Something critical is happening beneath the surface of financial markets that most investors aren’t paying attention to. The overnight funding markets, the essential plumbing that moves cash between banks every single night, started showing stress signals in late 2024 and early 2025. When these pipes get clogged, the entire financial system feels it immediately.

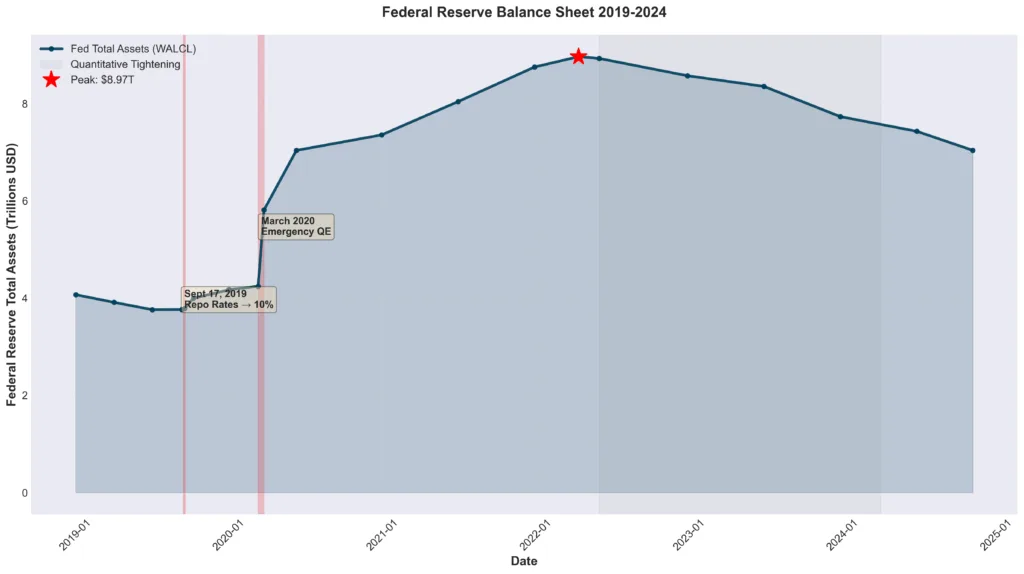

The Federal Reserve ended quantitative tightening (QT) earlier than planned because the banking system was running dangerously low on reserves. When banks don’t have enough liquidity, overnight markets start showing strain. We’ve seen this movie before. The exact same pattern emerged in September 2019 when repo rates spiked to 10%, forcing the Fed to intervene with emergency liquidity operations. That intervention marked the unofficial end of the previous QT cycle, even though the Fed didn’t formally announce it until March 2020.

