liquidity and flexibility

- Face geographic mobility needs

- Seek crisis insurance and monetary protection

- Prefer minimal management responsibilities

- Have limited capital to deploy (<$50,000)

- Are concerned about currency debasement and inflation

Choose Real Estate as Primary Focus If You:

- Seek income generation from investments

- Can commit substantial capital ($100,000+)

- Have stable geographic situation

- Benefit from real estate tax advantages

- Have time horizon exceeding 5-7 years

- Possess property management skills or interest

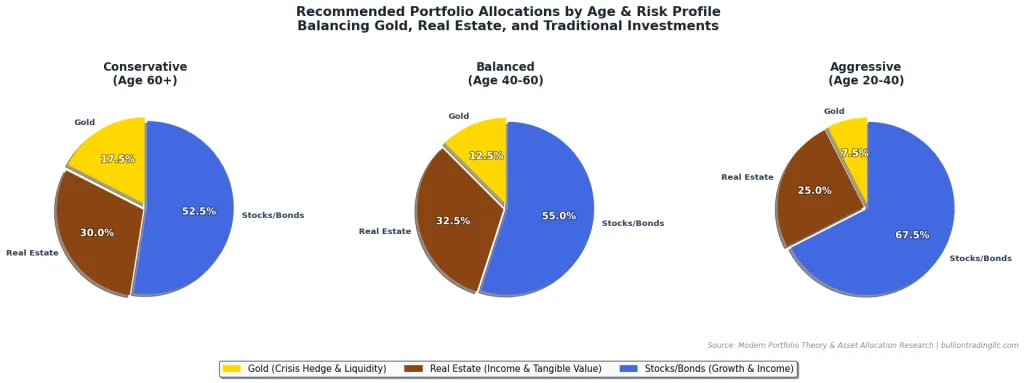

Optimal Strategy: Include Both Assets

For most investors, the ideal approach incorporates both assets in proportions aligned with personal circumstances:

Conservative Portfolio (Age 60+):

- 15-20% Gold (liquidity and crisis protection)

- 30% Real Estate (primary residence, possibly one rental)

- 50-55% Stocks/Bonds (growth and income)

Balanced Portfolio (Age 40-60):

- 10-15% Gold (portfolio insurance)

- 30-35% Real Estate (primary residence, 1-2 investments)

- 50-60% Stocks/Bonds (growth focus)

Aggressive Portfolio (Age 20-40):

- 5-10% Gold (crisis hedge)

- 20-30% Real Estate (possibly primary residence only)

- 60-75% Growth stocks (maximize appreciation)

Important Note: These allocation models serve as general guidelines only. There is no single “best” portfolio allocation, the optimal mix depends entirely on your unique financial situation, investment goals, risk tolerance, income needs, and personal circumstances. Before making any investment decisions, consider consulting with a qualified financial advisor who can assess your specific situation and help create a customized allocation strategy aligned with your objectives.

Conclusion: Building Wealth Through Strategic Diversification

The gold versus real estate debate has captivated investors for generations, but framing it as binary choice misses the fundamental principle of diversification. Both assets have demonstrated wealth preservation capabilities over centuries, yet they accomplish this through different mechanisms.

Gold offers unmatched liquidity, minimal carrying costs, geographic portability, and crisis protection. Its 2025 performance, achieving record prices above $3,900 per ounce with year-to-date gains exceeding 41%, demonstrates its enduring value as monetary insurance. Central banks continue accumulating gold at unprecedented rates, reflecting concerns about currency stability and geopolitical risks.

Real estate provides tangible shelter value, income generation potential, substantial tax advantages, and forced savings through mortgage amortization. Despite challenges with liquidity and concentration risk, real estate remains a cornerstone of wealth building for most families.

The optimal strategy for most investors involves thoughtful allocation to both assets within broadly diversified portfolios. Rather than choosing one over the other, successful wealth builders recognize that gold and real estate serve complementary purposes, gold providing liquidity and crisis protection, real estate offering tangible value and income generation.

As you consider your allocation decisions, assess your personal situation across liquidity needs, income requirements, risk tolerance, time horizon, and geographic flexibility. For many investors, beginning with a modest gold position provides portfolio insurance while maintaining flexibility to pursue real estate opportunities as capital and circumstances allow.

At Bullion Trading LLC, we specialize in helping investors implement gold allocation strategies aligned with their comprehensive financial plans. Our extensive inventory of gold bullion, silver products, and platinum offerings provides the physical assets needed to execute sophisticated portfolio strategies. Whether you’re beginning your precious metals journey or expanding existing positions, our team stands ready to provide the expertise and products necessary for successful implementation.