Ask ten gold owners what they will hand the IRS when they sell, and most give the same answer: 28 percent. It is the figure that shows up in every forum thread and half the headlines. It is also, for a lot of people, simply wrong. The collectibles tax on gold is real, but that 28 percent number is a ceiling, not a flat toll everyone pays at the door. What you actually owe comes down to four things: how long you held the metal, what tax bracket you sit in, what you originally paid, and whether you kept any proof of it. Get those right and the bill can be far smaller than the internet promised. Get them wrong, especially the last one, and it can be a good deal worse.

Why the IRS treats your gold coins as collectibles

Gold feels like money. The IRS does not see it that way. For tax purposes, a one ounce American Gold Eagle sitting in your safe shares a category with a rare stamp, a painting, or a bottle of first growth Bordeaux. The tax code, in Section 408(m), defines collectibles to include any metal or coin, and that single classification is what pulls physical bullion out of the ordinary capital gains system that covers stocks and drops it into its own corner with a higher cap.

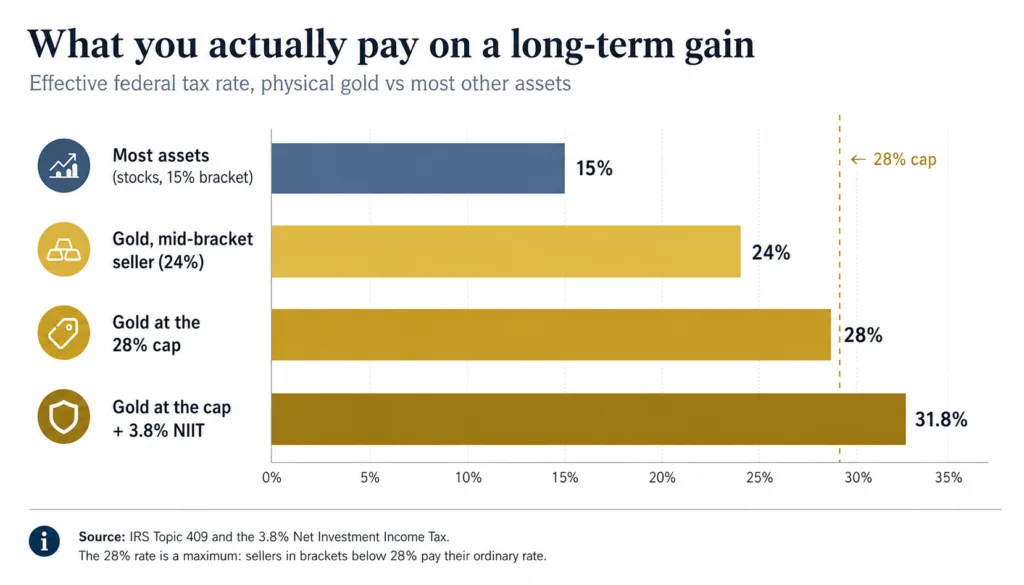

The practical effect is easy to miss. Sell a stock you have held more than a year and your long-term gain is taxed at 0, 15, or 20 percent depending on income. Gold does not get that deal. The IRS sets the maximum rate on long-term collectible gains at 28 percent, spelled out in its own guidance on capital gains and losses. That treatment covers bars, rounds, and coins, and it reaches funds that hold physical metal directly, which catches investors who assumed an ETF would shield them. It does not.

The number most people get wrong

Here is where the 28 percent myth falls apart. That rate is a maximum, and the word is doing all the work. As Kiplinger notes in its breakdown of how collectibles are taxed, the 28 percent ceiling sits above the 15 or 20 percent that applies to most other long-term gains. But a maximum is not a flat rate. If your ordinary income bracket sits below 28 percent, your collectible gain is taxed at that lower ordinary rate instead. Someone in the 12 percent bracket pays 12 percent on the gain, not 28. The 28 percent figure is the worst case for high earners, not the default for everyone.

So the honest answer to “what do I owe” is this: somewhere between your ordinary income rate and 28 percent, whichever is lower, applied to the profit. Not the sale price. The profit. People conflate the two constantly, and the gap between them is the difference between a manageable bill and a nasty surprise.

There is a second layer that can push the real cost higher for big sellers. High earners owe the Net Investment Income Tax, an extra 3.8 percent on investment income once modified adjusted gross income crosses 200,000 dollars for single filers or 250,000 for married couples filing jointly. The IRS spells out the rate and those thresholds on its Net Investment Income Tax page. Stack that surtax on top of the 28 percent cap and the effective federal rate on a large gain lands near 31.8 percent. Then add state income tax, because most states tax the gain as ordinary income no matter how the federal government classifies the asset. And the sales tax you may have paid at purchase is a separate matter from the income tax you owe at sale.

How long you held it changes everything

The entire 28 percent conversation only applies to long-term gains, meaning metal you owned for more than one year before selling. Sell inside that window and the collectibles cap does nothing for you. Short-term gains on bullion are taxed as ordinary income at your marginal rate, which currently runs as high as 37 percent. So a quick flip can be taxed harder than a patient sale, which is the opposite of what most people assume about a “collectible” penalty rate.

That gap is wide enough to change how you behave. Say you bought during a price spike, the metal ran higher, and you are tempted to lock in the win at month eleven. Holding past the one-year mark moves that gain off the ordinary income schedule and under the capped collectibles rate, which for many sellers is a meaningfully lower number. Timing a sale around the holding period is one of the few entirely legal levers you control with a calendar and some patience. For owners thinking through the mechanics of an actual sale, the question of how, where, and to whom you sell your gold matters nearly as much as the date you choose.

