If you stack gold and haven’t looked at platinum in a while, the numbers deserve ten minutes of your attention. Platinum was the best performing major precious metal of 2025, rising about 142% on the LBMA afternoon price, from $921 an ounce on January 2 to $2,226 by December 30. Gold gained 65% over the same year, which would have been the story of the decade if platinum hadn’t buried it. And yet the whole platinum vs gold investment question turns on one odd fact: after all that, an ounce of platinum still costs less than 40 cents for every dollar of gold. On July 1, 2026, the LBMA priced gold at $4,089 and platinum at $1,569.

For most of modern trading history, platinum was the more expensive metal. So either the market is offering gold stackers a rare discount, or the old relationship is simply dead. I think the honest answer sits in between, and it points to a specific portfolio decision rather than a price prediction. Here is the math, along with the parts the platinum promoters tend to skip.

How cheap is platinum, really?

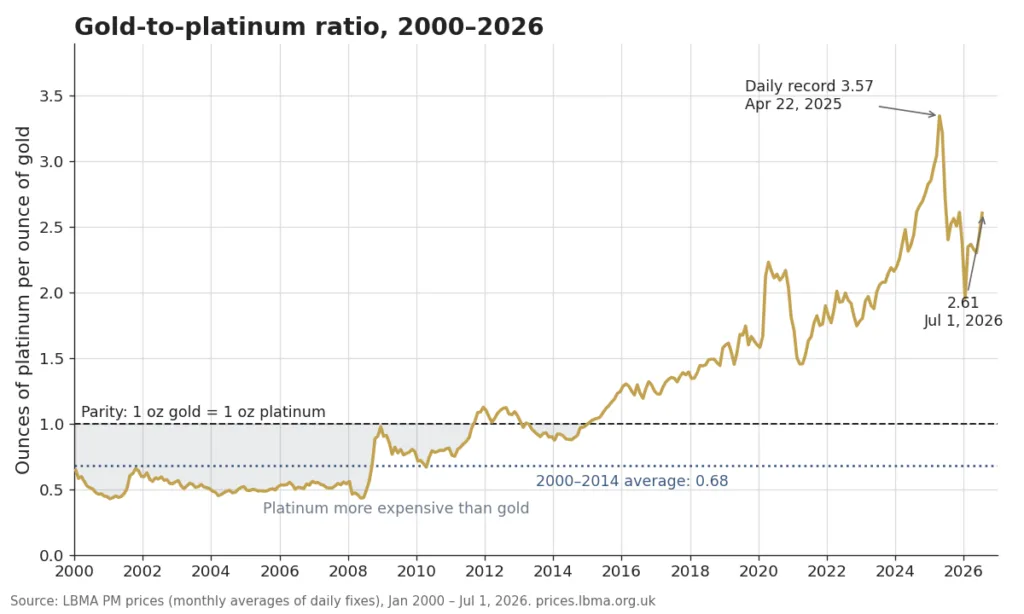

The gold-to-platinum ratio is just the gold price divided by the platinum price. On July 1, 2026 it stood at 2.61, meaning one ounce of gold buys 2.61 ounces of platinum. To see why that number is strange, run it backward through the LBMA record. From 1990 through 2014, platinum closed above gold on 92% of trading days. Between 2000 and 2008 the ratio averaged 0.53, so gold typically cost about half of what platinum did. At platinum’s old peak on March 4, 2008, an ounce of it ($2,273) bought 2.3 ounces of gold ($985). The metals have fully swapped places.

January 14, 2015 was the last day platinum closed above gold, and the gap has mostly widened since. The ratio set its record of 3.57 on April 22, 2025, right before platinum’s rally began in earnest. Even now, after platinum more than doubled, the ratio sits higher than its average in any calendar year before 2024. By this one measure, platinum remains cheaper against gold than at almost any point in the past century of records.

A warning before you treat that as a buy signal. Ratios revert to a mean only if the world that produced the mean still exists. Platinum’s old premium rested on a demand base that partly collapsed, and “historically cheap” stayed cheap for an entire decade. The ratio argument tells you platinum is unloved. It cannot tell you when, or whether, that changes.

Why the two metals stopped moving together

Gold and platinum diverged because they answer different questions. Gold is a monetary asset. Central banks bought 863 tonnes of it in 2025, and while that was 21% below 2024, it still ran nearly double the 473-tonne annual average of 2010 to 2021, according to the World Gold Council’s full-year 2025 demand data. No central bank runs a platinum reserve program. Nobody official stands under the platinum price with a bid.

