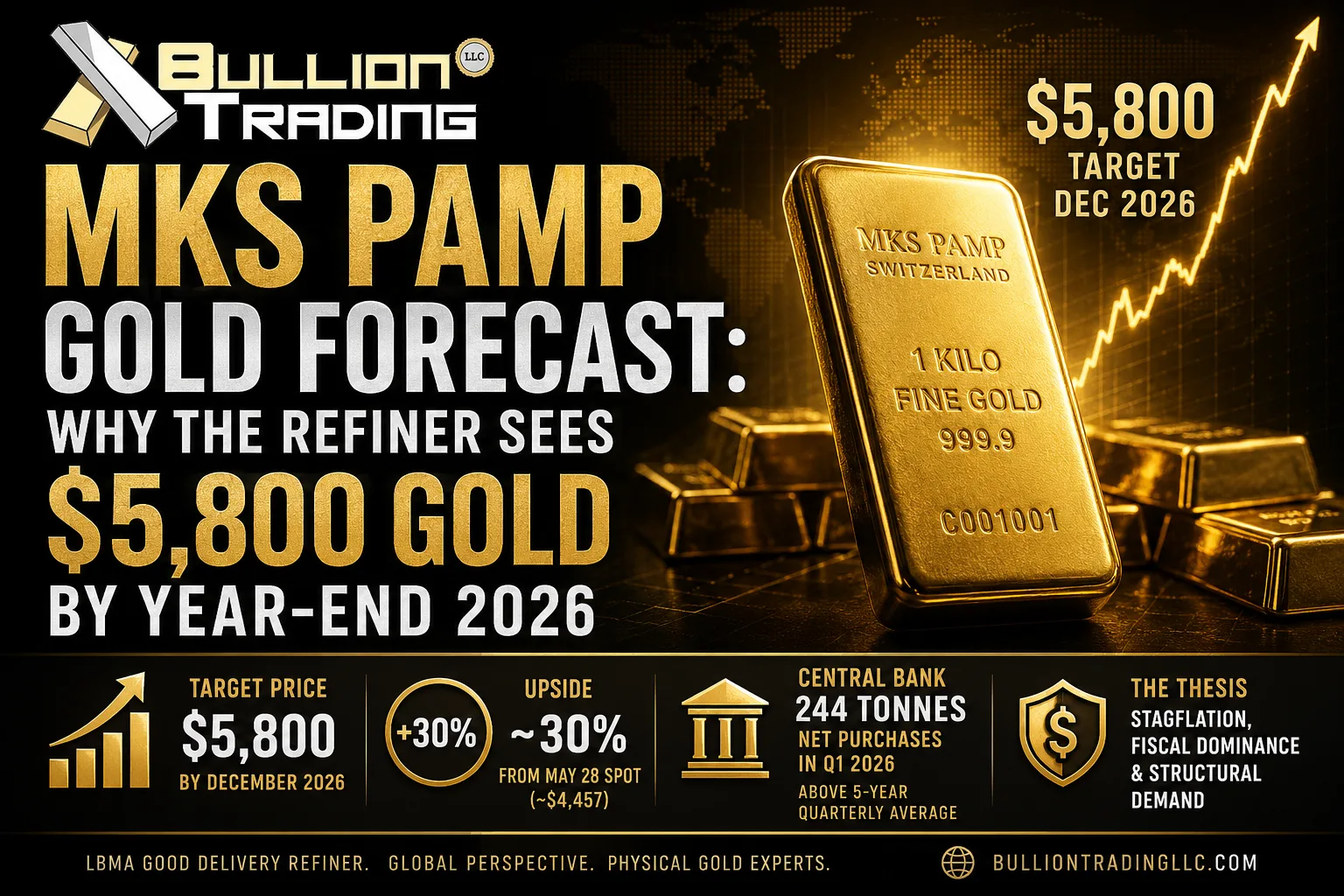

The MKS PAMP gold forecast for late 2026 is the most aggressive call coming out of any LBMA Good Delivery refiner this year, and it is worth taking seriously for one specific reason. MKS PAMP does not get paid to be loud. The Geneva-based firm refines the kilo bars that move between London, Zurich, and Shanghai vaults, and the people who run its research desk spend their days watching where the physical metal actually goes. When Nicky Shiels, the firm’s Head of Research and Metals Strategy, told Kitco in mid-May that gold would print a fresh all-time high near $5,800 an ounce by December, the call landed harder than a similar number from a sell-side equity strategist would have.

That call did not arrive in a vacuum. It is the top end of a 2026 forecast band the firm published in its annual GeoMacro outlook, and it rests on a single thesis the desk has been refining since the Iran conflict scrambled the currency trade earlier in the year. The thesis has a name. It is stagflation, the same disease that gutted American portfolios in the 1970s, and Shiels argues it is back whether the Federal Reserve admits it or not.

