Pick up any newspaper and the headline is the same: the consumer is cracking. That is true, but it is only half the picture. The other half rarely makes the front page, and it matters a great deal more for anyone who owns hard assets. The truth is that the United States no longer has one consumer. It has two, and they are living in economies that barely resemble each other. This is what economists now call the K-shaped economy, and once you start looking for it, you see it everywhere, including in places you would never think to check, like the order books of gold jewelry manufacturers.

Two Americas, one set of confusing data

On the bottom arm of the K, lower income households are clearly struggling. Higher fuel costs, soaring insurance premiums, the return of student loan payments, and years of cumulative inflation have ground down what used to be discretionary budgets. You do not have to take my word for it. The companies that sell to these households are saying it out loud. Kraft Heinz described lower income shoppers as “literally running out of money at the end of the month,” dipping into savings just to get by, a warning echoed almost word for word by the chief executives of McDonald’s and Whirlpool and rounded up in this Yahoo Finance report. Whirlpool’s chief executive went further still, telling investors that parts of consumer spending today look uncomfortably like the 2008 financial crisis, a comparison spelled out in this 24/7 Wall St. report. Planet Fitness, a brand built almost entirely on the value conscious customer, had one of its worst trading days on record after it flagged weaker than expected member growth and quietly paused a planned Black Card price increase. Even McDonald’s, the supposed recession hedge of the fast food world, has reported the same softness among low income diners.

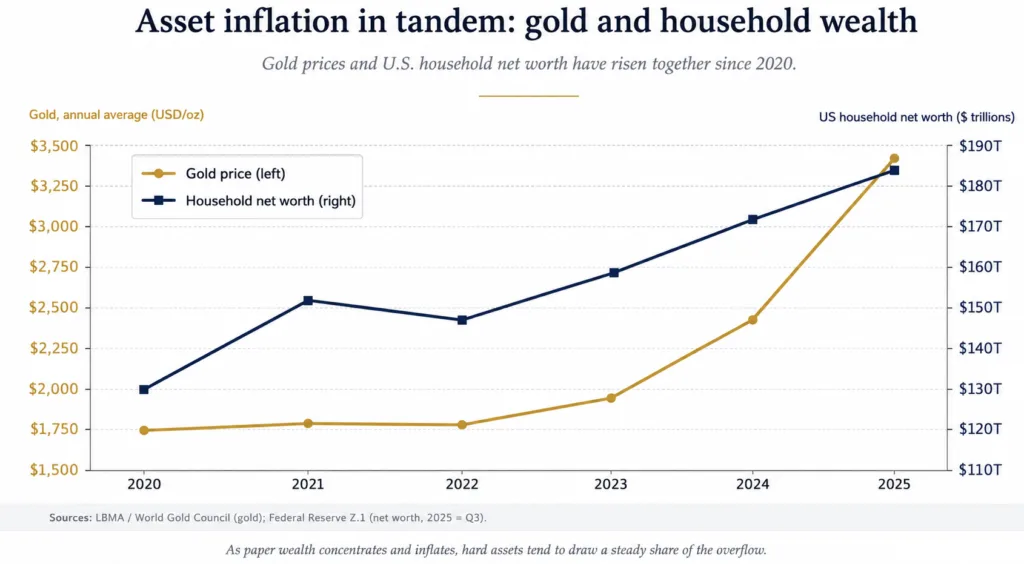

That is one America. Now look at the other one. Over roughly the past year and a half, household net worth in the United States has surged. Federal Reserve figures put it at a record $181.6 trillion in the third quarter of 2025, up from $175.6 trillion just one quarter earlier, with the entire gain driven by rising equity values. You can see the underlying numbers in the Fed’s quarterly Financial Accounts data, which show that direct and indirect holdings of corporate equity added about $5.6 trillion in that single quarter on the back of an artificial intelligence boom, while real estate actually slipped slightly. The pressure squeezing one group is, almost in the same breath, enriching the other.

