When gold prices break records, most investors rush to two familiar places. They buy physical bullion, or they buy mining stocks. Both have their merits, and both have well-known drawbacks. A third category sits quietly between them, generating cash from gold without ever pulling rock out of the ground. Gold royalty and streaming companies finance mines in exchange for a slice of future production or revenue, and over the past two decades they have outperformed nearly every other way to play the metal. Understanding how they actually work takes a little patience, but the payoff is a much clearer view of how serious institutional capital approaches the precious metals sector.

Where the model actually came from

Both businesses have surprisingly short histories. Pierre Lassonde and Seymour Schulich launched Franco-Nevada Mining Corporation in Toronto in 1983. Their thesis was simple. The oil and gas industry had used royalty structures for decades to fund exploration without owning wells. Nobody had built a serious version of this for gold. In 1986 they spent half the company’s treasury, roughly $2 million, to buy a 4 percent revenue royalty on a small Nevada property called Goldstrike. American Barrick, later Barrick Gold, then bought the deposit and drilled into what turned out to be one of the largest gold finds in North American history, a 50 million ounce orebody on the Carlin Trend. The original Franco-Nevada provided a 36 percent annualized rate of return from inception to February 2002, when it was acquired by Newmont Mining for US$3.2 billion, as documented on the company’s own history page. Newmont spun the royalty book back out through a 2007 IPO that raised CA$1.1 billion, the largest mining flotation in North American history at the time. It remains one of the great mining finance stories of the twentieth century, and it created the template every royalty firm has copied since.

Streaming came later, and from a different city. On October 15, 2004 Ian Telfer and Frank Giustra incorporated Silver Wheaton in Vancouver, structured around an idea Telfer had been refining for years. Instead of taking a percentage of mine revenue, Silver Wheaton paid Wheaton River Minerals (later folded into Goldcorp) total upfront consideration of about Cdn$262 million, broken into US$36.7 million in cash and 540 million Silver Wheaton shares, for the right to purchase all silver produced as a byproduct from the Luismin operations in Mexico at a fixed ongoing payment capped at the lesser of US$3.90 per ounce and prevailing market. The deal closed when silver was trading near seven dollars. Goldcorp got a tax-advantaged financing package, and Silver Wheaton locked in a margin that widened with every price tick higher. The company rebranded as Wheaton Precious Metals in 2017 after expanding into gold, palladium, and cobalt. It reported record annual revenue of $2.3 billion in 2025 on production of 689,864 gold equivalent ounces.

How a royalty differs from a stream

The two structures look similar at first glance but behave quite differently in practice. A royalty is a contractual right to receive a percentage of revenue or production from a mine. The most common version is the net smelter return, or NSR, where the holder collects a fixed percentage of gross sales minus the costs of transportation, smelting, and refining. The simpler cousin is the gross revenue royalty, or GRR, which takes a slice off the top with minimal deductions. The Corporate Finance Institute walks through the mechanics in detail, but the point worth remembering is that royalties tend to be tied to a property for life and require little or no further capital from the holder once they are negotiated.

A stream is different in two important ways. First, the streaming company writes a large check upfront, often covering 30 to 50 percent of mine construction costs. Second, instead of cash, the streamer receives physical metal at a deeply discounted price agreed in advance, sometimes a small fraction of the prevailing spot price. The Investing News Network published an investor’s guide to royalties and streams that walks through the typical contract clauses. Royalties usually attach to a property early in the exploration stage, before serious drilling begins. Streams come later, during construction or expansion, when capital needs are highest and conventional lenders are most cautious.

The shared genius of both models is the cost structure. A royalty or streaming company carries no labor force, no fuel bill, no environmental remediation liability, and no direct exposure to grade decline. The miner absorbs all of that. If a project’s all-in sustaining cost rises from $900 an ounce to $1,400, the streamer or royalty holder feels nothing. They keep collecting the same percentage of production, or the same fixed payment per ounce. When gold rises, margins expand almost instantly. When gold falls, the contractually low cost basis still leaves room to profit. That is the engine.