The number nobody on Wall Street is matching

The full MKS PAMP 2026 Precious Metals Outlook, shared in detail with deVere Insights, lays out an average gold price of $4,500 an ounce for the year inside a wide trading range of $3,750 to $5,400. The $5,800 figure sits above the range as a spike target, the level Shiels expects gold to touch in the second half of the year once macro reality catches up to the bond market. From the May 28 spot price of roughly $4,457, that is a 30 percent move in seven months.

The interesting part is not the absolute number. It is the spread between the MKS PAMP gold forecast and the consensus view from broker research desks, which have spent most of the year defending year-end targets in the $4,200 to $4,800 zone. Shiels has gone further out on the curve and put a real number on what fiscal dominance looks like if it actually shows up at the price tape, which is a more honest exercise than most strategists are willing to do in print. She has even said it is “theoretically possible” for gold to reach $10,000 by 2030, though she frames that as a tail risk rather than a base case.

To understand why a refiner would publish a number that aggressive, you have to back into the math the desk is using. That math starts with the assumption that the Fed has lost its room to maneuver.

The stagflation engine doing the heavy lifting

Stagflation is what happens when growth slows and inflation refuses to. The U.S. economy printed 2.0 percent annualized real GDP growth in the first quarter, according to the BEA advance estimate released on April 30, while headline CPI stayed sticky in the mid-3s. That is better than the recession scare that opened the year, but it is not the kind of expansion that cleans up the inflation problem. The Fed held its policy rate at 3.50 to 3.75 percent at the March 18 meeting, with Governor Stephen Miran dissenting in favor of a 25 basis point cut. The updated dot plot showed one cut for 2026 and another for 2027, a slower path than the bond market was pricing at the start of the year.

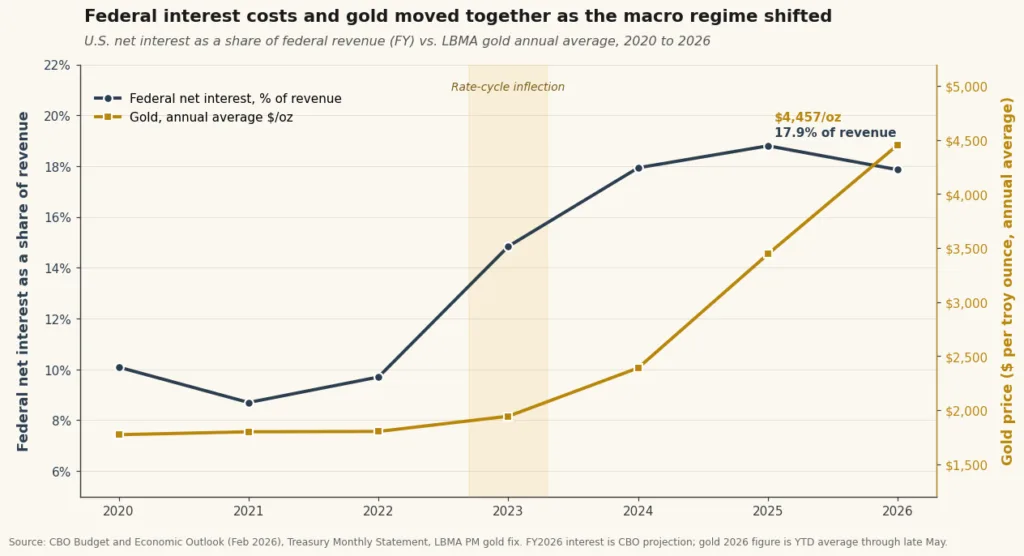

Ray Dalio, who runs Bridgewater Associates, put the diagnosis in plain English in a late April interview with Fortune. “We’re certainly in a stagflationary period,” he said, and warned that the most likely path through the next two years is a spiral that forces the Fed to monetize debt rather than fight inflation. Dalio has been recommending a 5 to 15 percent gold allocation as protection against what he has called a “debt death spiral,” with U.S. national debt now approaching $39 trillion and annual interest costs running about $1 trillion in fiscal 2026, or roughly 3.3 percent of GDP, according to CBO projections summarized by the American Action Forum.

That last number is where the MKS PAMP thesis lives. Interest expense above a trillion dollars a year makes the entire conversation about Fed independence harder to keep with a straight face. If you cannot cut rates because inflation is sticky, and you cannot let real rates rise because the Treasury cannot afford the interest bill, you are practicing fiscal dominance by another name. Gold is the asset that gets paid when the central bank loses the argument with the Treasury, and that link between sovereign balance sheets and the metal price is something we walked through in our analysis of how government debt replaced gold inside the Fed’s balance sheet.