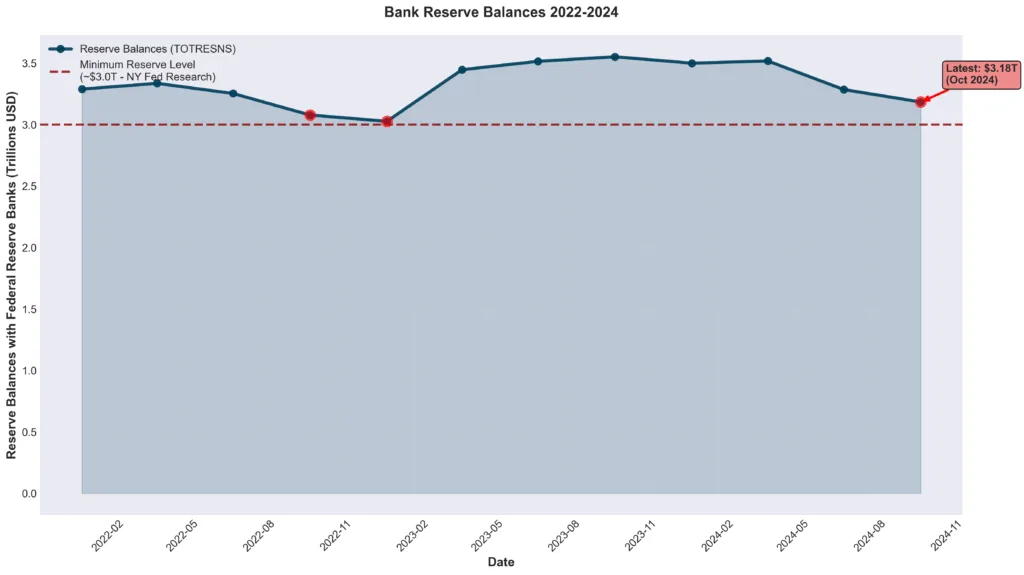

According to Federal Reserve data on bank reserves, total reserve balances have declined substantially from their pandemic peak of over $4 trillion to approximately $3.4 trillion by late 2024. This matters because research from the Federal Reserve Bank of New York suggests the banking system requires approximately $3 trillion in reserves to function smoothly without stress. We’re approaching that threshold again.

Even after the Fed officially stopped QT, funding conditions remained strained. Banks began using the Fed’s Standing Repo Facility (SRF) and discount window more frequently, clear signs that the system is running short on cash. The Federal Reserve’s H.4.1 statistical release shows elevated usage of these emergency lending facilities throughout late 2024 and into 2025.

Why the Fed Stopped QT: It Wasn’t Optional

The Federal Reserve didn’t end quantitative tightening because inflation was conquered or because the economy was strong. They stopped because they had to. The banking system was sending unmistakable distress signals through stressed funding markets.

As detailed in our analysis of gold as a liquidity crisis indicator, when overnight funding markets tighten, it reveals that bank reserves have fallen below comfortable levels. Banks become reluctant to lend to each other, hoarding liquidity for their own needs. This hoarding behavior creates a vicious cycle where liquidity tightens further.

Goldman Sachs research from late 2024 projected that the Fed would need to begin quietly growing its balance sheet again through what they call “reserve management purchases.” Let’s be clear about what this actually means: it’s quantitative easing by another name. The Fed will be buying Treasury bills to inject reserves back into the banking system.

The 2019 Playbook Repeats

The September 2019 repo crisis provides the clearest template for understanding current conditions. Overnight repo rates, which typically trade close to the Fed’s policy rate, suddenly spiked to 10% on September 17, 2019. According to Federal Reserve research on the 2019 repo spike, the crisis emerged when reserve levels fell below the threshold needed for smooth market functioning.

The Fed responded immediately with emergency repo operations, injecting hundreds of billions in liquidity. Within months, they formally restarted balance sheet expansion, though they carefully avoided calling it QE. The pattern was identical to today: QT pushed reserves too low → funding stress emerged → Fed reversed course with balance sheet expansion.

What Reserve Management Really Means for Gold

When the Fed expands its balance sheet through reserve management purchases or any other mechanism, it creates more dollars. More dollars chasing the same amount of goods means each dollar buys less, basic monetary economics.

But there’s a more immediate effect on gold. Balance sheet expansion increases bank reserves, which lowers the dollar’s value relative to hard assets. As examined in our analysis of Fed rate cuts and gold prices, gold doesn’t wait for formal announcements of stimulus. It reacts to stress happening behind the scenes in the financial system’s plumbing.

The sequence works like this:

- Banking system runs low on liquidity → Reserve balances fall below comfort levels

- Overnight funding markets show stress → Banks increase emergency borrowing

- Fed forced to add reserves → Balance sheet expansion through Treasury purchases

- Dollar foundation weakens → More currency units outstanding relative to economic activity

- Gold appreciates → Fixed supply becomes more valuable relative to expanding currency

According to World Gold Council Q3 2025 data, gold demand reached 1,313 tonnes in Q3 2025 despite prices trading near all-time highs. As detailed in our Q3 demand analysis, central banks purchased 219.9 tonnes in Q3 alone, up 28% from Q2. These sophisticated institutions with decades-long time horizons are accumulating gold precisely because they understand the liquidity dynamics forcing Fed balance sheet expansion.

The Standing Repo Facility: The Quiet Alarm

The Fed established the Standing Repo Facility (SRF) in July 2021 as a permanent backstop for overnight funding markets. Think of it as an emergency lending window where banks can borrow cash overnight using Treasury securities as collateral. Banks pay a penalty rate, currently 10 basis points above the Fed’s policy rate, to access this facility.