Platinum, by contrast, is an industrial metal that happens to be precious. Autocatalysts account for roughly 39% of its projected 2026 demand, with jewellery and other industrial uses making up most of the rest. That exposure turned toxic on September 18, 2015, when the EPA issued Volkswagen its notice of violation for diesel emissions cheating. Diesel engines, whose catalysts are platinum-heavy, ran about half of new car sales in Western Europe in 2015 and fell to an 11.9% share of EU registrations by 2024, per ACEA data. Platinum lost its marginal buyer in the same decade gold found its biggest one. If you want the longer version of how platinum and palladium ended up as the market’s afterthoughts, I covered it in Platinum and Palladium: The Forgotten Precious Metals.

What changed for 2026: deficits and a shrinking cushion

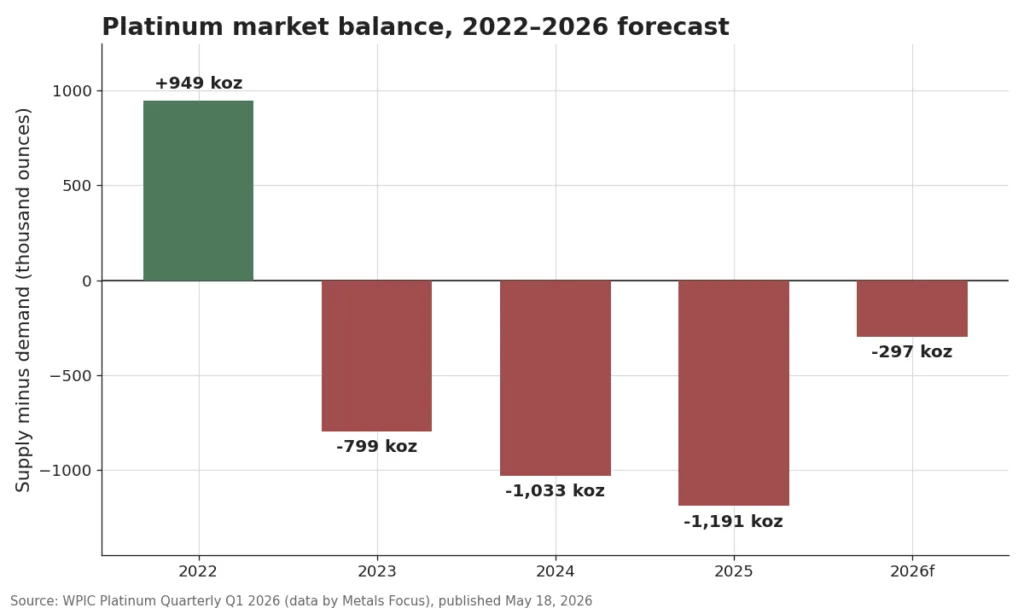

The bull case rests on supply and demand data from the World Platinum Investment Council, whose Platinum Quarterly (published May 18, 2026, with figures compiled independently by Metals Focus) shows a market that has now run short of metal three years straight: a deficit of 799,000 ounces in 2023, 1,033,000 in 2024, and 1,191,000 in 2025, the deepest in the data series. For 2026 the WPIC forecasts a fourth consecutive deficit of 297,000 ounces, revised up from the 240,000 it projected in November 2025.

Those deficits come out of a stockpile that is visibly draining. WPIC puts above-ground stocks at 2.04 million ounces at the end of 2025, down from 4.27 million at the end of 2023, and projects 1.75 million by the end of 2026. That is less than three months of global demand. Supply can’t respond quickly: 72% of refined mine production comes from South Africa, where output is forecast flat for 2026 despite prices having doubled, and Ivanhoe’s Platreef is the first new greenfield mine commissioned there since 2019. The only supply segment growing is recycling, up a forecast 9%.

Demand is rotating rather than booming. WPIC forecasts total 2026 demand down 9%, mostly because the ETF and exchange-warehouse buying that piled in during 2025 is unwinding. Underneath that, physical bar and coin demand is forecast up 27%, and industrial demand up 9%, with electronics up 20% on AI data center buildout. That last thread, platinum in hard drives and semiconductors, is the quiet one I wrote about in The Hidden Conductors. As for hydrogen, keep your expectations modest: WPIC’s stationary hydrogen category has grown from 13,000 ounces in 2022 to a forecast 69,000 in 2026, real growth but still under 1% of total demand. Anyone selling you platinum “because hydrogen” is early by years.