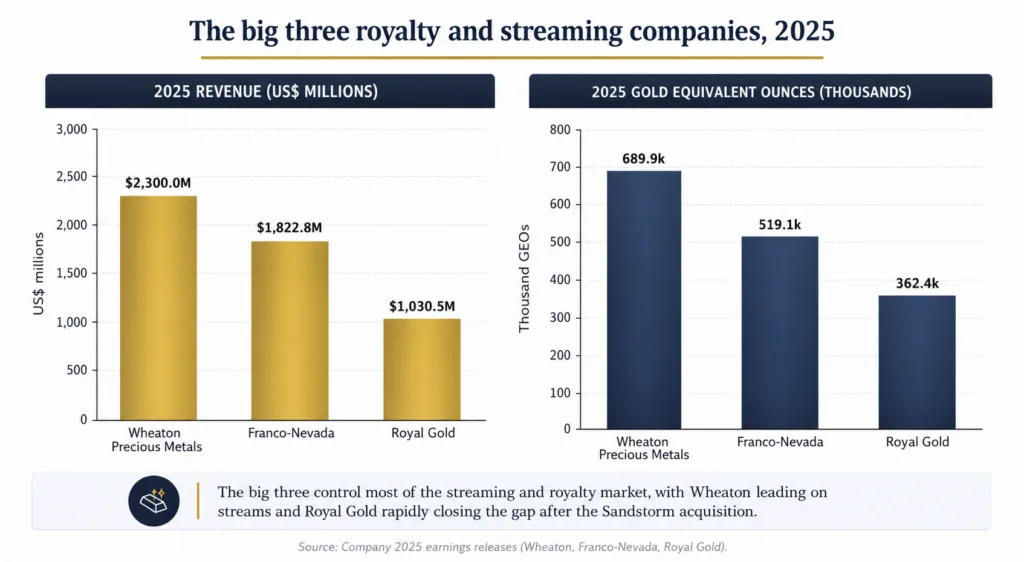

The big three and where they sit today

The sector consolidated rapidly over the last decade and three firms now dominate. Franco-Nevada is the largest by market capitalization, sitting near CA$35 billion as of February 2026 according to comparative data published by the Canadian Mining Report. Its portfolio includes more than 430 assets across the Americas, Africa, and Australia, with gold contributing roughly three quarters of revenue and the rest split between silver, platinum group metals, and a legacy oil and gas book. Even Franco-Nevada is not bulletproof. On November 28, 2023 the Panamanian Supreme Court ruled the Cobre Panama mining contract unconstitutional, forcing operator First Quantum to halt production. That single asset had been contributing close to 20 percent of Franco-Nevada’s revenue. The company took a roughly $1.1 billion impairment charge on the stream and yet still raised its dividend for the seventeenth straight year, ending 2023 with $1.4 billion in cash and no debt, as disclosed in its 2024 dividend announcement. That kind of balance sheet is rare in any sector.

Wheaton Precious Metals sits second at roughly CA$28 billion. Its model differs from Franco-Nevada’s in that it leans heavily on streams rather than royalties, which means bigger upfront commitments and a smaller but more concentrated asset list. The company’s 689,864 GEOs in 2025 came in above the 600,000 to 670,000 ounce guidance range it had set at the start of the year, helped by stronger output at Salobo, Peñasquito, and Constancia, and by fixed per-ounce production payments accounting for around 80 percent of revenue in the fourth quarter. That fixed cost base is what makes streams so attractive when bullion prices rise sharply.

Royal Gold reshaped the third spot in July 2025 when it announced a $3.5 billion all-share takeover of Sandstorm Gold Royalties, along with a $196 million cash deal for Horizon Copper. The combined entity, detailed in the official transaction press release, will hold 393 streams and royalties, with 80 already producing cash and 47 in active development. No single asset will represent more than 13 percent of net asset value, and gold will provide about 75 percent of revenue. The market reaction was mixed because Sandstorm shareholders gave up an independent vehicle, but the combined balance sheet now rivals Wheaton’s in flexibility, and the deal cemented Royal Gold’s claim to the third seat at the table.