Cost basis is where the real money is won or lost

You owe tax on the gain, which is the sale price minus your cost basis. Simple formula, except basis trips people up, because it is not just the spot price you paid. Your basis includes the premium you paid over spot, dealer fees, and the reasonable costs of acquiring the metal. If you bought a coin carrying a healthy premium, that premium is part of your basis and it lowers your taxable gain. Every dollar of documented cost is a dollar the IRS cannot tax, so the premium you paid is worth remembering rather than writing off.

Now the part that quietly costs people thousands. If you cannot prove what you paid, the IRS can treat your cost basis as zero, which turns the entire sale price into taxable gain. Picture selling 30,000 dollars of gold you genuinely bought for 22,000, then losing the receipt. Without records, you may be taxed as though all 30,000 were profit. Keep your invoices, your wire confirmations, your dealer statements. A shoebox of receipts is the cheapest tax planning you will ever do.

Which pieces you sell also matters when your stack was built over years at different prices. The default is first in, first out, which assumes you sold your oldest coins first. In a rising market those usually carry the lowest basis, so it tends to produce the largest taxable gain. Use specific identification instead, document which coins left your hands, and selling your higher-basis pieces first can shrink the gain. It takes recordkeeping, but it is legitimate.

Inherited and gifted metal follow different rules, and the contrast is stark enough to plan around. Gold you inherit gets a stepped-up basis, meaning your basis resets to the fair market value on the date the previous owner died. Inherit coins worth 50,000 dollars and sell them soon after for 51,000, and you are taxed on a 1,000 dollar gain, not on decades of appreciation. Gifted gold works the opposite way. It carries over the giver’s original basis. If an aunt paid 400 dollars for a coin and gives it to you when it is worth 2,400, your basis for figuring gain is 400, and the built-in profit comes with it. Same coin, very different tax outcome, depending on how it reached you.

Reporting is not the same as owing

One of the most stubborn myths in the bullion world is that if no tax form gets filed, no tax is due. The two questions are separate. A dealer files a Form 1099-B on a sale only when the metal matches a form traded under a futures contract the Commodity Futures Trading Commission has approved, and the amount meets that contract’s minimum size, a framework the IRS restated in its 2025 correction to the Form 1099-B instructions. There is no official coin-by-coin list. Industry guidance reads that rule to mean coins like the Krugerrand, the Maple Leaf, and the Mexican Onza become reportable at 25 or more, and silver at 1,000 troy ounces, while American Gold Eagles and fractional coins are generally not reported at all. This is one practical reason the choice between an American Gold Eagle and a Canadian Maple Leaf carries consequences beyond design and premium.

Cash has its own rule. If a dealer receives more than 10,000 dollars in cash in a single transaction or in related transactions, the dealer must file a Form 8300, according to the IRS guidance on reporting cash payments over 10,000 dollars. That rule targets cash structuring, but it surprises people who assumed cash kept a sale invisible. Anyone weighing where to unload coins should understand these mechanics before walking in, which is part of knowing whether it is safe to sell gold coins to a dealer in the first place.

Here is the trap worth repeating. The absence of a 1099-B does not make your gain tax free. If you sold gold at a profit, you owe capital gains tax whether or not any form reached the IRS. Reporting determines what the agency sees automatically. It does not determine what you legally owe. The honest path is to track your own gains and report them on Schedule D, where the 28% Rate Gain Worksheet in the Schedule D instructions is exactly where collectible gains get sorted out.

Legal ways to soften the hit

None of this means you are stuck paying the maximum. The holding period is the simplest tool, since crossing one year shifts you from ordinary rates to the capped collectibles rate. Losses are another: if you sold one position at a loss the same year you booked a gain, the loss offsets the gain. Tax-loss harvesting is not just a stock market trick.

For metal you have not bought yet, the structure you buy it in changes the picture entirely. Holding bullion inside a self-directed retirement account keeps gains sheltered while the metal stays in the account, so you are not settling up with the collectibles rate every time you reposition. A precious metals IRA is not right for everyone, and the custody rules are worth studying, but for long-term holders it sidesteps the annual friction a taxable account creates. One option is now closed: the like-kind exchange that once let investors swap one form of bullion for another without tax was limited to real property by the 2017 tax law, so it no longer applies to coins and bars.

Estate planning deserves a mention too, precisely because of that stepped-up basis. Metal held until death and passed to heirs erases the embedded gain for them, which is one reason some long-term owners are in no hurry to sell. Charitable giving can also defer the gain, though bullion carries a catch. Because metal is tangible personal property that a charity will usually just sell, your deduction is generally limited to what you paid, not the higher market value, under the unrelated-use rule. You sidestep the capital gain but cannot write off the appreciation. These are not loopholes. They are the ordinary rules, used on purpose.

The bottom line on what you actually owe

The 28 percent collectibles tax is the headline, but it is rarely the whole story and almost never the full bill for a typical seller. It applies only to long-term gains, it works as a ceiling rather than a flat rate, and it lands on your profit, not your proceeds. The investors who keep the most are not chasing exotic strategies. They hold past a year, keep every receipt, know which coins trigger a dealer’s paperwork, and report their gains honestly instead of betting on a missing form. Before you sell, run your numbers against your bracket and basis, and when the amounts are large, put a tax professional between you and the IRS. The metal did its job. Make sure the paperwork does too.