Usage of the SRF remained minimal throughout 2022 and most of 2023. But Federal Reserve statistical releases show increased SRF usage beginning in late 2024. This matters enormously because banks only use penalty-rate facilities when they can’t obtain funding through normal channels at better rates.

Rising SRF usage signals that overnight funding markets are tight. When funding is abundant, no bank would pay a penalty rate. They’d simply borrow from other banks at standard rates or use excess reserves. Elevated SRF usage tells you the system is running short on cash.

Why This Environment Is Textbook Bullish for Gold

Gold performs best not during announced stimulus programs, but during the period when financial stress builds and forces policy responses. By the time the Fed officially announces a program, gold has typically already priced in much of the move.

The current environment features every characteristic that historically precedes major gold appreciation:

1. Forced Balance Sheet Expansion

Unlike discretionary QE programs launched to stimulate growth, reserve management purchases occur because the system requires them. The Fed isn’t choosing to expand the balance sheet, they’re being forced to by liquidity dynamics. This distinction matters because forced interventions tend to be larger and more sustained than discretionary stimulus.

2. Weakening Dollar Foundation

More liquidity equals a bigger Fed balance sheet, which equals more dollars relative to economic output. According to Federal Reserve economic data, M2 money supply has expanded substantially since 2020, even accounting for the 2022-2023 decline during QT. Balance sheet re-expansion will resume this trend.

A larger monetary base relative to real economic activity inevitably weakens the currency’s purchasing power over time. Gold, with its fixed supply constrained by mining output of approximately 1.5% annually, becomes more valuable relative to the expanding fiat currency supply.

3. Persistent Inflation Pressures

The Fed ended QT despite inflation remaining above their 2% target. According to Bureau of Labor Statistics CPI data, core inflation has proven remarkably sticky, consistently running above 3% through much of 2024 and into 2025. The Fed’s tolerance for above-target inflation combined with forced balance sheet expansion creates exactly the combination that supported gold’s bull markets in the 1970s and 2000s.

As examined in our analysis of U.S. household debt crisis, current conditions mirror key aspects of 1970s stagflation: slowing growth, persistent inflation, and mounting debt levels that encourage inflationary monetary policy.

4. Central Bank Accumulation

Central banks purchased approximately 634 tonnes of gold through Q3 2025 according to World Gold Council preliminary data. This buying continues at elevated levels despite gold trading near record prices above $4,000 per ounce. Central banks have access to confidential data about banking system health. Their sustained accumulation at high prices signals their assessment of long-term currency risk.

When institutions with multi-decade time horizons and the best available data accumulate gold aggressively, retail investors questioning whether “gold is expensive” fundamentally misunderstand the asset’s role.

The Policy Box: Why The Fed Can’t Escape

The Federal Reserve faces an impossible policy dilemma that ultimately supports gold:

Scenario 1: Maintain Tight Policy

- Banking system runs out of reserves

- Funding markets seize up

- Credit crunch threatens real economy

- Fed forced to add liquidity anyway

- Outcome: Balance sheet expansion → Gold positive

Scenario 2: Ease Policy Proactively

- Lower rates and expand balance sheet

- Inflation persists or re-accelerates

- Dollar weakens from monetary expansion

- Outcome: Currency debasement → Gold positive

As detailed in our analysis of gold bull market corrections, this policy box creates asymmetric risk/reward for gold investors. The downside scenarios (deflation, strong dollar) get prevented by Fed intervention, while the upside scenarios (inflation, dollar weakness) become more likely.

The U.S. national debt exceeding $38 trillion, approximately 125% of GDP, further constrains Fed options. High debt levels make sustained tight monetary policy economically unsustainable due to debt service costs. The government paid over $1.2 trillion in interest in fiscal year 2024, approaching 20% of total federal revenue.

These debt dynamics create structural bias toward lower rates and expanded money supply over time, both supportive for gold.