Where the money actually concentrates

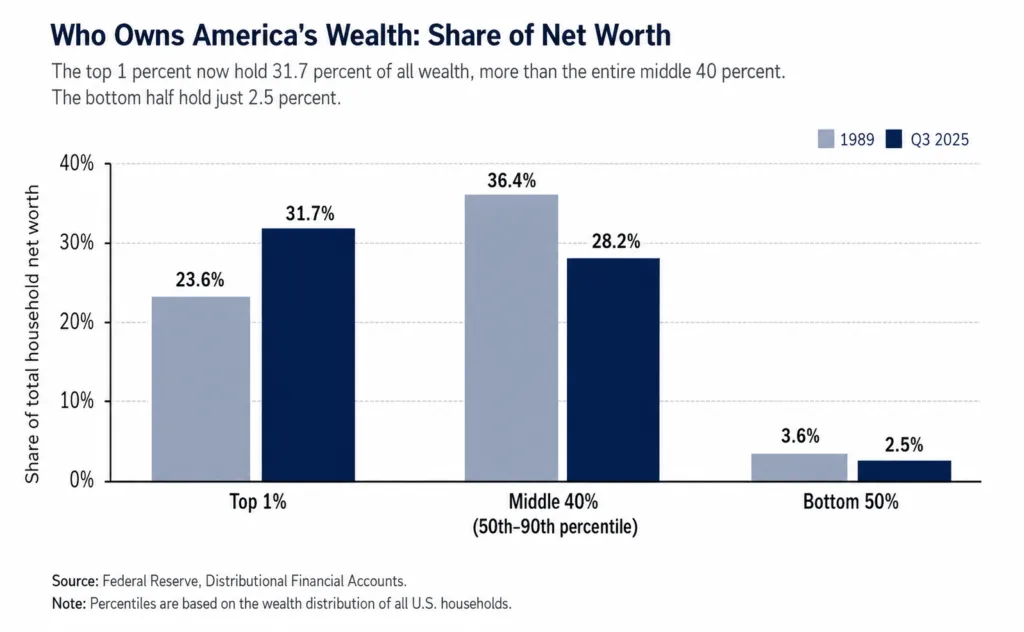

This is the part most coverage glosses over. The wealth is not spread evenly across that record net worth figure. It is piling up at the very top. According to the Fed’s Distributional Financial Accounts, the top 1 percent of households held 31.7 percent of all U.S. net worth in the third quarter of 2025, while the bottom half of all households held just 2.5 percent. Put differently, the wealthiest 1 percent now own more than the entire middle 40 percent of the country combined, and roughly thirteen times what the bottom half holds altogether.

The flow into that top tier is staggering. UBS reported that the United States minted more than 1,000 new dollar millionaires every single day in 2024, some 379,000 over the year, more than half of all the new millionaires created on the planet. The full breakdown sits in the UBS Global Wealth Report. When the S&P 500 climbs more than 20 percent in a year, the people who already own equities get a raise that no paycheck could ever match. The people who do not own equities get nothing. That is the engine of the K, and it has been running hot.

Why the spending data looks contradictory

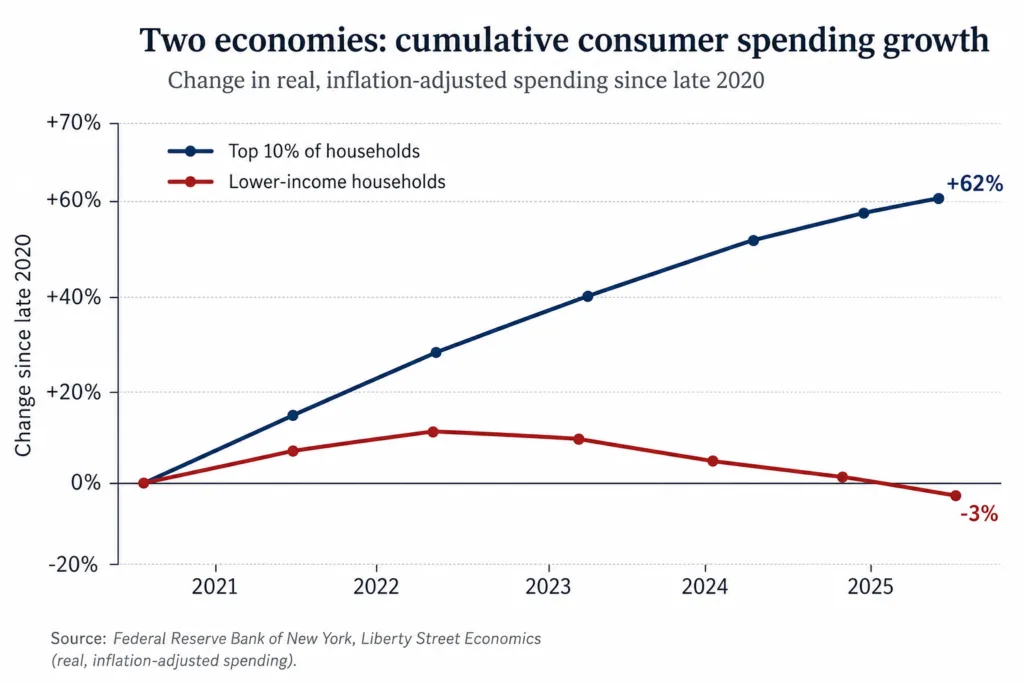

This split explains a puzzle that has frustrated economists for two years. How can retail sales hold up while half the country says it cannot afford groceries? Because the spending is coming from the top of the K. Research from the New York Fed’s Liberty Street Economics team shows the highest income households now drive a remarkable share of total consumption, and that spending by the top 10 percent grew far faster than any other group through 2025. By some measures, the top 10 percent alone account for close to half of all consumer spending in the country.