Why investors keep coming back to this corner of the market

The pitch is straightforward. You get leveraged exposure to the gold price without taking on the operational dysfunction that has plagued large miners for decades. Cost inflation, labor strikes, country risk, capital overruns, and reserve depletion all eat into the earnings of a Newmont or a Barrick. A royalty or streaming firm sidesteps most of it. Operating margins routinely run above 80 percent of revenue, a figure that an actual mine operator would find absurd. That is why a piece of paper signed in 1986 by two Toronto entrepreneurs ended up outperforming the gold price itself for two consecutive decades.

Royalty stocks behave more like high-margin financial firms than miners. They tend to pay growing dividends, carry low debt, and trade at richer multiples than producers. Other paper exposures to the metal, like COMEX gold futures contracts, offer pure price exposure but no cash flow and require constant rolling. A royalty share generates dividends backed by actual mine output, with no expiration date. The compounding effect over time has been significant. The same logic that pulls sovereign wealth funds into bullion drives some of those institutions toward royalty equities as a complement, not a substitute.

There are still risks worth respecting. Royalty and streaming firms depend on the operators they finance. If a mine shuts down for political reasons, as Cobre Panama did, or for permitting issues, the revenue stops cold. Concentration is a real problem for smaller players. The bigger firms manage this through diversification across geographies and metals, which is why Royal Gold’s Sandstorm deal carried such strategic weight. Investors should also remember that a streaming or royalty share does not entitle anyone to physical metal. The product is cash flow, paid in dollars, and the underlying gold gets sold at market by the operator. For physical exposure, holding allocated bullion is still the only honest answer, and the difference between allocated and unallocated gold storage is something every serious stacker should understand before mixing the two approaches in a single portfolio.

How to read the sector over the next decade

The next ten years will hinge on a few things, and they are all connected. New mine financing is getting harder. Banks have tightened lending standards for resource projects, equity raises in junior gold are punishing, and government scrutiny of mine permits has intensified everywhere from Latin America to Eastern Europe. That creates a structural opening for streaming and royalty capital. Every dollar of bank credit that disappears from the mining sector is a dollar that a Wheaton or a Royal Gold can place at favorable terms. Whether they price those terms aggressively enough to maintain their historical returns is the real test.

The other variable is the gold price itself. If bullion stays elevated, royalty holders will collect bigger checks, but operators will be less desperate to sell future production cheaply. Negotiating leverage shifts both ways depending on where the market sits. The 2025 cycle saw record metals revenue across all three majors, which is what you would expect in the middle of a bull run. What separates a good royalty company from a great one is the discipline to walk away from bad deals when capital is abundant, and the willingness to write large checks when nobody else will. The history of Franco-Nevada and Wheaton is mostly a history of those judgment calls. Sometimes spectacularly right, occasionally wrong, but rarely boring.

For investors trying to size their precious metals allocation overall, the question is one of fit and conviction. There is a useful perspective on how much gold makes sense in a balanced portfolio in this primer on the ideal amount of gold to keep in your investment portfolio. Treat a royalty position as equity exposure to gold, not as a substitute for physical holdings. The two assets serve different jobs. Physical metal hedges currency debasement and counterparty failure. A royalty share captures the operating leverage that comes with rising prices and growing production. Owning both, in proportions that match your time horizon, has historically been the cleanest way to participate in a gold bull market.

Conclusion

Royalty and streaming companies will not replace a physical bullion allocation, and they are not supposed to. What they offer is a way to participate in the cash flows that gold generates as it moves from rock to refinery, with cost structures that look more like an insurance company than a mine. The financial mechanics reward patience, discipline, and a long memory for which contracts paid off and which did not. For anyone trying to understand how serious capital actually approaches the precious metals sector in 2026, learning how Pierre Lassonde priced a 4 percent royalty on Goldstrike in 1986 is still one of the best places to start.