The bid from central banks that will not let up

The second leg of the forecast is the most visible one if you read the World Gold Council reports closely. Central banks bought a net 244 tonnes of gold in the first quarter of 2026, a number that came in above both the previous quarter and the five-year average, according to the WGC Q1 2026 Gold Demand Trends report. The Council still projects a full-year purchase total in the 700 to 900 tonne range, which would mark the fifth consecutive year of buying above the long-run average.

The names doing the buying matter as much as the size. The National Bank of Poland led the league table again with 31 tonnes added in Q1, pushing its reserves to 582 tonnes as part of a multi-year plan to hit 700. Uzbekistan added 25 tonnes. The People’s Bank of China added 7 tonnes and more than doubled its prior quarter pace. None of these are tactical trades. They are sovereign reserve managers reweighting away from dollar assets and toward something that cannot be sanctioned, frozen, or printed against.

That structural bid is the reason MKS PAMP can underwrite an aggressive call. Investment demand is volatile and ETF flows can flip in a week, but central bank buying tends to grind in one direction for years at a time. It also helps explain why Swiss refining throughput has surged, a flow we tracked in our piece on Switzerland’s gold export surge and what the data is telling us.

Why silver and platinum sit in the same trade

Shiels did not stop at gold. The same outlook calls for silver to revisit the January high above $120 an ounce, with the caveat that the move is contingent on gold making fresh records first. The argument is straightforward. Silver remains far below its inflation-adjusted peak near $200 an ounce, and the gold-to-silver ratio has compressed but is still wide by historical standards. If the stagflation trade keeps grinding, silver gets the leveraged version of gold’s move.

Platinum is the cleaner industrial play in the forecast. MKS PAMP sees the metal reaching $2,000 an ounce in 2026, citing a structural deficit in the South African supply base and a long-running underinvestment cycle in mining capacity. Platinum has been the disappointment of the precious complex for nearly a decade, but the firm thinks the setup is finally in place for a breakout, and the bar for surprise is low compared with gold.

None of these calls require an outright dollar crisis to be right. They require the Fed to keep being late and the deficit to keep being financed at the short end of the curve. If both of those things hold, the entire precious complex re-rates, and the relationship between fiscal stress and metal prices we walked through in our breakdown of quantitative easing and gold keeps mattering more, not less.

What can derail the call

The most honest part of the MKS PAMP outlook is the acknowledgment that the path to $5,800 is not linear. The firm sees consolidation in the near term, and the May pullback toward $4,400 on softer oil and progress in the Strait of Hormuz negotiations is exactly the kind of move that has to happen before the next leg up. Gold trades like a coiled spring during stagflation episodes. It does not grind higher in a straight line, and traders who chase the breakout often get shaken out before the real move begins.

The cleanest derailment scenario is one where the Fed regains credibility. If Q2 GDP rebounds toward 2 percent and the inflation print finally rolls under 3, the stagflation narrative dies and the bond market starts pricing actual cuts. In that world real yields rise, the dollar firms, and gold caps at the low end of the MKS PAMP range rather than the high end. Shiels has been candid about this in interviews. The call is not a guarantee. It is the path the desk thinks is most likely given the data on its screens right now.

There is also the geopolitical wild card. Gold has morphed during the Iran conflict into something closer to an inverse oil proxy, and that correlation has scrambled the usual stagflation hedge logic. If the Hormuz negotiations actually resolve, oil drops further, and inflation expectations soften, gold gives back some of the conflict premium before the structural bid takes over. The longer-term thesis stays intact. The path just gets messier.

What the call actually means for a portfolio

If the MKS PAMP gold forecast is right and the metal prints $5,800 by December, gold will have roughly doubled from the start of 2025 in 24 months. That is not a normal cycle. It is the kind of move that happens when the macro regime changes underneath investors, the way it did in 1971 after Bretton Woods broke and again in 1979 when Volcker finally took the chair at the Fed. Dalio’s recommendation of a 5 to 15 percent allocation looks high until you compare it with actual pension fund behavior. According to World Gold Council research, only about a third of pension funds hold any gold at all, and among those that do, the majority sit at allocations of just 1 to 2 percent. The history of fiat currencies under fiscal stress, which we covered in our look at what Weimar, Zimbabwe, and Venezuela tell us about holding gold, suggests the institutional underweight is the real anomaly, not Dalio’s number.

The risk to underweight allocations is asymmetric. If the stagflation thesis is wrong, gold gives back maybe 15 percent and the rest of the portfolio benefits from rate cuts and a stronger dollar. If it is right, the metal does what MKS PAMP says it will do, and the gap between holders and non-holders becomes structural rather than tactical. That asymmetry, more than any single price target, is the actual reason the $5,800 call matters.

What happens at the next two FOMC meetings will tell us whether the desk has the timing right. The thesis is already in place. The price is the only thing left to argue about, and Shiels has put hers on the table in print.