That money is not sitting quietly in brokerage statements. It shows up in restaurant reservations, in premium travel, in luxury goods, in second homes, and in experiences. The affluent consumer keeps spending as if no slowdown exists, because for them it does not. Meanwhile the household down the road is deciding between the electric bill and a full tank of gas. Both stories are true at the same time, which is exactly why the aggregate data reads like a contradiction. The strain on the lower half is real, and it ties directly into a broader debt picture I have written about before in this look at the U.S. household debt crisis.

What I am seeing in the gold market

Here is where it gets interesting to me personally, and I want to be specific about what I mean. I am not talking about the retail bullion investor buying a tube of coins. I am talking about wholesale customers who manufacture and sell finished gold jewelry and gold products to the public. These are businesses whose order volume tracks real consumer demand on the ground, well before it shows up in any government release.

And many of them are buying more gold, not less.

I cannot tell you with certainty what is driving that, and I am not going to pretend otherwise. Part of it may be a substitution effect. Diamond prices have been falling hard, slumping by as much as a quarter in 2025 as lab grown stones flooded the market and crushed natural diamond values to their lowest level this century, a collapse documented in this Money report. Gold, over the same stretch, has done the opposite and kept climbing. When the gem in the ring keeps losing value and the metal around it keeps gaining, it is not hard to see why a manufacturer would lean toward gold. If you want the practical distinction between the two kinds of gold at play here, this piece on bullion gold versus jewelry gold lays it out.

Part of it may be something simpler: consumers, or at least the half of them with money, are still spending despite all the talk of a downturn. And part of it is probably both at once. What I can say plainly is that wholesale demand for gold from our manufacturing customers has stayed strong. To me, that hints there may be more real consumer demand bubbling beneath the surface than most commentators currently give credit for. The order book does not lie, even when the headlines do.

Why concentration tends to favor hard assets

For a gold investor, this is not just an interesting macro footnote. It speaks directly to the conditions in which gold has historically done its best work. Gold tends to perform well in periods when wealth concentration is rising, when asset inflation is outrunning wage growth, and when confidence in the financial system starts to wobble at the edges. Right now all three boxes are getting ticked at the same time.

Think about the mechanism. When a small group controls an ever larger slice of the wealth, and that group keeps watching its paper assets balloon, a portion of that money looks for a home outside the same financial system that created it. Some of it goes into real estate. Some into art and collectibles. And a steady share, historically, has gone into gold, which answers to no central bank and carries no counterparty. That instinct is visible in the institutional flows too. You can see it in who has been accumulating the metal lately in this breakdown of who is buying all the gold, and in the broader investment surge that pushed annual gold demand to a record $555 billion year.

The story underneath the story

So the biggest takeaway here may not be where consumers are spending their money. It may be who is doing the spending in the first place. Consumption is becoming concentrated among the people who own financial assets, while a large share of the country keeps treading water or sliding backward. That is a structural shift, not a passing mood, and it does not unwind quickly.

Now layer in the other forces already in motion. Government deficits keep widening. Monetary expansion has been the default response to every shock for fifteen years and shows little sign of reversing. When wealth keeps concentrating at the top while the public balance sheet keeps deteriorating, history offers a fairly consistent lesson. Sooner or later, hard assets start attracting more attention, not less. They become the thing people reach for when they no longer fully trust the system minting all that paper wealth.

I am not predicting a crash, and I am not telling you the consumer is secretly fine. Both halves of the K are real. The lower half is genuinely hurting, and pretending otherwise would be dishonest. But the upper half is spending and accumulating at a pace that the gloomier headlines never mention, and a slice of that accumulation has a way of finding its way into metal. The wholesale demand I am watching from manufacturers may be one of the earliest, quietest signals of that. The retail investor who is paying attention to the same forces, asset inflation, wealth concentration, and a financial system running on borrowed confidence, may want to make sure they are positioned for the side of the K that keeps pulling away. Gold has spent a very long time being the asset people turn to when the rest of the picture stops adding up.