What It Means for Gold Investors

Understanding liquidity stress dynamics provides crucial context for gold investment decisions:

Don’t Confuse Volatility With Weakness

Gold experienced notable intraday volatility during late 2024 and early 2025, with some sessions showing 3-5% price swings. Market commentary often interprets this as gold weakness. But as we examined in our liquidity crisis indicator analysis, gold’s volatility during funding market stress typically precedes major appreciation.

The volatility doesn’t indicate problems with gold, it reveals gold functioning as a liquid asset that institutions sell when they need to raise cash quickly during stress periods. This temporary selling creates opportunities for patient investors who understand the pattern.

Focus on Structural Drivers

The fundamental case for gold strengthens with every sign of liquidity stress:

- Banking system requires Fed intervention

- Intervention involves balance sheet expansion

- Expansion increases money supply

- Increased supply relative to fixed gold supply supports appreciation

Short-term price moves driven by technical factors, options expiration, month-end rebalancing, create noise around this structural signal.

Physical Ownership Eliminates Counterparty Risk

During periods of banking system stress, physical gold provides insurance that financial assets cannot match. Physical gold carries zero counterparty risk, it maintains value regardless of any institution’s solvency. As explored in our gold vs. real estate analysis, this characteristic becomes particularly valuable during financial system uncertainty.

Historical Precedent: 2019 Repo Crisis Aftermath

The September 2019 repo crisis provides the cleanest historical precedent for current conditions. After repo rates spiked to 10%, the Fed initially conducted temporary repo operations. But by October 2019, they announced a program to purchase $60 billion monthly in Treasury bills to expand the balance sheet.

Gold’s response proved instructive. From September 2019 through August 2020, gold rallied from approximately $1,470 per ounce to over $2,060, a gain exceeding 40%. The rally accelerated in March 2020 when the COVID crisis forced even more aggressive Fed intervention, but the foundation was established when the 2019 liquidity stress revealed the Fed’s commitment to maintaining abundant reserves.

Current conditions feature the same dynamics: QT pushed reserves too low, funding stress emerged, Fed will respond with balance sheet expansion. Investors who understand this pattern recognize that temporary gold weakness during the stress phase typically precedes sustained appreciation during the policy response phase.

Practical Implementation

For investors positioning portfolios for the liquidity-driven environment ahead:

Core Physical Holdings

Physical gold in coins and bars provides pure exposure with zero counterparty risk. Popular sovereign coins like American Gold Eagles, Canadian Gold Maples, or Austrian Philharmonics offer high liquidity with recognizable government minting. Larger bars provide lower premiums for substantial positions.

Systematic Accumulation

Dollar-cost averaging removes timing anxiety while ensuring consistent exposure. Making regular purchases captures both strength and weakness, reducing impact of short-term volatility while building positions aligned with structural drivers.

Appropriate Position Sizing

Conventional wisdom suggests 5-15% precious metals allocation for most investors, though specific circumstances vary. Size positions such that volatility doesn’t force liquidation at inopportune times. The psychological ability to hold through 10-20% corrections separates successful gold investors from those who sell at precisely the wrong moment.

Complement With Silver

Silver provides leverage to gold moves while offering additional industrial demand drivers. The gold-silver ratio helps identify relative value opportunities between the metals.

Conclusion: Following the Liquidity Signals

The overnight funding markets are sending clear signals that banking system liquidity has declined below comfortable levels. The Fed’s decision to end QT early, combined with increased usage of emergency lending facilities, reveals that the system requires intervention.

Reserve management purchases, quantitative easing by another name, will expand the Fed’s balance sheet, increasing money supply while gold’s supply remains fixed by geological constraints. This dynamic has consistently supported gold appreciation throughout monetary history.

The Federal Reserve didn’t end quantitative tightening because inflation was conquered or because economic conditions were ideal. They ended QT because the banking system couldn’t handle it. In this environment, where liquidity stress forces balance sheet expansion despite persistent inflation, gold occupies the ideal position.

Whether you’re establishing initial precious metals positions or expanding existing holdings, Bullion Trading LLC offers comprehensive gold and silver products backed by market expertise. From popular sovereign coins to large institutional bars, our inventory serves every investment strategy. In an environment where banking system stress forces monetary expansion despite persistent inflation, gold ensures your wealth benefits from the outcome while being protected from the risks.