Two honest caveats. First, these are forecasts, revised quarterly, and the 2026 number has already moved once. Second, the first quarter of 2026 actually posted a 268,000-ounce surplus, the first in six quarters, as ETF holders took profits and South African mines had an unusually strong quarter. The deficit story is genuine, but it arrives lumpy.

The case against: what gold does that platinum can’t

The downside is where platinum differs most from what a gold stacker is used to, so this section deserves more of your attention than the bull case did.

Start with volatility, and you don’t need 2008 to see it (though 2008 is instructive: platinum fell from $2,273 in March to $763 by late October, a 66% collapse in eight months). Look at the last five. Platinum set its all-time LBMA record of $2,811 on January 26, 2026, then gave back 44% to reach $1,569 by July 1, as the Iran conflict pushed energy prices and rate expectations higher and investors dumped ETF holdings. Gold fell too over that stretch, but by 24% from its own January peak, and it found buyers faster. When macro fear turns into a liquidity scramble, platinum trades like a cyclical commodity, not a safe haven.

Then there’s the stagnation risk, which I’d argue is the scarier one. From 2021 through 2024, platinum went nowhere, trading between $831 and $1,294 for four full years while gold climbed from about $1,943 to $2,609. Deficits ran through most of that period too. A supply shortfall is not a fuse with a known length; the market covered it by draining stockpiles, and prices only moved when investors finally noticed.

Finally, the practical frictions. The platinum market clears around 8 million ounces a year, roughly 250 tonnes, against gold demand of several thousand tonnes, so fewer dealers make tight two-way markets in it. Expect the gap between a dealer’s sell price and buyback offer on platinum coins to run wider than on their gold equivalents, and expect fewer product choices in stock at any given moment.

Platinum vs gold investment in physical form: products, premiums, IRA rules

If you decide the trade-off suits you, the physical side works much like gold with fewer menu options. The flagship coin is the American Platinum Eagle, minted since 1997 with a $100 face value, the highest denomination ever struck on a U.S. coin. Like the Royal Canadian Mint’s Platinum Maple Leaf, it is struck in .9995 fine platinum, and refiners such as Valcambi and PAMP produce 1 oz platinum bars at the same purity that typically carry lower premiums than sovereign coins. I walked through the bar side in Buying Valcambi Bars Online.

On cost: dealer listings in mid-2026 have generally shown 1 oz Platinum Eagles at premiums around 5 to 8% over spot, against roughly 3 to 7% for 1 oz Gold Eagles, with bars cheaper than coins in both metals. Premiums float with supply, so check live prices rather than trusting any article’s snapshot, including this one.

For retirement accounts, platinum is IRA-eligible under the same section of the tax code as gold, with a stricter purity bar. IRC 408(m)(3) admits platinum coins described in 31 U.S.C. 5112(k), which covers the Platinum Eagle, plus platinum bullion meeting the exchange minimum fineness of .9995 (gold bars get in at .995). The metal must sit with an IRS-approved trustee, not in your safe. The custodian mechanics, fees, and pitfalls are the same ones covered in the Precious Metals IRA guide.

So is platinum a good investment for 2026?

Here’s where I land after staring at this data for a week. Add platinum if all of the following are true: you already hold a gold core you’re not touching, your horizon is five years or longer, you actually believe the WPIC deficit-and-drawdown story, and a 40% drawdown in six months (which just happened) would leave you bored rather than panicked. In that case platinum is a reasonable satellite position. Some investors size a satellite like this at 5 to 15% of their total metals allocation; treat that as an illustration of “small,” not a prescription, because the right number depends on your income, horizon, and nerves.

Stick with gold alone if your metals exist as insurance: crisis liquidity, a hedge against currency debasement, something you might need to sell quickly at a fair price on a bad day. Platinum fails that job description on every line. Nobody official stands ready to buy it, spreads run wider, and history says it falls hardest exactly when fear peaks. Platinum was never built for that job.

The ratio chart makes the anomaly case in one glance, and the 2026 tape makes the risk case just as fast. Both are telling the truth. Platinum at 38 cents on the gold dollar is a real oddity backed by three years of real deficits, and it is also the most volatile way to own a precious metal. Buy the oddity with money that can wait, keep the insurance in gold, and don’t let anyone convince you the two metals are interchangeable. They stopped being that in 2015.